Free Nys Ct 245 Form in PDF

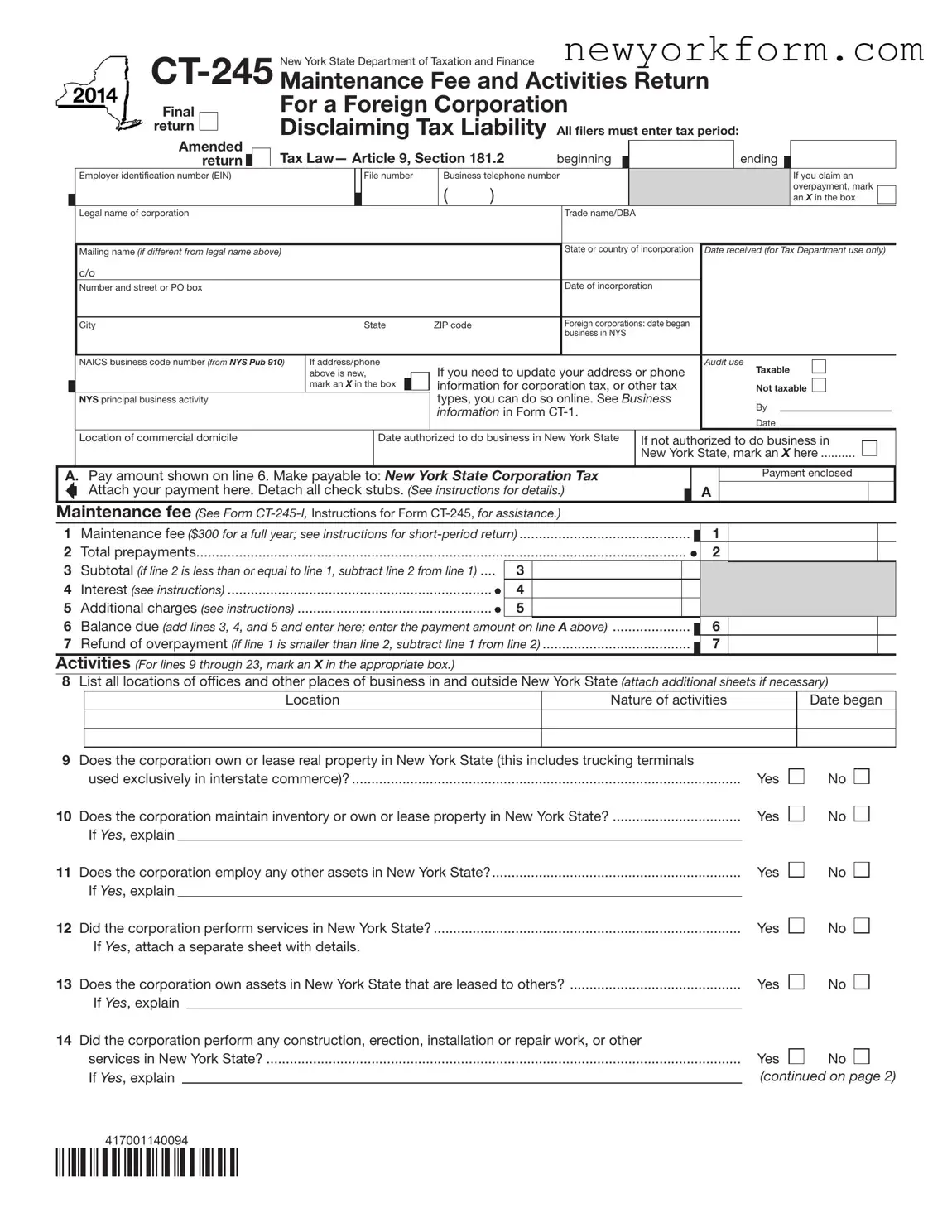

The New York State Department of Taxation and Finance CT-245 form, officially titled "Maintenance Fee and Activities Return Final for a Foreign Corporation Disclaiming Tax Liability," is a document that foreign corporations must complete and submit if they conduct business within the state but claim no taxable presence. This form encompasses a variety of sections that detail the corporation's activities, property, employment, and financial transactions within New York State. It requires the corporation to provide their Employer Identification Number (EIN), business and mailing names, and contact information, along with a declaration of the tax period concerned. Additionally, businesses need to indicate their principal activities, the date they began operations in New York, and whether they are authorized to do business in the state. A critical feature of the form is the maintenance fee section, where businesses calculate fees owed for the year—$300 for a full year, with adjustments noted for shorter tax periods—alongside any prepayments, interests, additional charges, or refunds applicable. The form also probes into the specifics of the corporation's interactions within the state, including real estate ownership or leasing, maintaining inventory or property, employee functions, and the conduct of various types of services or sales activities like petroleum products. Furthermore, the document delves into the involvement in partnerships, joint ventures, or other collaborative entities doing business within New York. The completion of this form is not only a requirement but also a certification by the authorized individuals that the information provided is true, correct, and complete, upholding the corporation's compliance with New York State Tax Law—Article 9, Section 181.2.

Nys Ct 245 Sample

|

|

|

|

New York State Department of Taxation and Finance |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|||||||||||||||||||||

|

Final |

|

|

For a Foreign Corporation |

|

|

|

|

|

|

|||||||||||

|

return |

|

|

Disclaiming Tax Liability All filers must enter tax period: |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Amended |

|

|

Tax Law— Article 9, Section 181.2 |

beginning |

|

|

|

ending |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

|

return |

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employer identiication number (EIN) |

|

|

|

|

File number |

|

Business telephone number |

|

|

|

|

|

If you claim an |

|||||||

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

overpayment, mark |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

an X in the box |

|||

|

Legal name of corporation |

|

|

|

|

|

|

|

|

|

|

|

Trade name/DBA |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Mailing name (if different from legal name above) |

|

|

|

|

State or country of incorporation |

Date received (for Tax Department use only) |

||||||||||||||

|

c/o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and street or PO box |

|

|

|

|

|

|

|

|

|

|

|

Date of incorporation |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

City |

|

|

|

|

State |

ZIP code |

|

|

Foreign corporations: date began |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

business in NYS |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

NAICS business code number (from NYS Pub 910) |

If address/phone |

|

|

|

|

|

|

|

Audit use |

|||||||||||

|

|

|

|

|

above is new, |

|

If you need to update your address or phone |

|

Taxable |

||||||||||||

|

|

|

|

|

mark an X in the box |

|

|

information for corporation tax, or other tax |

|

Not taxable |

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

NYS principal business activity |

|

|

|

|

|

|

|

types, you can do so online. See Business |

|

By |

||||||||||

|

|

|

|

|

|

|

|

|

information in Form |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

Date |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Location of commercial domicile

Date authorized to do business in New York State

If not authorized to do business in

New York State, mark an X here ..........

A. Pay amount shown on line 6. Make payable to: New York State Corporation Tax |

|

|

|

Payment enclosed |

||||||||

|

Attach your payment here. Detach all check stubs. (See instructions for details.) |

|

|

A |

|

|

||||||

|

|

|||||||||||

Maintenance fee (See Form |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

............................................Maintenance fee ($300 for a full year; see instructions for |

1 |

|

|

|

|||||||

2 |

Total prepayments |

|

|

|

|

|

|

2 |

|

|

|

|

3 |

Subtotal (if line 2 is less than or equal to line 1, subtract line 2 from line 1) .... |

3 |

|

|

|

|

|

|

|

|

|

|

4 |

Interest (see instructions) |

4 |

|

|

|

|

|

|

|

|

|

|

5 |

Additional charges (see instructions) |

5 |

|

|

|

|

|

|

|

|

|

|

6 |

Balance due (add lines 3, 4, and 5 and enter here; enter the payment amount on line A above) |

|

6 |

|

|

|

||||||

7 |

......................................Refund of overpayment (if line 1 is smaller than line 2, subtract line 1 from line 2) |

7 |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Activities (For lines 9 through 23, mark an X in the appropriate box.)

8List all locations of ofices and other places of business in and outside New York State (attach additional sheets if necessary)

Location |

Nature of activities |

Date began |

|

|

|

|

|

|

|

|

|

9Does the corporation own or lease real property in New York State (this includes trucking terminals

|

used exclusively in interstate commerce)? |

Yes |

||

10 |

Does the corporation maintain inventory or own or lease property in New York State? |

Yes |

||

|

If Yes, explain |

|

|

|

11 |

Does the corporation employ any other assets in New York State? |

Yes |

||

|

If Yes, explain |

|

|

|

12 |

Did the corporation perform services in New York State? |

Yes |

||

|

If Yes, attach a separate sheet with details. |

|

||

13 |

Does the corporation own assets in New York State that are leased to others? |

Yes |

||

|

If Yes, explain |

|

|

|

No

No

No

No

No

14Did the corporation perform any construction, erection, installation or repair work, or other

services in New York State? |

Yes |

No |

|

If Yes, explain |

|

(continued on page 2) |

|

417001140094

Page 2 of 2

15Did the corporation participate in a partnership, limited liability company/partnership, or joint venture doing

business in New York State? |

Yes |

16Did the oficers or employees of the corporation do any of the following in New York State?

a. |

Perform public relations activities |

Yes |

b. |

Furnish technical advice to retailers or consumers |

Yes |

c. |

Investigate claims |

Yes |

d. |

Collect accounts |

Yes |

e. |

Perform services |

Yes |

f. |

Approve or reject orders |

Yes |

g. Perform other activities (attach an explanation) |

Yes |

|

h. Coordinate or supervise, or both, the activities of a subsidiary that is taxable in New York State |

Yes |

|

If you answered Yes to any of the above questions |

|

|

|

activities, including continuity, frequency, and regularity. |

|

No

No

No

No

No

No

No

No

No

17Transportation corporations only: Did the corporation make any pickups or deliveries in New York State

during this calendar year? |

Yes |

If Yes, attach a sheet indicating the number of pickups and deliveries made and describe the total activities |

|

of the corporation in this state. |

|

No

18Is the corporation formed for or engaged in the business of extracting, producing, reining, manufacturing, or

compounding petroleum? |

Yes |

No |

19Does the corporation sell petroleum products (crude oil, plant condensate, gasoline, aviation fuel, kerosene,

|

diesel motor fuel, benzol, fuel oil, residual oil, or liqueied or liqueiable gases such as butane, ethane, or propane)? ... |

Yes |

No |

|||

|

If Yes, is any of the petroleum shipped to New York State from a location outside New York State? |

Yes |

No |

|||

20 |

Does the corporation import petroleum products into New York State for its own consumption? |

Yes |

No |

|||

21 |

Has the corporation been terminated in the state in which it was incorporated? |

Yes |

No |

|||

|

If Yes, enter date of termination |

|

|

|

|

|

22 |

Was the corporation previously subject to tax in New York State? |

Yes |

No |

|||

|

If Yes, enter date the corporation ceased doing business in New York State |

|

|

|

||

|

|

|

|

|||

23 |

Is the corporation a qualiied subchapter S subsidiary (QSSS)? |

Yes |

No |

|||

|

If Yes, enter name and federal employer identiication number of the parent corporation |

|

|

|||

24List all employees, including oficers, employed within New York State (attach additional sheets if necessary).

Name |

Title |

Date began |

Duties and responsibilities |

Compensation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Third – party

designee

(see instructions)

|

|

|

|

Designee’s name (print) |

Designee’s phone number |

||

|

|

|

|||||

Yes |

|

No |

|

|

( |

) |

|

|

|

|

|

|

|

|

|

Designee’s |

|

PIN |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certification: I certify that this return and any attachments are to the best of my knowledge and belief true, correct, and complete.

|

Printed name of authorized person |

|

Signature of authorized person |

|

Oficial title |

|

|

|

|||

Authorized |

|

|

|

|

|

|

|

|

|

|

|

person |

|

|

|

Telephone number |

|

Date |

|

||||

|

|

|

|

( |

) |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||

Paid |

Firm’s name (or yours if |

|

|

Firm’s EIN |

|

|

Preparer’s PTIN or SSN |

||||

preparer |

|

|

|

|

|

|

|

|

|

|

|

Signature of individual preparing this return |

Address |

City |

State |

ZIP code |

|||||||

use |

|||||||||||

|

|

|

|

|

|

|

|

|

|

||

only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer’s NYTPRIN |

|

Date |

|

||||

(see instr.)

See instructions for where to ile.

417002140094

File Overview

| Fact | Detail |

|---|---|

| Purpose of the Form | CT-245 is designed for a foreign corporation to report and pay a maintenance fee for the privilege of doing business in New York State. |

| Governing Law | Amended Tax Law—Article 9, Section 181.2 of the New York State Tax Law governs the CT-245 form. |

| Applicable to | Foreign corporations that are disclaiming tax liability but are still required to pay a maintenance fee for doing business in New York State. |

| Maintenance Fee | The form outlines that the maintenance fee is $300 for a full year, with provisions for short-period returns. |

| Key Activities Reporting | Corporations must disclose their business activities within New York State, including properties owned or leased, services performed, and participation in partnerships doing business in the state. |

| Refund of Overpayment | Allows foreign corporations to claim a refund for any overpayment of the maintenance fee reported on the form. |

Nys Ct 245: Usage Guidelines

Filling out the NYS CT-245 form involves providing detailed financial and business information about a foreign corporation that disclaims tax liability in New York State. This process requires attention to detail to ensure accuracy, as this information is vital for the Department of Taxation and Finance to process the return correctly. Once completed, the form helps in determining the corporation's maintenance fee or potential overpayment for the tax period specified. Following the steps below will guide one through the process of filling out the form efficiently.

- Enter the tax period's beginning and ending dates at the top of the form.

- Fill in the Employer Identification Number (EIN), file number, and business telephone number.

- Mark an X in the box if you are claiming an overpayment.

- Enter the legal name of the corporation, any trade name/DBA, and the mailing name if it differs from the legal name.

- Specify the incorporation's state or country, and provide the date of incorporation.

- Foreign corporations must indicate the date they began business in New York State (NYS).

- Fill in the NAICS business code number, which can be found in NYS Publication 910.

- If the address or phone number has changed, mark an X in the specified box to update the corporation tax or other tax types online.

- Indicate if the corporation is taxable or not taxable by marking the appropriate statement.

- Enter the amount of the maintenance fee on line 1, total prepayments on line 2, and then calculate lines 3 through 6 as instructed. Attach your payment if there is a balance due.

- For refunds of overpayment, enter the appropriate amount on line 7.

- List all New York State office locations and describe the nature and start dates of activities at each.

- Answer questions 9 through 23 by marking "Yes" or "No" and provide explanations or attach additional sheets if necessary.

- Include information about real property, service activities, asset employment, and any construction or service work in NYS.

- Detail participation in partnerships or business ventures within NYS and outline the scope of officer or employee activities.

- Respond to queries regarding petroleum business activities, if applicable.

- Indicate if the corporation has been terminated or was previously taxed in NYS and if it is a Qualified Subchapter S Subsidiary (QSSS).

- List all employees, including officers, who are employed within New York State, specifying their name, title, date they began, duties, responsibilities, and compensation.

- Designate a third-party designee, if desired, by providing the designee's name, phone number, email address, and PIN.

- The authorized individual must certify the return by printing their name, signing, providing their title, email address, telephone number, and the date.

- Complete the preparer's section, if applicable, including firm's name, EIN, preparer's PTIN or SSN, signature, address, e-mail address, and date.

- Review the instructions for specific filing locations and submit the form as directed.

After submitting the NYS CT-245 form, ensure to keep a copy for your records. Monitoring any correspondence from the New York State Department of Taxation and Finance is also crucial to promptly address any additional requests or provide further clarification, if needed.

FAQ

Frequently Asked Questions (FAQs) about the NYS CT-245 Form

- What is the purpose of the NYS CT-245 form?

The NYS CT-245 form, designated by the New York State Department of Taxation and Finance, is specifically for foreign corporations operating within New York State. Its primary purpose is to document the maintenance fee and report certain activities of the corporation for the tax period in question. Importantly, this form is utilized by foreign corporations to disclaim any tax liability while ensuring compliance with Article 9, Section 181.2 of the Amended Tax Law.

- Who is required to file the NYS CT-245 form?

This form must be filed by foreign corporations that are engaged in business activities in New York State but claim to be not taxable under the state's tax laws. It serves to update the state on the corporation’s activities and confirm payment of the annual maintenance fee. The form is also relevant for foreign corporations that need to report changes in their contact or operational information, like an address or phone number update, business commencement dates, or changes in legal or trade names.

- What are the key components of the NYS CT-245 form?

The form is comprehensive and includes several sections requesting various pieces of information:

- A section for basic information such as the corporation’s legal name, Employer Identification Number (EIN), and state or country of incorporation.

- Financial data including maintenance fee calculation and any applicable interest or additional charges.

- A detailed inquiry into the corporation’s activities within New York State, covering aspects like real property ownership, service provision, and asset leasing.

- Spaces to list employees within New York State, highlighting their roles, responsibilities, and compensation details.

- Where and how can one file the NYS CT-245 form?

The NYS CT-245 form should be submitted to the New York State Department of Taxation and Finance following the instructions given within the form. Filers are required to attach payment for the maintenance fee directly to the form, if applicable. Furthermore, for those claiming an overpayment, the form provides a specific section to indicate this and calculate the refund due. If there have been any changes to the corporation’s address or phone information, filers are encouraged to mark the respective section within the form and can update this information online. Detailed instructions are available to assist with queries related to form completion and the filing process.

Common mistakes

Filling out the New York State Department of Taxation and Finance CT-245 form, which is the Maintenance Fee and Activities Return Final for a Foreign Corporation return, can sometimes be confusing and lead to errors. Here are several common mistakes people make when completing this form:

- Incorrect filing period dates: Every filer must enter the beginning and ending dates for the tax period relevant to the return. Omitting these dates or using incorrect dates can cause significant processing delays.

- Failure to indicate if the return is amended: If you're amending a previously filed CT-245, marking the correct box is crucial. Not clearly indicating that your submission is an amended return can lead to incorrect processing of your file.

- Incomplete payment details: When you owe a maintenance fee, it's vital to ensure that the payment is correctly attached and that all the check stubs are detached as described in the instructions. Missing or incomplete payment can result in delays or penalties.

- Not updating business information: If your business address or phone number has changed, ticking the box to indicate this change is essential. Neglecting to mark this box or update your information can lead to miscommunication and potential issues with your return.

- Omitting necessary attachments: The form specifically requests additional sheets for various sections, such as detailing activities if the corporation performs services in New York State or employs assets within the state. Failing to attach these sheets can make your return incomplete.

- Incorrect certification: The section for certification demands that an authorized person verify the return’s accuracy. Submitting the form without the proper signature, printed name, title, and contact information of the certifying individual can render the submission invalid.

Additionally, here are a few other errors to avoid:

- Not fully listing all New York State activities, locations, or employees as required.

- Misclassifying the corporation’s business activities by using the wrong North American Industry Classification System (NAICS) code number.

- Forgetting to include the date the corporation began business in New York State, if applicable.

Avoiding these mistakes can help ensure that the CT-245 return is processed efficiently and accurately. Moreover, thoroughly reviewing the form’s instructions before submission can significantly reduce errors and improve the overall filing experience.

Documents used along the form

When dealing with New York State corporate taxation and compliance, businesses often find themselves in need of multiple forms and documents to accurately report and maintain their status. Specifically, for foreign entities operating within the state, the NYS CT-245 form is a fundamental document required for disclosing their tax liabilities and activities. Accompanying this form, there are various other documents that play critical roles throughout the process. Understanding these ancillary forms can be invaluable for ensuring thorough compliance and maximizing operational efficacy.

- CT-1 (Form CT-1, Corporation Tax Instructions): Provides comprehensive instructions and guidance on corporation tax requirements in New York State, serving as an essential resource for preparing corporate tax returns accurately.

- CT-3 (General Business Corporation Franchise Tax Return): Used by general business corporations to file their franchise tax returns. It details income, tax payable, and other relevant financial information.

- CT-3-S (New York S Corporation Franchise Tax Return): This form is specifically for S corporations, detailing income, deductions, and tax payable, among other required disclosures for state tax purposes.

- IT-204 (Partnership Return): Required for partnerships operating in New York State, this form reports income, losses, and other tax-related items to the state tax authority.

- CT-3M/4M (General Business Corporation MTA Surcharge Return): Required for corporations operating within the Metropolitan Commuter Transportation District (MCTD) to calculate the MTA surcharge.

- CT-400 (Estimated Tax for Corporations): Corporations must file this form to make quarterly estimated tax payments if they owe $1,000 or more in state corporation tax after subtracting credits.

- CT-5 (Request for Six-Month Extension to File): Allows corporations to request an additional six months to file their state tax return, providing extra time to gather necessary documentation and ensure accuracy.

- IT-2658 (Report of Estimated Tax for Corporate Partners): Used by partnerships to report and remit estimated tax on behalf of partners that are C corporations.

- CT-60 (Affiliated Entity Information Schedule): Relevant for corporations that are part of a combined report, this form provides information on each affiliated entity's operations and ownership.

Understanding and utilizing these forms in conjunction with the NYS CT-245 is crucial for foreign corporations to navigate the complexities of New York State's tax system effectively. Maintaining awareness of these documents ensures that businesses can remain compliant with state tax obligations, avoid penalties, and operate efficiently within New York State. For best results, consulting with a tax professional who is familiar with New York State's specific requirements can provide tailored advice and guidance tailored to your business's unique situation.

Similar forms

The Form 1120, U.S. Corporation Income Tax Return, is akin to the NYS CT-245 in that it is aimed at corporations reporting their income, gains, losses, deductions, and credits to determine their federal income tax liability. Like the NYS CT-245, Form 1120 requires detailed financial information, ensuring compliance with tax laws. Both forms play crucial roles in the financial reporting obligations of corporations, albeit at different government levels.

Form 2553, Election by a Small Business Corporation, shares similarities with the NYS CT-245 as both involve specific tax considerations for business entities. Form 2553 is used by small businesses to elect treatment as an S corporation for federal tax purposes, affecting their tax liabilities. Similarly, NYS CT-245 is concerned with the tax responsibilities of foreign corporations in New York State, highlighting the tailored nature of both documents to suit specific tax situations.

The Business Corporation Franchise Tax Return in other states often mirrors the NYS CT-245's purpose and structure by requiring out-of-state (foreign) corporations to report their activities and calculate tax obligations within those states. These forms ensure that corporations contribute to the tax revenues of states where they have significant business operations, akin to the objectives of the NYS CT-245.

Form CT-3, New York State Corporation Franchise Tax Return, is designed for business corporations operating within New York and mandates the reporting of income and calculation of franchise tax, paralleling the NYS CT-245's focus on foreign corporations. Both forms serve as tools for the New York State Department of Taxation and Finance to assess and collect tax revenues from corporations based on their activities and income within the state.

Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business, is akin to the NYS CT-245 in its focus on the activities of foreign entities within the U.S. While Form 5472 is used at the federal level to report transactions of foreign-owned corporations, CT-245 serves a similar purpose at the state level for foreign corporations operating in New York, demonstrating their roles in regulatory compliance on different governmental levels.

Form 1065, U.S. Return of Partnership Income, though primarily for partnerships, shares the commonality with NYS CT-245 of requiring detailed reporting of operational activities to calculate tax liabilities accurately. Both documents ensure that business entities report their income and activities comprehensively for tax assessment purposes, reinforcing the significance of transparency and accuracy in tax reporting.

The Annual Report filings required by the Secretary of State in many jurisdictions resemble the NYS CT-245 form in their objective to collect detailed information about the operations and status of business entities. These reports often require information on company officials, business activities, and locations, similar to what is detailed in the NYS CT-245, facilitating state oversight and compliance verification.

Form SS-4, Application for Employer Identification Number (EIN), while primarily for obtaining an EIN, shares with the NYS CT-245 the foundational aspect of identifying a business entity in the eyes of tax authorities. An EIN is crucial for tax reporting and compliance – a prerequisite for fulfilling obligations like those outlined in the NYS CT-245, emphasizing the interconnectivity of various tax-related documentation requirements.

Form IT-204-LL, New York State Partnership, Limited Liability Company, and Limited Liability Partnership Filing Fee Payment Form, is designed for certain business entities to report income, deductions, and credits. This form shares with the NYS CT-245 the fundamental requirement of tax reporting for operational entities within New York State, underscoring the state's comprehensive approach to taxing business activities.

Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding, although used primarily for individuals, relates to the NYS CT-245 by its focus on foreign entities' activities in relation to U.S. taxes. It serves to establish foreign status for withholding tax purposes, similar to how the NYS CT-245 identifies foreign corporations' activities within New York State, both aimed at correct tax identification and treatment.

Dos and Don'ts

When filling out the New York State Department of Taxation and Finance CT-245 form, it's important to follow specific guidelines to ensure accuracy and compliance. Here are things you should and shouldn't do:

Do's:Ensure that all required fields are filled out, including the tax period, legal name of the corporation, Employer Identification Number (EIN), and the maintenance fee amount.

Mark the appropriate box if you are filing an amended return to avoid confusion with the original submission.

Double-check the calculation of the maintenance fee ($300 for a full year, unless it's a short-period return which may vary) to avoid errors.

If the address or phone number has changed since your last filing, be sure to mark the designated box and provide the updated information.

Accurately list all locations of offices and other places of business, both in and outside New York State, attaching additional sheets if necessary.

Attach separate sheets with detailed explanations or descriptions for any activities marked "Yes" that require further information.

Include the payment for the maintenance fee with the form, ensuring it's correctly attached as instructed.

If claiming a refund of overpayment, carefully calculate this amount to ensure accuracy.

Sign and date the form to certify that the information provided is true, correct, and complete to the best of your knowledge.

Retain a copy of the form for your records before submitting it to the New York State Department of Taxation and Finance.

Do not leave any required fields blank. Incomplete forms may result in processing delays or rejection.

Do not guess on figures or dates. Verify all information before submitting the form to avoid potential discrepancies.

Do not mark "Yes" on activity questions without providing the required additional sheets for explanation, if applicable.

Avoid using outdated forms. Always check that you are filling out the most current version of the CT-245 form.

Do not forget to attach your payment for the balance due. Failure to do so may result in penalties.

Do not ignore the instructions for filling out the form. Each section contains specific guidelines that are crucial for correct submission.

Do not submit the form without reviewing it for errors. Take the time to double-check your entries.

Do not use pencil or non-permanent ink to fill out the form to prevent alterations after submission.

Avoid providing unnecessary or irrelevant information. Stick to the requested details to ensure clarity.

Do not delay submission beyond the filing deadline to avoid late filing penalties and interest charges.

Misconceptions

There are several misconceptions surrounding the New York State Department of Taxation and Finance CT-245 form, a Maintenance Fee and Activities Return for Foreign Corporations. Understanding these can clarify the obligations and opportunities for foreign corporations operating in New York State. Let's address and correct these misconceptions:

- Only applicable to large foreign corporations: The CT-245 form is required for all foreign corporations that do business in New York State, regardless of size. It’s a common misconception that only large corporations need to file this form.

- It's only about paying a maintenance fee: While paying the maintenance fee is a critical part of the form, the CT-245 also collects detailed information on the corporation's activities within New York State. This includes property ownership, employee details, and business activities, making it much more than just a fee submission.

- Once filed, no further compliance is required: Filing the CT-245 form is part of ongoing compliance requirements. Foreign corporations must also ensure they remain in good legal standing and comply with any other relevant tax and reporting obligations under New York law.

- Filing this form grants authorization to do business in New York: Submitting the CT-245 does not grant a foreign corporation the authorization to operate in New York State. Separate application for authority must be submitted and approved by the New York State Department of State.

- No penalties for late filing: Like with other tax forms, late filing of the CT-245 can result in interest charges, additional fees, and penalties. Keeping to the filing schedule is crucial to avoid unnecessary costs.

- Only for profit-making activities: The scope of the CT-245 is broader than just profit-oriented activities. It encompasses all qualifying activities of a foreign corporation within New York State, whether directly revenue-generating or not.

- Claiming overpayment is complicated: While tax filings can be complex, the CT-245 form includes a clear section for claiming overpayments. If an overpayment is claimed, the form directs how to indicate this, and steps to ensure a refund can be processed efficiently.

- No need to update if corporate information hasn't changed: Even if a foreign corporation's information remains the same, they must file the CT-245 annually as long as they continue to do business in New York State. It’s a common error to assume that unchanged information means no filing requirement.

Understanding and correcting these misconceptions is vital for foreign corporations to ensure compliance and avoid penalties. The CT-245 form is an essential requirement for foreign corporations doing business in New York State, encompassing more than just a maintenance fee payment and necessitating careful attention to detail and deadlines.

Key takeaways

When dealing with the New York State Department of Taxation and Finance CT-245 form, which is focused on Maintenance Fee and Activities Return for a Foreign Corporation, it's crucial to understand its unique requirements:

- Identify the form as designated for foreign corporations operating in New York State that need to report activities and maintenance fees, disclaiming tax liability under Amended Tax Law—Article 9, Section 181.2.

- Ensure accurate completion of the start and end of the tax period to comply with reporting requirements.

- Make sure the Employer Identification Number (EIN) and other corporation identifiers are accurately filled in to avoid processing delays.

- The form requires a declaration of the legal name, any trade names (DBA - Doing Business As), and the incorporation details including the state or country of origin.

- Highlight any changes in contact information by marking the designated box, to keep the corporation's records up to date with the tax department.

- Detail the corporation's primary New York State business activity, providing insight into the nature of the operations conducted within the state.

- Understand the maintenance fee payment structure, which is outlined in the form, including provisions for partial tax periods.

- Complete the section about various activities accurately — including questions about real estate ownership, employees in New York State, and business operations — which directly influence the tax liabilities.

- Provide comprehensive lists of business locations and employee details as required, which may require attaching additional sheets.

- Ensure a designated third-party designee is clearly identified, if applicable, to allow for additional communication between the tax department and representatives of the corporation.

- Accurately certify the document by having an authorized individual sign and date the form to validate the information provided is true, correct, and complete.

Upon completion, review the form and its instructions for submission details to ensure it is directed to the appropriate department for processing. Compliance with these key takeaways helps to streamline the filing process and underscores the importance of accuracy and thoroughness when dealing with state tax obligations.

Common PDF Documents

Dmv Surrender Plates - Highlights the necessary information required to surrender vehicle plates, such as license plate number and vehicle plate class.

New York Sw Management - Underlines the address and contact details of SW Management for applicants’ reference, centralizing communication channels for inquiries and submissions.