Free Nys Dtf 17 Form in PDF

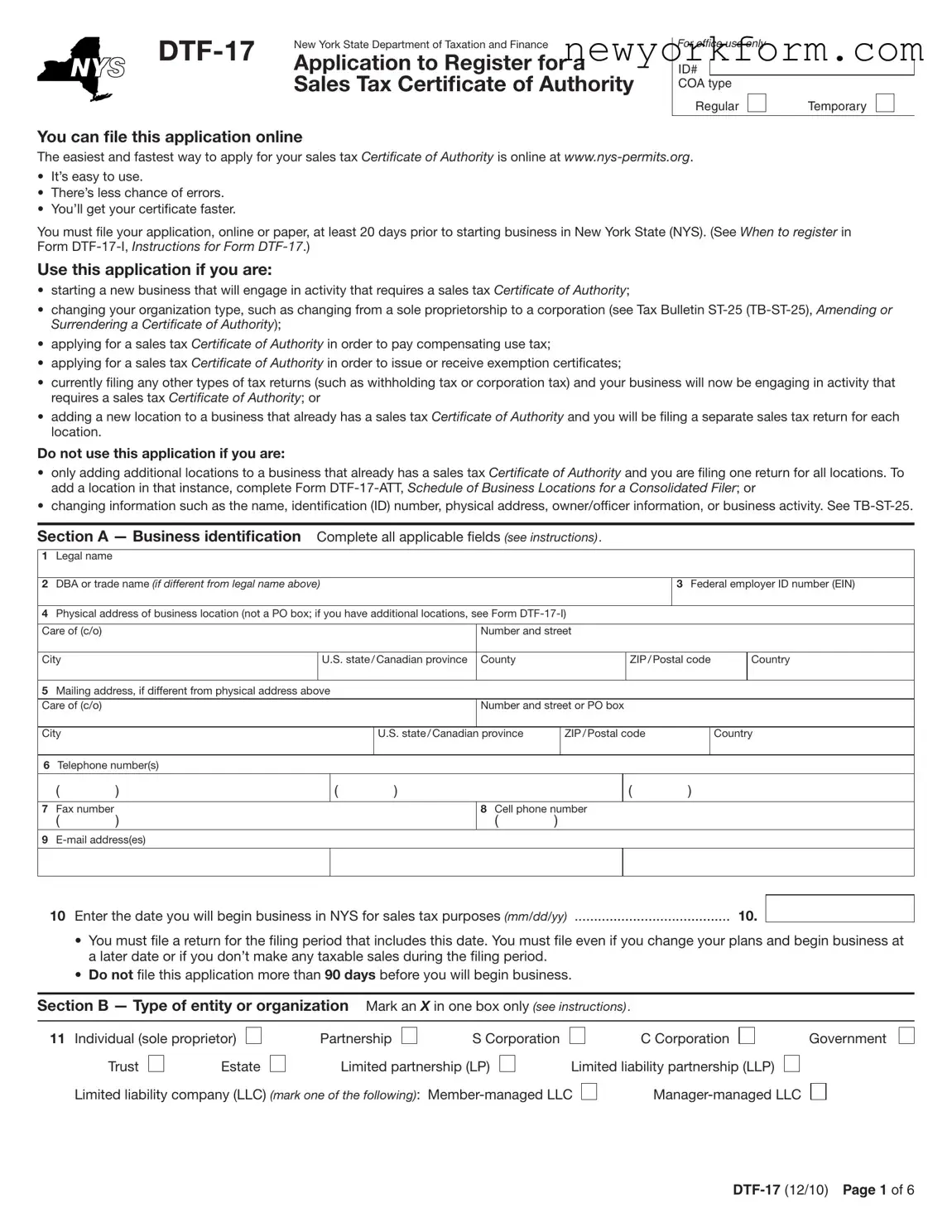

Engaging in business activities within New York State that necessitate collecting sales tax requires obtaining a Sales Tax Certificate of Authority, which can be applied for using the DTF-17 form provided by the New York State Department of Taxation and Finance. This form serves various purposes, including registering a new business for sales tax collection, changing an organization's type, applying to pay use tax, or issuing/receiving exemption certificates, among other activities. Importantly, the form must be filed at least 20 days before commencing business operations in the state, offering an online application option to streamline the process and minimize errors. Additionally, it details specifics on the type of entity, franchisor information (if applicable), and whether the business will file combined or separate sales tax returns for multiple locations. It also addresses situations involving acquisition of businesses and outlines the requirement to describe business activities and provide information about responsible persons, banking details for tax purposes, and any professional tax preparer involved. Completing and submitting this form is crucial for compliance with state tax regulations, thereby enabling businesses to legally conduct taxable sales and services within New York State.

Nys Dtf 17 Sample

New York State Department of Taxation and Finance |

|

|

|

|

Application to Register for a |

|

Sales Tax Certificate of Authority |

For office use only

ID#

COA type

Regular |

|

Temporary |

You can file this application online

The easiest and fastest way to apply for your sales tax Certificate of Authority is online at

•It’s easy to use.

•There’s less chance of errors.

•You’ll get your certiicate faster.

You must ile your application, online or paper, at least 20 days prior to starting business in New York State (NYS). (See When to register in Form

Use this application if you are:

•starting a new business that will engage in activity that requires a sales tax Certificate of Authority;

•changing your organization type, such as changing from a sole proprietorship to a corporation (see Tax Bulletin

•applying for a sales tax Certificate of Authority in order to pay compensating use tax;

•applying for a sales tax Certificate of Authority in order to issue or receive exemption certiicates;

•currently iling any other types of tax returns (such as withholding tax or corporation tax) and your business will now be engaging in activity that requires a sales tax Certificate of Authority; or

•adding a new location to a business that already has a sales tax Certificate of Authority and you will be iling a separate sales tax return for each location.

Do not use this application if you are:

•only adding additional locations to a business that already has a sales tax Certificate of Authority and you are iling one return for all locations. To add a location in that instance, complete Form

•changing information such as the name, identiication (ID) number, physical address, owner/oficer information, or business activity. See

Section A — Business identification Complete all applicable ields (see instructions) .

1Legal name

2DBA or trade name (if different from legal name above)

3Federal employer ID number (EIN)

4Physical address of business location (not a PO box; if you have additional locations, see Form

Care of (c/o) |

|

Number and street |

|

|

|

|

|

|

|

City |

U.S. state / Canadian province |

County |

ZIP / Postal code |

Country |

|

|

|

|

|

5Mailing address, if different from physical address above

Care of (c/o) |

|

Number and street or PO box |

|

|

|

|

|

|

|

City |

U.S. state / Canadian province |

ZIP / Postal code |

Country |

|

|

|

|

|

|

6Telephone number(s)

( )

( )

( )

7 Fax number

( )

9

8 Cell phone number

( )

10 Enter the date you will begin business in NYS for sales tax purposes (mm/dd/yy) |

10. |

•You must ile a return for the iling period that includes this date. You must ile even if you change your plans and begin business at a later date or if you don’t make any taxable sales during the iling period.

•Do not ile this application more than 90 days before you will begin business.

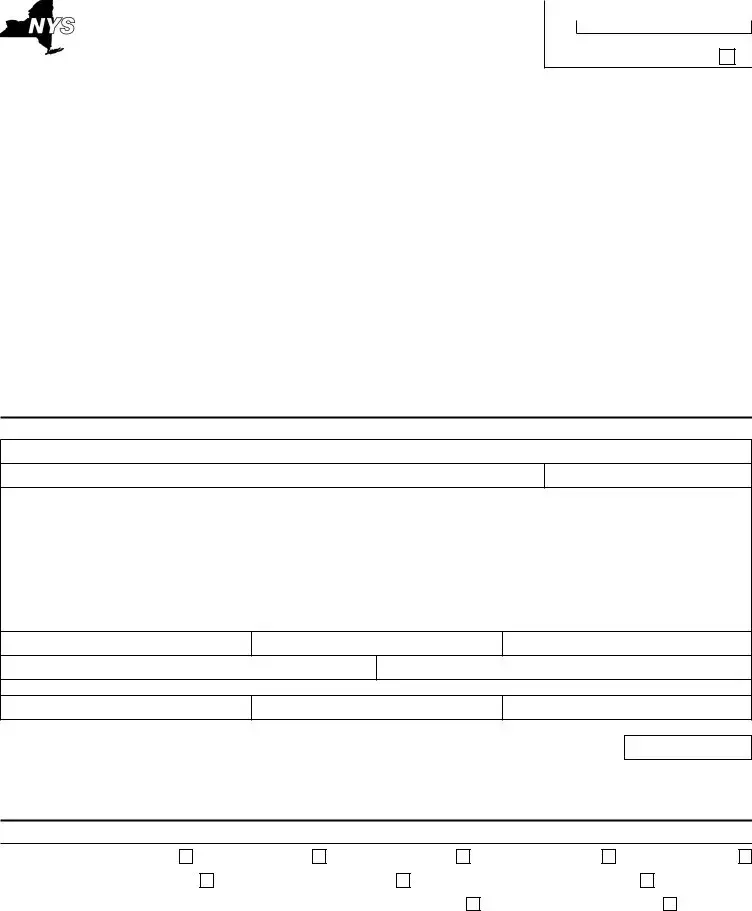

Section B — Type of entity or organization Mark an X in one box only (see instructions) .

11Individual (sole proprietor)

Trust |

|

Estate |

Partnership |

S Corporation |

Limited partnership (LP)

C Corporation |

Government |

Limited liability partnership (LLP)

Limited liability company (LLC) (mark one of the following):

PAGE 2 of 6

Section B — Type of entity or organization (continued)

12a |

Are you a franchisee? |

12a. Yes |

12b |

If Yes, provide franchisor’s name and address: |

|

No

Franchisor’s name

Franchisor’s address (number and street)

City

U.S. state/Canadian province

ZIP/ Postal code

Country

Section C — Business information (see instructions)

If you have more than one permanent place of business, mark an X in the appropriate box to indicate how you will ile.

13a Separate sales tax returns for each location (you must complete a separate Form |

13a. |

13b One sales tax return for all locations (you must also complete Form |

13b. |

14a If you or your business currently ile, have iled in the past, or were required to ile sales tax returns or returns for other NYS business taxes, such as corporation tax or withholding tax, enter the ID number(s) below.

•

•

•

ID number

ID number

ID number

Tax type

Tax type

Tax type

14b Were you previously registered to collect sales tax, but your Certificate of Authority expired or was |

|

|

|

|

|

surrendered, revoked, or suspended? |

14b. Yes |

No |

|

|

If Yes, provide the ID number from your previous business (if available) |

|

|

|

14c |

14c. |

|

|

|

15You can choose to register as a temporary vendor if your business does not expect to make taxable sales for more than two consecutive sales tax quarters (see instructions). Provide the date that your business

activity will end (mm/dd/yy) |

|

|

|

|

15. |

|

|

|

||

16 If you acquired all or part of the assets of a business that was registered (or required to be registered) for sales tax, |

|

|||||||||

did you ile Form |

... 16. Yes |

No |

||||||||

|

Information about former business owner: |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

Sales tax ID number |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Address (number and street) |

|

City |

U.S. state / Canadian province |

ZIP / Postal code |

|

|

Country |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Section D — Business activity |

Mark an X in the applicable box for each item (see instructions). |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Licenses

17a Are you or do you intend to be licensed by the NYS Liquor Authority (SLA)? |

17a. |

Yes |

17b If Yes, enter your SLA license number (if available) |

17b. |

|

|

No

18a |

Are you or do you intend to be licensed by the NYS Lottery? |

18a. |

Yes |

|

18b |

If Yes, enter your Lottery retailer number (if available) |

18b. |

|

|

|

|

|||

19a |

.............Do you or will you operate a facility registered with the NYS Department of Motor Vehicles (DMV)? |

19a. |

Yes |

|

19b |

If Yes, enter your DMV facility number (if available) |

19b. |

|

|

|

|

|||

No

No

Section D — Business activity (continued)

Sales of goods and services

Do you intend to sell or provide any of the following goods and services? |

|

|

|

20a Cigarettes or other tobacco products sold at retail |

20a. |

Yes |

|

|

If Yes, complete and attach Form |

|

|

|

and Vending Machines for Sales of Cigarettes and Tobacco Products. |

|

|

20b |

New tires (automotive, motorcycle, trailer, etc.) |

20b. |

Yes |

20c |

Passenger car rentals |

20c. |

Yes |

20d |

Motor fuel sold at a illing station |

20d. |

Yes |

20e |

Diesel motor fuel sold at a illing station |

20e. |

Yes |

20f |

Heating fuels, including diesel, irewood, pellets, or coal |

20f. |

Yes |

20g |

Electricity or gas (including propane in containers of 100 pounds or more), steam, or refrigeration |

20g. |

Yes |

20h |

Mobile telecommunications service |

20h. |

Yes |

20i |

Other telecommunications service, including telephone answering service |

20i. |

Yes |

20j |

Clothing or footwear |

20j. |

Yes |

20k |

Hotel, motel, or other accommodations located in Nassau County or Niagara County |

20k. |

Yes |

20l |

Restaurant or tavern food or drink, or other food service (including catering, |

|

|

|

located in Nassau County or Niagara County |

20l. |

Yes |

20m |

Admissions to places of amusement, club dues, and/or cabaret charges located in Niagara County |

20m. |

Yes |

No

No

No

No

No

No

No

No

No

No

No

No

No

New York City only:

20n |

Parking or garaging services |

20n. |

Yes |

20o |

Interior decorating or design services |

20o. |

Yes |

20p |

Beauty, barbering, or miscellaneous personal services |

20p. |

Yes |

20q |

Interior cleaning or maintenance services |

20q. |

Yes |

20r |

Protective or detective services |

20r. |

Yes |

20s |

Credit rating or reporting services |

20s. |

Yes |

20t |

Hotel, motel, or other accommodations |

20t. |

Yes |

|

Other: |

|

|

20u |

Are you a manufacturer or a wholesaler that does not make retail sales? |

20u. |

Yes |

20v |

Will you participate solely in lea markets, antique shows, or other shows? |

20v. |

Yes |

20w |

Will you conduct business solely as a sidewalk vendor? |

20w. |

Yes |

No

No

No

No

No

No

No

No

No

No

Section E — Account and reporting information

21Enter the information for the bank account where sales tax money will be deposited. You must provide this information even if the account you list will not be used exclusively for sales tax purposes.

Manufacturers and wholesalers: enter the primary bank account information for your business.

Bank name

Routing number

Account number

22 Do you intend to accept credit cards? |

22. Yes |

No

23If this is not the entity that will be reporting the income from the operations of this business on an income tax return or corporation tax return, enter the name and EIN of the legal entity or social security number (SSN) for the individual that will be reporting the income from the operations of the business iling sales and use tax returns.

Name of legal entity or individual

EIN or SSN

PAGE 4 of 6

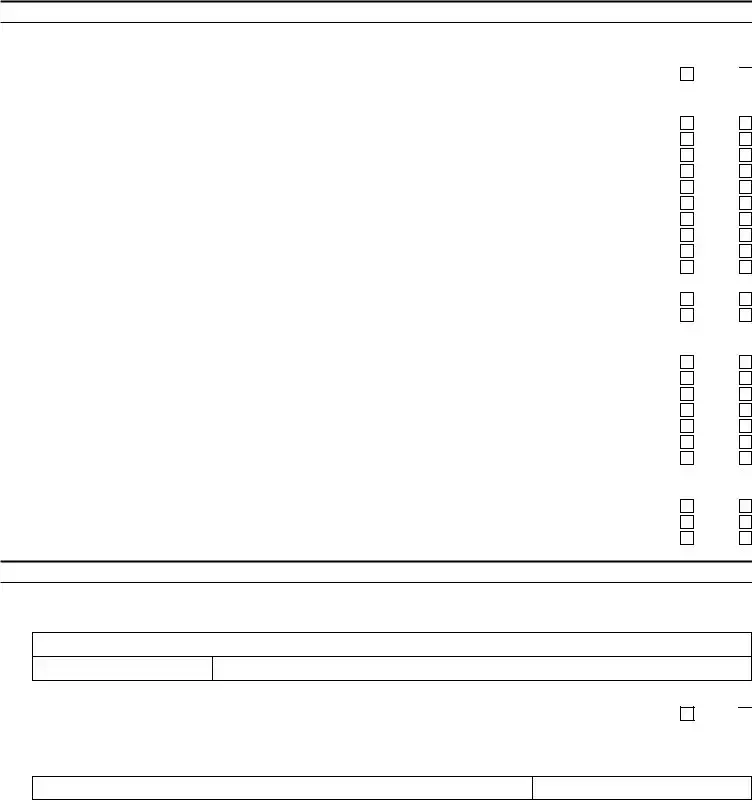

Section F — Business description (see instructions)

24a In the space below, briely describe your business activities. Describe the products or services that you will sell in NYS from the business location(s) that you are registering. Please be speciic. See the instructions for examples.

Enter the NAICS code that best describes the principal (and secondary, if appropriate) activity of the business location(s) that you are registering. You can ind a list of NAICS codes in Publication 910, Principal Business Activity for New York State Purposes, or by using the online NAICS Code Lookup on our Web site (see Need help? in Form

24b Principal NAICS code (required)

24c Secondary NAICS code

Section G — Responsible person(s) (see instructions)

Enter the applicable information for all responsible persons (see instructions). This includes, but is not limited to, owners, partners, members, oficers, and any other person responsible for the business’s

25 |

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

Section G — Responsible person(s) (continued)

|

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

Name (first, middle initial, last, suffix) |

|

|

|

|

Business title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street; not a PO Box) |

|

City |

|

|

U.S. state /Canadian province |

ZIP/ Postal code |

Country |

||

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

Home phone number |

|

Effective date of assuming responsibility |

|

|||||

|

|

( |

) |

|

|

|

|

|

|

|

|

Primary duties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All responsible persons must complete the following — except those in |

Ownership |

Proit distribution percentage, if different than |

|||||||

|

C corporations, government entities, trusts, and estates |

percentage if over 5%: |

ownership percentage and if over 5%: |

|||||||

|

|

|

|

|

|

|

|

|

|

|

Section H — Tax preparer information

Tax preparer’s or irm’s name |

|

|

Preparer’s or irm’s EIN (if known) |

Preparer’s NYTPRIN (if known) |

|||||

|

|

|

|

|

|

|

|

|

|

Preparer’s or irm’s address (number and street) |

City |

U.S. state/Canadian province |

ZIP/Postal code |

|

|

Country |

|||

|

|

|

|

|

|

|

|

|

|

Preparer’s |

|

|

|

Preparer’s telephone number |

|

Preparer’s PTIN (if known) |

|||

|

|

|

|

( |

) |

|

|

|

|

If you want sales tax information mailed to this preparer, mark an X in the box .............................................................................................

Section I — Signature of responsible person – Complete all ields (see instructions)

I certify that the above statements are true, complete, and correct, and that no material information has been omitted. I make these statements with the knowledge that willfully providing false or fraudulent information with this document may constitute a felony or other crime under New York State Law, punishable by a substantial ine and possible jail sentence. I also understand that the Tax Department is authorized to investigate the validity of any information entered on this document.

Name

Signature

|

SSN |

|

|

Date |

|

|

|

|

|

Title |

Daytime telephone number |

|||

|

|

( |

) |

|

If your application is missing information or is not signed, we will return it to you.

Mail your application to: NYS TAX DEPARTMENT

SALES TAX REGISTRATION UNIT

W A HARRIMAN CAMPUS

ALBANY NY 12227

PAGE 6 of 6

This page was intentionally left blank.

File Overview

| Fact Name | Fact Detail |

|---|---|

| Form Purpose | DTF-17 is used to apply for a Sales Tax Certificate of Authority in New York State. |

| Application Method | The application can be filed online, which is easier and faster, reducing the chances of errors. |

| Deadline for Filing | Applications must be filed at least 20 days before starting business activities in New York State. |

| Who Should Use It | The form is intended for new businesses requiring a sales tax Certificate of Authority, changes in organization type, businesses needing to issue or receive exemption certificates, among other specified situations. |

| Who Should Not Use It | The form is not for businesses only adding locations under an existing Certificate of Authority or changing basic business information. |

| Temporary Vendor Registration | Businesses not expecting to make taxable sales for more than two consecutive sales tax quarters can register as temporary vendors. |

| Governing Law | The application and issuance of a Sales Tax Certificate of Authority in New York State are governed by the state's taxation laws and regulations. |

Nys Dtf 17: Usage Guidelines

After the decision to start or expand a business in New York State (NYS) that involves activities requiring a sales tax Certificate of Authority, the immediate step is to file an application. This move is crucial for businesses aiming to engage in taxable sales within the state. Not only does this compliance step ensure the legality of your business operations, but it also streamulates the financial responsibilities towards the state. With a deadline of at least 20 days before initiating business activities in NYS, proper and timely completion of the application is essential. Given the option, applying online at www.nys-permits.org is recommended for its ease, reduced error margin, and quicker processing times. However, if a paper application suits better, understanding and meticulously following the form filling instructions is crucial.

- Section A - Business Identification: Fill in your legal business name, any DBA (Doing Business As) or trade name, provide your Federal Employer Identification Number (EIN), and list the physical location of your primary business (note that PO boxes are not acceptable). If the mailing address differs from the physical one, include that as well.

- Provide contact numbers, including telephone, fax, cell, and email addresses to ensure the state can contact you regarding your application.

- Enter the date you anticipate to start your business operations in NYS for sales tax purposes in the format mm/dd/yy.

- Section B - Type of Entity or Organization: Mark the box that corresponds to your business structure (Individual, Corporation, LLC, etc.). If you're a franchisee, indicate that and provide your franchisor’s name and address.

- Section C - Business Information: Detail if you have more than one business location and how you intend to file sales tax returns. Also, disclose if you or your business has previously registered or is required to for NYS business taxes, including any ID numbers associated with past filings.

- If applicable, specify whether you’re registering as a temporary vendor and state the planned end date of taxable sales activities.

- Note if you have purchased assets from a business that was previously registered for sales tax, mentioning if Form AU-196.10 was filed.

- Section D - Business Activity: Indicate your licensing status with the NYS Liquor Authority, Lottery, or if you operate a DMV-registered facility. Mark all applicable boxes that describe the goods or services you intend to sell, which may require additional forms or registration.

- Section E - Account and Reporting Information: Provide your bank account details where sales tax funds will be deposited. State whether you will accept credit cards and disclose the legal entity or individual reporting income from your operations, if different from the business itself.

- Section F - Business Description: Briefly describe your business activities, the products or services you’ll offer, and enter the NAICS code that best describes your business’s primary activity.

- Section G - Responsible Person(s): List all individuals with significant responsibility for the business's operations, including any owners, officers, or partners, providing their full names, home addresses, SSNs, contact details, and the date they assumed their role within the company.

- Leave Section H - Tax Preparer Information blank if it does not apply.

- Section I - Signature: The application must be signed by a responsible person, certifying the accuracy and completeness of the information provided. Include the signatory’s title, SSN, and daytime phone number.

Once completed, review the application to ensure all required fields are filled correctly. Missing or inaccurate information can delay the processing time. If submitting a paper form, send it to the appropriate address listed at the end of the form. Remember, prompt and accurate filing paves the way for a smoother commencement of your business operations in New York State.

FAQ

- How do I apply for a sales tax Certificate of Authority in New York State?

- When should I apply for my sales tax Certificate of Authority?

- What activities require a sales tax Certificate of Authority?

- Can I apply for a temporary sales tax Certificate of Authority?

To apply for a sales tax Certificate of Authority in New York State, you have the option to file your application either online or via a paper form. However, it is highly recommended to apply online at www.nys-permits.org for the fastest and easiest process. Applying online reduces the chance of errors and ensures you receive your certificate faster. If you decide to file a paper application or need more information about the online process, detailed instructions and necessary forms can be found at the New York State Department of Taxation and Finance's website.

You must submit your application at least 20 days before you start your business operations in New York State. However, do not file this application more than 90 days before your business will begin. This requirement ensures that your application is timely and that you comply with state regulations from the onset of your business activities. Filing outside of this window could result in delays or complications with receiving your Certificate of Authority.

If you are starting a new business that engages in activities requiring the collection of sales tax, or if you are changing your business structure, you will need to apply for a sales tax Certificate of Authority. Additionally, if your business involves selling at retail, operating as a vending machine or automotive dealership, renting out accommodations such as hotels or motels, or if you will be conducting any activity where sales tax is collected from customers in New York State, you must register for and obtain this certificate. Even businesses intending to issue or receive exemption certificates for sales tax purposes are required to register.

Yes, if you anticipate that your business will not make taxable sales for more than two consecutive sales tax quarters, you may opt to register as a temporary vendor. When applying, specify the expected date your temporary business activities will end. This option is suited for businesses participating in seasonal or short-term events, such as flea markets, holiday markets, or special events, ensuring compliance with New York State sales tax regulations for the duration of their temporary operation.

Common mistakes

Applying for a Sales Tax Certificate of Authority in New York State, using the DTF-17 form, is a critical step for businesses operating within the state. However, it's not unusual for applicants to encounter pitfalls during the process. Understanding these common mistakes can save time, prevent delays, and ensure compliance with state tax laws.

Not filing online: While paper applications are accepted, the New York State Department of Taxation and Finance recommends applying online for faster processing and fewer errors. Despite this, many individuals still opt for paper filings, which increases the likelihood of delays and mistakes.

Missing the filing deadline: Applicants are required to file the application at least 20 days before commencing business operations in New York State. Failing to meet this deadline can lead to operating without a valid Sales Tax Certificate of Authority.

Inaccurate business identification information: All fields under Section A must be completed accurately, reflecting the legal name, DBA (if applicable), Federal Employer ID Number (EIN), and physical address of the business. Mistakes or omissions in this section can cause significant delays in processing.

Incorrect type of entity selection: Section B asks for the business's entity type (e.g., individual, partnership, corporation). Incorrectly identifying your business type can affect your tax obligations and eligibility for certain benefits.

Omitting additional locations: If your business operates from multiple locations, each location may need to be registered separately. Failure to include all locations or to indicate the correct filing method under Section C can lead to compliance issues.

Not updating business information: Section D mandates accurate business activity descriptions and selections. Businesses that fail to provide detailed descriptions or check the appropriate boxes for their services or goods risk misclassification and incorrect tax assessments.

Skipping bank account information: Section E requires bank account details for sales tax deposits. Overlooking or avoiding this section can complicate tax payments and collections.

Neglecting responsible person's information: Section G demands details about all responsible persons, including SSNs and primary duties. Incomplete or inaccurate information can lead to issues with accountability and contact.

Leaving the signature section incomplete: The application must be signed by a responsible person to certify the accuracy of the information provided. An unsigned application is incomplete and will be returned.

Ignoring tax preparer information: If a tax preparer is involved in handling your sales tax filings, failing to provide their information in Section H can result in misdirected communications or accountability issues.

To sum up, when filling out the DTF-17 form, attention to detail and adherence to instructions are paramount. By avoiding these common errors, businesses can ensure a smoother registration process, enabling them to focus on their operations rather than on correcting preventable mistakes.

Documents used along the form

When businesses embark on the journey of obtaining a Sales Tax Certificate of Authority in New York State, the DTF-17 form is a crucial starting point. However, navigating the administrative landscape requires several other forms and documents, each serving its unique purpose in ensuring compliance with state regulations. The following list offers a glimpse into these essential documents, providing a brief description of each to aid businesses in their registration process.

- DTF-17-ATT: This form is known as the Schedule of Business Locations for a Consolidated Filer. It's used by businesses that operate multiple locations under one consolidated Sales Tax Certificate of Authority, allowing them to add additional locations to their existing registration.

- AU-196.10: The Notification of Sale, Transfer, or Assignment in Bulk is required when a business acquires assets of another business that was registered or required to be registered for sales tax. This form helps ensure that any outstanding tax liabilities are addressed.

- DTF-716: This Application for Registration of Retail Dealers and Vending Machines for Sales of Cigarettes and Tobacco Products is necessary for businesses intending to sell tobacco products, ensuring they comply with specific taxation rules for these items.

- ST-120: The Resale Certificate allows registered sales tax vendors to purchase items for resale without paying sales tax. This form is provided to suppliers to document that the purchase is for resale purposes.

- ST-100: The Quarterly Sales and Use Tax Return is a recurring document necessary for reporting sales tax collected from customers. It is essential for maintaining compliance with tax collection and filing requirements.

- ST-330: This Hotel Operators' Quarterly Sales Tax Return is specifically for businesses in the hospitality sector. It facilitates the reporting of taxes collected on accommodation charges.

- ST-119.1: The Exempt Organization Certificate is utilized by nonprofit and tax-exempt organizations to make tax-free purchases for organizational use, acknowledging their exemption status.

- IT-2104: The Employee's Withholding Allowance Certificate, although primarily used for income tax withholdings, is crucial for newly registered businesses in setting up their payroll systems in compliance with state tax requirements.

- TR-570: The Certificate of Registration for Highway Use Tax (HUT) is required for businesses that operate motor vehicles on New York State highways, ensuring the proper reporting and payment of highway use taxes.

Navigating the forms and documents associated with the registration for a Sales Tax Certificate of Authority may seem daunting at first. However, understanding the purpose and requirements of each form can make the process more manageable, ensuring that businesses remain compliant with New York State's taxation laws. Adequate preparation and attention to detail in completing these forms will pave the way for a smoother registration process and ongoing operations.

Similar forms

The Form SS-4, Application for Employer Identification Number (EIN), provided by the Internal Revenue Service, is similar to the NYS DTF-17 form because it is also an initial registration form that businesses need to fill out. Both forms require detailed information about the business, such as the legal name, physical and mailing addresses, type of entity, and identification numbers. The Form SS-4 primarily focuses on obtaining a federal EIN, which is necessary for tax filing and reporting at the federal level, akin to how the DTF-17 form is used to register for sales tax purposes at the state level.

Form W-9, Request for Taxpayer Identification Number and Certification, shares similarities with the DTF-17 because both documents collect taxpayer identification information, such as the business’s name and EIN or Social Security Number. While Form W-9 is used to provide a taxpayer identification number to entities that will pay you, thereby ensuring accurate reporting to the IRS, the DTF-17 is used to register a business with the NYS Department of Taxation and Finance for sales tax purposes. Both forms are critical in the proper management and identification of a business’s tax liabilities and responsibilities.

The Business License Application form, often used by cities or states, resembles the DTF-17 form in its purpose to register a business for regulatory compliance. Both forms collect detailed information about the business, including its name, location, and type of business activity. The primary difference lies in their scope; while the DTF-17 is specific to sales tax registration in New York State, a general Business License Application can cover a range of compliance areas from zoning to health and safety regulations, depending on the jurisdiction.

The UC-1, Unemployment Compensation Registration form, used by state departments to register businesses for state unemployment contributions, is similar to the DTF-17 in its function of registering a business for a specific governmental tax or contribution. Both forms require information about the business type, address, and identification numbers. However, the UC-1 focuses on unemployment insurance contributions, providing social security to unemployed workers, contrasting with the DTF-17’s focus on sales tax collection.

Form 2553, Election by a Small Business Corporation, is used to elect S corporation status for federal tax purposes and parallels the DTF-17 form in the aspect of choosing a business's taxation structure. While Form 2553 pertains to federal income tax selection, DTF-17 pertains to state sales tax registration. Both are critical in defining how a business is viewed and taxed by governmental authorities, affecting operational and fiscal strategies.

The Combined Registration Application commonly found in many states, which allows businesses to register for multiple tax types or permits, such as sales tax, withholdings tax, and unemployment insurance, shares a similar comprehensive approach with the NYS DTF-17 form. Both serve as a gateway for new businesses to meet state tax obligations, albeit the Combined Registration Application spans a broader array of tax responsibilities beyond just sales tax.

Form DTF-17-ATT, Schedule of Business Locations for a Consolidated Filer, which is specifically mentioned as an adjunct form to the DTF-17 for businesses with multiple locations filing under one sales tax certificate, illustrates the modular nature of tax and business registration processes. Like DTF-17, it collects detailed business information but focuses on the logistics of operating multiple premises under a single tax umbrella. This specificity complements the DTF-17's broader registration goal by addressing the complexity of larger business operations.

The Form 1065, U.S. Return of Partnership Income, although primarily an annual tax filing form for partnerships, intersects with the DTF-17 form in its collection of detailed business information, including identification numbers, business activity codes, and personal details of partners. The initial registration with DTF-17 ensures the business’s compliance with state sales tax laws, a foundational step before engaging in annual tax reporting obligations exemplified by Form 1065.

The Alcoholic Beverage Control (ABC) License Application, required for businesses selling alcohol, parallels the DTF-17 form through its role in regulatory compliance and need for detailed business information. Both forms enable businesses to operate within their respective legal frameworks—DTF-17 for sales tax and the ABC License for alcohol sales. Each ensures that businesses contribute to public coffers in accordance with their sales activities.

Lastly, the Zoning Permit Application, while not a tax document, is akin to the DTF-17 form in its requirement for detailed business information to assess compliance with local regulations. Where the DTF-17 form ensures businesses collect and remit sales taxes properly, a Zoning Permit Application ensures that the business location and operations comply with municipal land use and zoning laws, illustrating the breadth of regulatory compliance businesses must navigate beyond tax obligations.

Dos and Don'ts

Filling out the New York State Department of Taxation and Finance's DTF-17 form, which is the application for a Sales Tax Certificate of Authority, is a crucial process for businesses planning to operate within the state. To ensure accuracy and compliance with state tax laws, here are four things you should do and four things you shouldn't do when completing this form:

Do:- Apply early: Submit your application at least 20 days before you plan to start your business operations in New York State to ensure you receive your certificate in time.

- Ensure accuracy: Double-check all the information you enter, especially your business identification and bank account details, to prevent delays in the processing of your application.

- Provide a complete business description: Clearly describe your business activities and the goods or services you’ll be selling in New York State, including the NAICS code that best fits your main business activity.

- Use correct contact information: Make sure the email, telephone, and mailing addresses are current and accurate to avoid any miscommunication with the Department of Taxation and Finance.

- Estimate your start date: Enter the exact date you will begin business operations in New York State for sales tax purposes to ensure you file your returns for the correct filing period.

- Omit information about responsible persons: Provide complete details for all responsible persons involved in your business's operations, including their social security numbers and primary duties.

- Ignore the specific sales type questions: If you intend to sell or provide goods and services such as cigarettes, alcohol, or rent passenger cars, ensure you complete the additional forms required for these types of sales.

- Use a P.O. Box address for the business location: The physical address of your business location is required on the form and cannot be a P.O. Box. If you have a separate mailing address that is a P.O. Box, that can be included in the designated section.

By following these guidelines, you can streamline the process of obtaining your Sales Tax Certificate of Authority and avoid potential issues that could delay your business operations.

Misconceptions

Many people have misconceptions about the New York State Department of Taxation and Finance (NYS DTF) Form DTF-17, which is the Application to Register for a Sales Tax Certificate of Authority. Understanding these misconceptions is crucial for businesses looking to comply with New York State tax laws. Here are six common misconceptions:

- Misconception 1: The DTF-17 form can only be filed on paper.

This is not accurate. While you have the option to file this form on paper, New York State encourages businesses to file online at www.nys-permits.org. Filing online is not only easier but also reduces the chance of errors and speeds up the processing time, ensuring you receive your Certificate of Authority faster.

- Misconception 2: You can file the DTF-17 form at any time.

Filing this application at any time is a misunderstanding. Businesses must file the DTF-17 at least 20 days before they start operating in New York State. Additionally, the application should not be filed more than 90 days before the anticipated start date of the business.

- Misconception 3: Any business can file form DTF-17.

Actually, this form is specifically for businesses beginning activities that require a Sales Tax Certificate of Authority, changing their organizational type, applying to pay use tax, or needing to issue or receive exemption certificates, among other specific situations. If you're simply adding locations to an existing Certificate of Authority and filing one return for all, this isn't the right form for you.

- Misconception 4: It's unnecessary to file a return if your plans change or you don't make sales.

Contrary to this belief, once you apply for a Certificate of Authority using Form DTF-17 and specify your business start date, you’re obligated to file a return for that filing period even if your plans change or you don't engage in taxable sales activities.

- Misconception 5: Registering as a temporary vendor is not an option.

Many people are unaware that the DTF-17 form allows businesses expecting to make taxable sales for no more than two consecutive sales tax quarters to register as temporary vendors. This flexibility can be beneficial for seasonal businesses or vendors at fairs and markets.

- Misconception 6: All parts of the DTF-17 form must be completed by everyone.

This is incorrect. Not all sections of the DTF-17 apply to every applicant. For example, if you don’t have a tax preparer, Section H can be left blank. Similarly, certain questions within the form, such as whether you intend to accept credit cards, may not apply depending on your business operations.

Understanding these misconceptions can help ensure that your application process is smooth and compliant with New York State requirements. It's crucial for business owners to carefully read the instructions for Form DTF-17 and seek clarification when needed to avoid delays in receiving their Sales Tax Certificate of Authority.

Key takeaways

When you're preparing to apply for your New York State Sales Tax Certificate of Authority using the DTF-17 form, here are some key takeaways to guide you through the process:

- Applying online at www.nys-permits.org is strongly recommended because it's easier, reduces the likelihood of errors, and results in faster processing times.

- Applications must be submitted at least 20 days before the commencement of your business activities in New York State to ensure compliance.

- This form is versatile and should be used not only by new businesses but also by existing entities undergoing organizational changes, such as a sole proprietorship transitioning to a corporation, or businesses expanding to include new locations.

- It’s critical to accurately describe your business activities and the goods or services you plan to offer in New York State, as this information directly affects your tax liabilities and responsibilities.

- All responsible persons, including owners, officers, and partners involved in the day-to-day operations, must provide detailed personal and business information as part of the application process to ensure accurate tax reporting and compliance.

By closely adhering to these guidelines and thoroughly completing the DTF-17 form, businesses can confidently navigate the registration process, ensuring they meet all New York State requirements for sales tax collection and reporting.

Common PDF Documents

New York State Tax Rate - Child and dependent care credit calculations offer state-specific tax relief for eligible expenses.

New York Attorney General Office - A witness, anyone 18 years or older, must sign alongside the complainant to validate the Authorization section, though notarization is not needed.

Nyc Summons Ticket - It serves not only as a notification but also as a formal invitation for the defendant to participate in the legal process and defend their interests.