Promissory Note Template for the State of New York

When it comes to financial agreements in New York, the Promissory Note form plays a crucial role. This initial aspect of borrowing or lending money might seem intimidating, but understanding its function and requirements is quite straightforward. Essentially, this document serves as a legally binding agreement between two parties — the borrower and the lender — laying out the repayment details of the money borrowed. It specifies the amount borrowed, the interest rate agreed upon, the repayment schedule, and what happens if the loan is not repaid. Importantly, New York has specific laws and guidelines that govern the drafting and enforcement of these documents, ensuring both parties are protected and clear on their obligations. The purpose behind this form is not only to provide a clear agreement to prevent any misunderstandings but also to offer a legal framework that can be utilized to enforce the agreement, should the need arise. Navigating through the creation of a Promissory Note form might appear daunting at first glance, however, with a proper understanding of its components and significance, individuals can ensure their financial dealings are secure.

New York Promissory Note Sample

New York Promissory Note Template

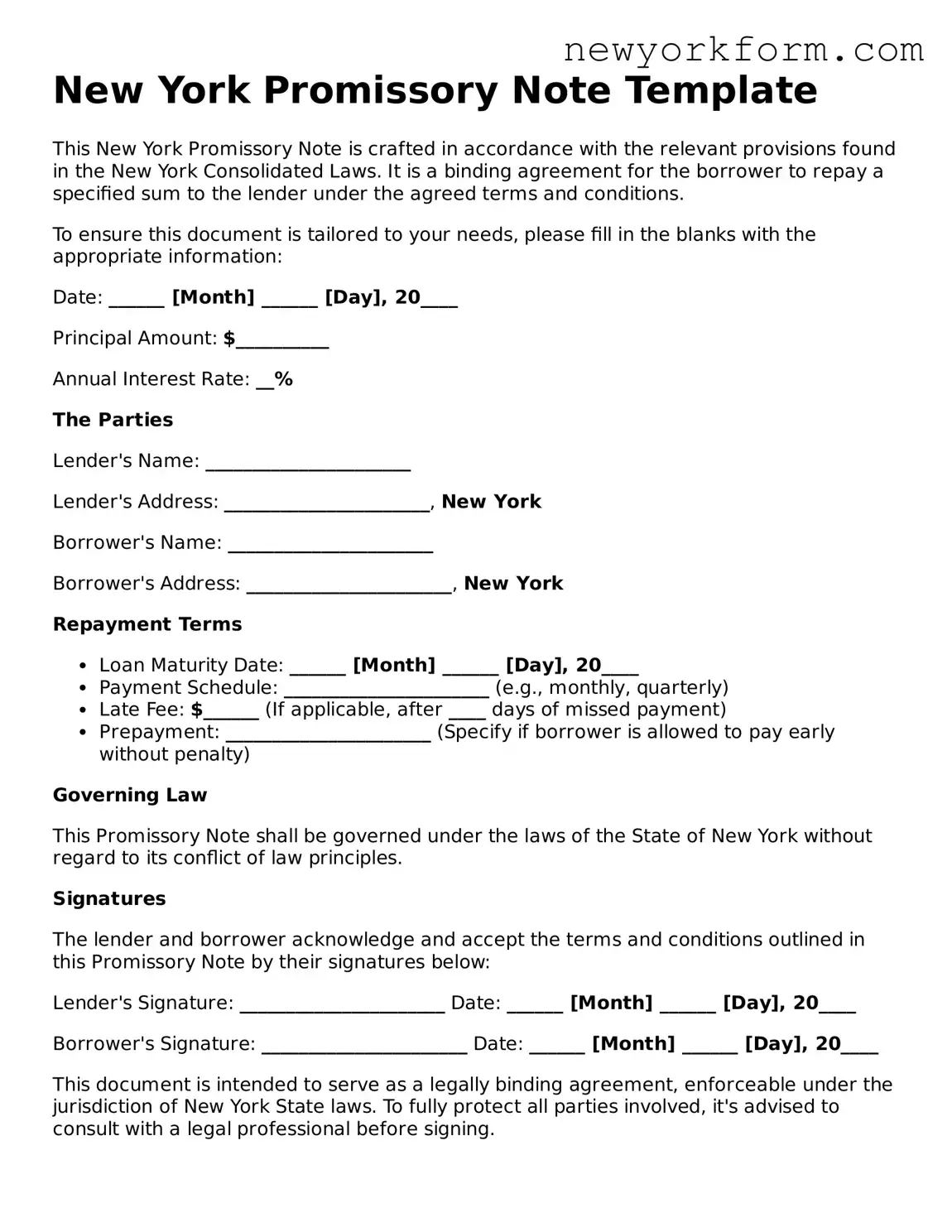

This New York Promissory Note is crafted in accordance with the relevant provisions found in the New York Consolidated Laws. It is a binding agreement for the borrower to repay a specified sum to the lender under the agreed terms and conditions.

To ensure this document is tailored to your needs, please fill in the blanks with the appropriate information:

Date: ______ [Month] ______ [Day], 20____

Principal Amount: $__________

Annual Interest Rate: __%

The Parties

Lender's Name: ______________________

Lender's Address: ______________________, New York

Borrower's Name: ______________________

Borrower's Address: ______________________, New York

Repayment Terms

- Loan Maturity Date: ______ [Month] ______ [Day], 20____

- Payment Schedule: ______________________ (e.g., monthly, quarterly)

- Late Fee: $______ (If applicable, after ____ days of missed payment)

- Prepayment: ______________________ (Specify if borrower is allowed to pay early without penalty)

Governing Law

This Promissory Note shall be governed under the laws of the State of New York without regard to its conflict of law principles.

Signatures

The lender and borrower acknowledge and accept the terms and conditions outlined in this Promissory Note by their signatures below:

Lender's Signature: ______________________ Date: ______ [Month] ______ [Day], 20____

Borrower's Signature: ______________________ Date: ______ [Month] ______ [Day], 20____

This document is intended to serve as a legally binding agreement, enforceable under the jurisdiction of New York State laws. To fully protect all parties involved, it's advised to consult with a legal professional before signing.

PDF Form Information

| Fact | Detail |

|---|---|

| Governing Law | New York's promissory note form is governed by the state's General Obligations Law, as well as relevant federal laws, including the Truth in Lending Act for notes involving consumer loans. |

| Types | There are two main types of promissory notes used in New York: secured and unsecured. A secured note is backed by collateral, while an unsecured note is not, relying purely on the borrower's promise to pay. |

| Interest Rate Limit | Under New York law, the maximum interest rate a lender can charge on a personal loan is 16% per annum. Charging more than this rate can be considered usury, which is illegal. |

| Enforceability | To be legally enforceable in New York, a promissory note must be signed by the borrower and should clearly state the loan amount, interest rate, repayment schedule, and the consequences of default. |

| Statute of Limitations | In New York, the statute of limitations for taking legal action to collect a debt based on a promissory note is six years from the date of the note's maturity or the last payment date, whichever comes later. |

New York Promissory Note: Usage Guidelines

Filling out a New York Promissory Note is a task that's more straightforward than it might first appear. This document is an agreement for one party to pay back another party a certain amount of money, either on a specific date or over a period of time. Ensuring that all sections are completed accurately is crucial for the legality and enforceability of the note. The following steps are designed to guide you through this process smoothly.

- Start by identifying the party who will be borrowing the money (the "Maker") and the party who will be lending the money (the "Holder"). Write down their full legal names, complete addresses, and the date the promissory note is being created.

- Specify the principal amount of money being borrowed. This is the amount before any interest or fees that the Maker will owe to the Holder.

- Detail the interest rate that will be applied to the principal amount. This should be a yearly rate and it must comply with New York State's legal limits to avoid being considered usurious or illegal.

- Define the repayment schedule. Include the number of payments, the amount of each payment, and the frequency of payments (monthly, quarterly, etc.). Also, specify the start date of these payments.

- Include information about what will happen if a payment is late. Specify any late fees and after how many days a payment is considered late.

- Address the terms under which the remaining balance may become due immediately, a provision often referred to as an "acceleration clause." This typically covers scenarios such as the death of the Maker, a default on payments, or bankruptcy.

- Discuss any collateral that the Maker will provide to secure the loan. If the promissory note is secured, describe the collateral in clear, detailed terms.

- Both parties should sign and date the note. In some cases, you might also want to have the signatures witnessed or notarized to add an extra layer of authentication, though this is not a legal requirement in New York.

Once you've completed these steps, make sure copies of the promissory note are distributed to all involved parties. Keep the original document in a safe place, as it serves as a legally binding agreement that outlines the obligations of the Maker to the Holder. Following the steps outlined ensures a clear understanding by both parties and helps protect everyone's interests.

FAQ

-

What is a New York Promissory Note?

A New York Promissory Note is a legal document that creates a promise to pay a specified sum of money to a person or entity, the payee, either at a determined future date or on demand. The party promising to pay is known as the maker or issuer. Used widely across New York, this document helps ensure clarity in the terms of the debt, including repayment schedule, interest rate, and what happens if the debt is not repaid.

-

Is a New York Promissory Note legally binding?

Yes, in New York, as in other states, a properly executed promissory note is a legally binding contract. For enforceability, it should clearly state the amount to be repaid, the payment schedule, interest, and be signed by all parties involved. It may also require witness or notarization depending on the sum involved and the presence of collateral.

-

Are there different types of Promissory Notes in New York?

Indeed, New York recognizes several types of promissory notes, primarily secured and unsecured. A secured promissory note is backed by collateral, meaning if the borrower fails to repay, the lender can claim the collateral. An unsecured note, on the other hand, does not involve collateral, offering less security to the lender. The choice between them often depends on the amount of the loan, the relationship between the lender and borrower, and the degree of risk the lender is willing to accept.

-

What must be included in a New York Promissory Note?

To meet the legal requirements in New York, a promissory note must include: the full amount of the debt, interest rate, repayment schedule, details of the parties involved (lender and borrower), signatures, and any terms regarding late fees or prepayment penalties. If the note is secured, it should also detail the collateral. Clarity and completeness in these details can prevent disputes.

-

How is interest determined in a New York Promissory Note?

New York sets the legal maximum interest rate at 16% per annum for personal loans. This cap is designed to prevent usury, the practice of charging excessively high-interest rates. In a promissory note, the interest rate should be agreed upon by both parties within this legal boundary. The note should clearly state the rate, ensuring both borrower and lender understand the cost of the loan.

-

What happens if the borrower does not repay the note in New York?

If a borrower fails to repay according to the terms of the promissory note, the lender has several legal avenues in New York. For secured notes, the lender might seek to take possession of the collateral. For unsecured notes, the lender may initiate a lawsuit to recover the owed money. Additionally, defaulting on the loan might allow the lender to demand immediate payment of the entire outstanding balance, plus any applicable interest and fees.

-

Can parties modify a Promissory Note?

Yes, parties can modify a New York Promissory Note, but any modifications must be agreed upon by both the lender and the borrower. It’s advisable to document any amendments in writing and have both parties sign off, to maintain the note’s enforceability. This process ensures the agreement continues to reflect the mutual understanding of the repayment terms.

-

Is a witness or notarization required for a Promissory Note in New York?

While New York law does not specifically require a promissory note to be witnessed or notarized, having a notary or witness can add a layer of protection against future disputes over its validity. Notarization, in particular, provides a legal attestation that the signatures on the note are genuine. Nonetheless, the core legality of the note hinges on the clarity of the terms and the proper signatures of the parties involved.

-

How can a New York Promissory Note be enforced if disputed?

Should a dispute arise over a New York Promissory Note, the aggrieved party might first seek a resolution through direct communication or mediation. If these efforts fail, they can file a lawsuit in the appropriate court, depending on the amount of the loan. The documentation provided in the promissory note serves as the foundational evidence of the loan’s terms and conditions, which the court will analyze to adjudicate the dispute.

Common mistakes

Filling out a New York promissory note form seems straightforward, but errors can easily occur. Knowing what mistakes to avoid ensures the document is valid and enforceable. These missteps range from basic oversights to more nuanced legal considerations.

- Not specifying the type of promissory note. New York recognizes both secured and unsecured promissory notes. A secured note is backed by collateral, whereas an unsecured note isn’t. Failing to define the type can lead to misunderstandings and issues if repayment problems arise.

- Omitting key details. Every promissory note must include the principal amount loaned, interest rate, repayment schedule, and parties’ information. Leaving out any of these details can make the note difficult to enforce.

- Incorrect interest rate. New York has laws governing the maximum interest rate that can be charged. Charging an illegal interest rate, even unintentionally, can render the note entirely void or subject the lender to legal penalties.

- Ignoring state laws. Besides interest rates, other state-specific regulations must be followed. For example, the note may need to include specific disclosures or language. Not adhering to these laws can compromise the legal standing of the note.

- Vague repayment terms. Ambiguity in how or when the loan should be repaid can lead to disputes. Clearly define the repayment process, including any grace periods or penalties for late payment.

- Forgetting to specify the governing law. Indicating which state’s law will govern the note helps resolve any legal disputes. In the case of a New York promissory note, specifying New York law is crucial, especially if parties are from different states.

- Not having it signed. An unsigned promissory note is generally unenforceable. Ensure that all parties sign the document, preferably in the presence of witnesses or a notary public for added legal validity.

- Neglecting to make copies. Once signed, failing to provide all parties with a copy of the promissory note is a critical mistake. This ensures that everyone has a record of the agreement and its terms.

- Failing to include a clause on modification. Circumstances change, and the promissory note may need amendments. Without a modification clause, adjusting any aspect of the note can become legally challenging.

To avoid these common pitfalls, attention to detail and a thorough understanding of New York’s legal landscape are critical. It’s often wise to consult a legal professional when preparing a promissory note. This ensures all legal requirements are met, and the agreement stands up in court, should disputes arise. Handling these documents with care and diligence is key to a smooth financial transaction.

Documents used along the form

When dealing with financial agreements in New York, a Promissory Note is essential for outlining the terms of a loan between parties. This document is crucial for ensuring all parties understand the amount loaned and the repayment schedule. However, to ensure a smooth lending process, several other documents are often used alongside a Promissory Note. Each serves a unique purpose, complementing the Promissory Note to provide a comprehensive framework for the transaction.

- Loan Agreement: This document is more comprehensive than a Promissory Note and outlines the duties and obligations of each party in detail. It includes specifics such as the repayment schedule, interest rates, and what happens in case of a default. This serves as a legal foundation for the loan.

- Security Agreement: If the loan is secured with collateral, a Security Agreement details the asset(s) pledged as security. This guarantees the lender rights to the collateral if the borrower defaults, outlining conditions under which the lender can seize the asset.

- Guaranty: This document is used when a third party agrees to guarantee the loan, providing an assurance to the lender that the loan will be repaid. The guarantor becomes liable if the borrower fails to fulfill the repayment obligations.

- Amortization Schedule: An Amortization Schedule is often attached to a Promissory Note to detail the breakdown of payments over the loan term. It shows each payment's contribution to the principal amount and interest, illustrating how the loan balance decreases over time.

- Notice of Default: This document is used to inform a borrower that they have failed to meet one or more obligations of the Promissary Note. It sets out the nature of the default and the steps that may be taken to rectify the situation, including any grace periods afforded to the borrower.

In the realm of lending and finances, these documents collectively ensure that both parties are well-informed and protected. While the Promissory Note outlines the basic terms of the loan, companion documents like a Loan Agreement and Security Agreement provide detailed frameworks and safeties for the lending process. Including these additional documents helps to mitigate risks and clarifies the responsibilities of all parties involved in the transaction.

Similar forms

A Loan Agreement is a document similar to the New York Promissory Note, as both outline the terms under which money has been borrowed and must be repaid. While a promissory note succinctly binds one party to repay a sum to another, a loan agreement typically goes into greater detail, including the responsibilities of both the lender and borrower, the interest rate, payment schedules, and the consequences of non-payment.

A Mortgage Agreement is another document that shares similarities with a New York Promissory Note, particularly in its function of setting terms for the borrowing and repaying of money. However, a mortgage agreement specifically ties the loan to the purchase of real estate, using the property itself as security for the loan. Should the borrower fail to repay, the lender has the right to take ownership of the property.

A Deed of Trust functions similarly to the New York Promissory Note by detailing the borrower's obligation to repay a loan. The difference lies in that a deed of trust involves three parties: the borrower, the lender, and a trustee who holds the property title until the loan is repaid in full. This setup is often used in place of a traditional mortgage in some states.

Personal Guarantees are documents that, like New York Promissory Notes, are used to ensure that a loan is repaid. In a personal guarantee, a third party agrees to repay the loan if the original borrower does not. This guarantee provides additional security to the lender by backing the loan with the guarantor's personal assets, making it a stronger instrument for debt collection.

An IOU (I Owe You) is a simplified version of a New York Promissory Note that acknowledges that one party owes another a certain amount of money. While it is less formal and typically lacks detailed terms of repayment, an IOU serves as a written confirmation of a debt, similar in essence to a promissory note but without legal complexities and often not specifying repayment details.

Bills of Sale are similar to New York Promissory Notes in that they document the transfer of ownership or title of goods from one party to another, often involving a monetary exchange. While a promissory note records a commitment to pay a specific amount, a bill of sale confirms that a transaction has taken place, listing the item sold, the purchase price, and the parties involved.

Dos and Don'ts

When filling out the New York Promissory Note form, certain practices should be followed to ensure the document is completed accurately and legally. Here are some guidelines:

Do's:

- Ensure all information is complete and accurate, including the full names of the borrower and lender, the loan amount, interest rate, and repayment schedule.

- Verify the legality of the interest rate according to New York state laws to avoid any usury violations.

- Include a clear repayment schedule, outlining when payments are due, the number of payments, and if there are any late fees.

- Specify the consequences of defaulting on the loan to make both parties aware of the potential legal and financial repercussions.

- Have the promissory note signed by both the borrower and the lender in the presence of a witness or notary, if required, to enhance its enforceability.

- Keep a copy of the fully signed promissory note for both the borrower's and lender's records.

Don'ts:

- Do not leave any blanks in the form; unanswered sections can lead to disputes or misunderstandings in the future.

- Avoid using unclear or ambiguous terms that might be interpretable in multiple ways; specificity is crucial.

- Do not forget to state whether the loan is secured or unsecured; this distinction can significantly impact the enforcement of the note.

- Refrain from setting an interest rate that exceeds New York state’s maximum legal rate to prevent the document from being invalid.

- Avoid neglecting to detail the loan's purpose, if applicable, especially if the loan is for a specific use.

- Do not fail to review and understand every part of the note before signing; once signed, it becomes a legal document.

Misconceptions

Many misconceptions surround the New York Promissory Note form. Understanding these common errors can help individuals navigate their financial agreements with more confidence and legal awareness. Here are seven notable misconceptions:

- All promissory notes are the same. It is incorrect to think that there's a one-size-fits-all promissory note. New York, like other states, has specific legal requirements and guidelines that may differ from those in other jurisdictions.

- Oral agreements are as binding as written ones. While oral agreements can be legally binding, a written promissory note is much easier to enforce. In New York, having a promissory note documented and signed can be critical in legal disputes.

- A signature is all that's needed to make it legal. Aside from the borrower’s signature, New York law may require witness signatures or notarization for the document to be considered legally binding in certain situations.

- Interest rates can be as high as agreed upon by the parties. New York State has usury laws that cap interest rates. Violating these caps can render a promissory note unenforceable and possibly subject the lender to legal penalties.

- Promissory notes are only for business loans. This is a misconception as promissory notes can also be used for personal loans between family members or friends, not just for business financing or transactions.

- There are no legal consequences if a promissory note is not repaid. The truth is, failing to repay a loan as outlined in a promissory note can lead to legal action, including but not limited to, wage garnishment, asset seizure, or a judgment against the borrower.

- The borrower is the only party with responsibilities. While the borrower must repay the debt according to the terms of the note, the lender is also bound by laws regarding how they conduct the lending process and pursue repayment.

Understanding the specific requirements and legal implications of the New York Promissory Note form is crucial for both lenders and borrowers. It ensures that financial transactions are conducted fairly and within the scope of the law.

Key takeaways

Understanding the components and legal significance of a promissory note is critical, particularly when it comes to financial transactions in New York. Here are key takeaways that should help you navigate the process of filling out and utilizing the New York Promissory Note form effectively:

- Clarify the Amount: The promissory note must clearly state the amount of money being borrowed. This clarity is crucial to ensure there is no ambiguity about the debt obligation.

- Identify the Parties: Both the borrower and the lender must be properly identified by their legal names to avoid any future disputes over who is involved in the agreement.

- Interest Rate Compliance: Ensure the interest rate complies with New York's usury laws. Charging an interest rate higher than what's legally allowed can render the promissory note void or subject the lender to legal penalties.

- Repayment Schedule: The note should specify how repayment will be made, whether in installments, a lump sum, or at will (demand note). A clear repayment schedule helps both parties understand their obligations.

- Security or Collateral: If the promissory note is secured, the collateral must be described clearly. This ensures both parties are aware of the asset(s) subject to seizure in case of default.

- Late Fees and Penalties: If applicable, the note should outline any late fees or penalties for missed payments. This can incentivize timely repayment and provide recourse for the lender.

- Acceleration Clause: Including an acceleration clause can protect the lender by allowing them to demand immediate payment of the entire outstanding balance if the borrower violates terms of the agreement.

- Governing Law: Specify that New York law governs the promissory note. This is important for enforcing the note's terms and resolving any disputes.

- Signatures: Both the borrower and the lender must sign the promissory note. Signatures officially bind the parties to the terms of the agreement, making it a legally enforceable document.

When properly filled out and utilized, the New York Promissory Note form is a powerful tool that provides security for the lender and clarity for the borrower. Taking the time to understand and accurately complete the form can prevent misunderstandings and legal issues down the line.

Fill out More Forms for New York

Mv New York - Including contact information for both parties in the Motorcycle Bill of Sale facilitates easy follow-up if necessary.

Notary Sworn Statement - It protects the serving party by providing a legal shield against claims of improper service or non-notification.

Corporate Formation - The information contained sets legal and operational precedents for the corporation’s future.