Free Nycers F351 Form in PDF

Every year, Tier 3 and Tier 4 Disability Retirees participating in the New York City Employees' Retirement System (NYCERS) face a critical responsibility: the completion and submission of the F351 form, an affidavit of Personal Service Income for the year. Primarily, this documentation plays a vital role in maintaining eligibility for continued disability benefits by detailing any personal income received outside of certain exclusions. Notably, the form excludes income such as the retiree's NYCERS pension checks, Social Security benefits, Workers' Compensation, and earnings from rental property, stocks, bonds, IRAs, and interest on bank account deposits. The inclusion of personal income from both public and private sectors makes this process comprehensive, ensuring that NYCERS receives a clear picture of the retiree's financial status. Failure to submit this affidavit (along with the appropriate accompanying documents, such as tax returns and W-2 forms) could result in the suspension of benefits—highlighting the form's importance. Moreover, it underscores the need to report accurately to avoid potential legal repercussions, as submitting false information is considered a felony under the Penal Code of the State of New York. The F351 form, therefore, is not just a routine document; it's a crucial annual submission that safeguards the retiree's financial integrity and ongoing receipt of benefits.

Nycers F351 Sample

NYCERS USE ONLY |

F351 |

|

*351*

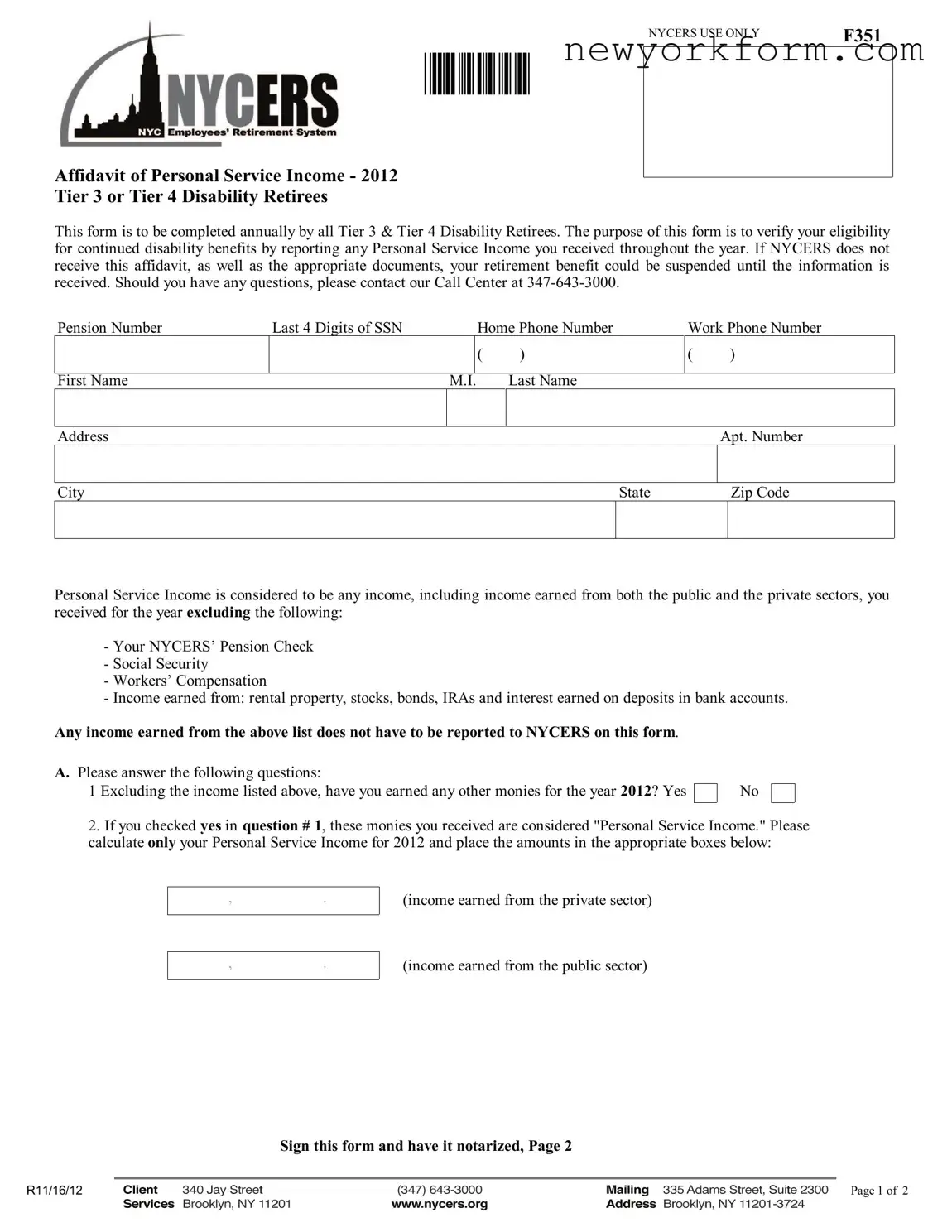

Affidavit of Personal Service Income - 2012

Tier 3 or Tier 4 Disability Retirees

This form is to be completed annually by all Tier 3 & Tier 4 Disability Retirees. The purpose of this form is to verify your eligibility for continued disability benefits by reporting any Personal Service Income you received throughout the year. If NYCERS does not receive this affidavit, as well as the appropriate documents, your retirement benefit could be suspended until the information is received. Should you have any questions, please contact our Call Center at

Pension Number |

Last 4 Digits of SSN |

Home Phone Number |

( )

Work Phone Number

()

First Name |

M.I. |

Last Name |

|

|

|

|

|

|

|

|

|

Address |

|

|

|

Apt. Number |

|

|

|

|

|

|

|

City |

|

|

State |

|

Zip Code |

|

|

|

|

|

|

Personal Service Income is considered to be any income, including income earned from both the public and the private sectors, you received for the year excluding the following:

-Your NYCERS’ Pension Check

-Social Security

-Workers’ Compensation

-Income earned from: rental property, stocks, bonds, IRAs and interest earned on deposits in bank accounts.

Any income earned from the above list does not have to be reported to NYCERS on this form.

A.Please answer the following questions:

1 Excluding the income listed above, have you earned any other monies for the year 2012? Yes

No

2.If you checked yes in question # 1, these monies you received are considered "Personal Service Income." Please calculate only your Personal Service Income for 2012 and place the amounts in the appropriate boxes below:

,.

(income earned from the private sector)

,.

(income earned from the public sector)

Sign this form and have it notarized, Page 2

R11/16/12 |

Page 1 of 2 |

NYCERS USE ONLY |

F351 |

|

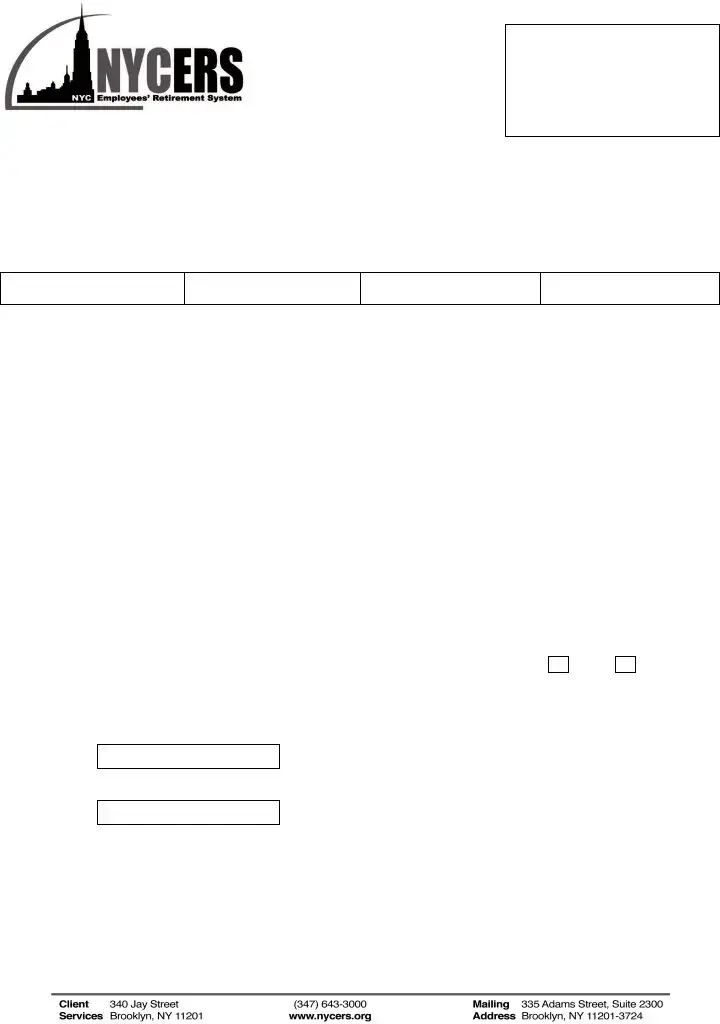

Pension Number |

Last 4 Digits of SSN |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

B. If you filed a Federal Income Tax Return for 2012, you must submit a copy of your Tax Return and your

you are married and filed a joint return, you must also submit a copy of your spouse's

I am including with this affidavit, the following:

A copy of my Federal Tax Return for the year of 2012 and my

I did not file my Federal Tax Return for the year of 2012 but I have attached my

I did not file my Federal Tax Return for the year of 2012 and I have 0.00 Personal Service Income and no

To verify my eligibility for continued benefits, I have included the required documents with this affidavit.

Signature of Member |

Date |

|

|

|

|

Pursuant to The Penal Code of the State of New York, offering a document containing false statements or false information constitutes a felony punishable by a maximum of 4 years imprisonment. All documents suspected of containing false statements will be referred to The New York City Department of Investigation for investigation.

This form must be acknowledged before a Notary Public or Commissioner of Deeds

State of |

|

County of |

|

|

On this |

|

day of |

|

|

2 0 |

|

, personally appeared |

before me the above named, |

|

|

|

|

|

|

, to me known, and known to |

|||||

me to be the individual described in and who executed the foregoing instrument, and he or she acknowledged to me that he or she

executed the same, and that the statements contained therein are true. |

If you have an official seal, affix it |

|||||

Signature of Notary Public or |

|

|||||

|

||||||

Commissioner of Deeds |

|

|||||

|

|

|

|

|

|

|

Official Title |

|

|||||

|

|

|

|

|

||

Expiration Date of Commission |

|

|||||

|

|

|

|

|

|

|

Sign this form and have it notarized, THIS PAGE

R11/16/12 |

Page 2 of 2 |

File Overview

| Fact | Detail |

|---|---|

| Form Number | F351 |

| Title | Affidavit of Personal Service Income - 2012 Tier 3 or Tier 4 Disability Retirees |

| Purpose | To verify eligibility for continued disability benefits by reporting any Personal Service Income received throughout the year. |

| Required Annually | Yes, this form must be completed annually by all Tier 3 & Tier 4 Disability Retirees. |

| Exclusions | Income not considered as Personal Service Income includes the NYCERS’ Pension Check, Social Security, Workers’ Compensation, and income from rental property, stocks, bonds, IRAs, and interest earned on deposits in bank accounts. |

| Documentation Required | A copy of the Federal Income Tax Return for 2012 and any W-2 forms received. If married and filed jointly, include W-2 forms for the spouse. |

| Consequences of Non-compliance | Retirement benefit suspension until the affidavit and appropriate documents are received by NYCERS. |

| Contact Information | NYCERS Call Center at 347-643-3000 |

| Legal Penalty for False Statements | Offering a document with false statements or information constitutes a felony, punishable by up to 4 years imprisonment under The Penal Code of the State of New York. |

Nycers F351: Usage Guidelines

Filling out the NYCERS F351 form is an essential step for Tier 3 and Tier 4 Disability Retirees to ensure their eligibility for continued disability benefits. This affidavit verifies any Personal Service Income received over the year. It is crucial to provide accurate information and include all necessary documents, as failing to do so may lead to a suspension of retirement benefits. Reporting personal service income accurately is not just a matter of compliance, but also a legal requirement, with severe consequences for false statements. Below are step-by-step instructions to complete this form accurately and efficiently.

- Start with the section labeled "NYCERS USE ONLY" and enter your Pension Number and the last 4 digits of your Social Security Number.

- Fill out your contact information, including Home Phone Number and Work Phone Number, ensuring you include the area code.

- Write your First Name, Middle Initial (M.I.), and Last Name clearly.

- Provide your Address, including Apt. Number, City, State, and Zip Code.

- Read the definitions provided under "Personal Service Income" to understand what income should be reported. Remember, income from your NYCERS’ Pension Check, Social Security, Workers’ Compensation, and certain investments like rental property, stocks, bonds, IRAs, and interest on bank deposits are excluded.

- In section A, question 1, check "Yes" or "No" to indicate if you earned any money in 2012 that does not fall under the exclusions listed.

- If you checked "Yes" in question 1, proceed to calculate your Personal Service Income for 2012 for both the private and public sectors. Place these amounts in the respective boxes provided.

- Turn to Page 2 of the form. In section B, you'll need to address your Federal Income Tax Return status for 2012. Check the statement that applies to your situation, whether you've filed the tax return and are including copies of your W-2 forms, or if you did not file taxes but are attaching any W-2 forms received.

- Sign and date the form at the bottom of Page 2. Ensure that your signature is done in front of a Notary Public or Commissioner of Deeds, who will then complete the section dedicated to their certification, including their official title and expiration date of commission.

- After completing the affidavit and having it notarized, review the document to make sure all information is accurate and that you have attached all required documents, such as your Federal Tax Return and W-2 forms, as applicable.

Once you have completed all the steps and checked your documents, it is time to submit the form to NYCERS. Make sure to follow any specific instructions for submission, including mailing addresses or online submission procedures, if available. Timely and accurate submission is crucial to avoid any delays or suspensions in your benefits. Remember, integrity and honesty in reporting your income sustain not only your compliance with regulations but uphold your legal and ethical responsibilities as a retiree receiving disability benefits.

FAQ

What is the purpose of the NYCERS F351 form?

The F351 form is designed for Tier 3 and Tier 4 Disability Retirees to report their Personal Service Income annually. This process ensures the retirees' continued eligibility for disability benefits. Failure to submit this affidavit along with the required documentation could lead to a suspension of retirement benefits.

Who needs to complete the NYCERS F351 form?

Any Tier 3 or Tier 4 Disability Retiree who has received Personal Service Income throughout the year must fill out and submit this form. This includes income earned from both the public and private sectors, excluding specific sources like the retiree's NYCERS Pension Check, Social Security, Workers’ Compensation, and income from rental property, stocks, bonds, IRAs, and bank account interest.

What documents must be submitted along with the F351 form?

Retirees need to include a copy of their Federal Income Tax Return for the year, along with their W-2 forms. If filing jointly with a spouse, retirees should also submit copies of their spouse's W-2 forms. If no tax was filed for the year, any received W-2 forms must still be submitted. If no income was earned and no tax was filed, indicating zero Personal Service Income with no W-2 forms, this should be clearly marked on the affidavit.

What happens if the F351 form is not submitted?

If NYCERS does not receive the form along with the appropriate documents, the retiree's disability benefits may be suspended. This suspension will remain in effect until the necessary information is provided and verified by NYCERS.

Is notarization required for the F351 form?

Yes, after filling out the form, the retiree must sign it in the presence of a Notary Public or Commissioner of Deeds. The form is only considered complete and valid once it has been properly acknowledged and notarized, confirming the retiree's personal service income and the truthfulness of the information provided.

Are there any legal consequences for submitting false information on the F351 form?

Yes, submitting a document that contains false statements or information can lead to legal repercussions. According to the Penal Code of the State of New York, such an act constitutes a felony punishable by up to 4 years in prison. All documents suspected of containing false information will be investigated by The New York City Department of Investigation.

Common mistakes

When filling out the NYCERS F351 form, which is essential for Tier 3 and Tier 4 Disability Retirees to verify their eligibility for continued disability benefits, certain common mistakes can lead to delays or complications in the process. Understanding and avoiding these errors is crucial to ensure smooth processing of one’s affidavit of Personal Service Income.

One common mistake is not accurately reporting all Personal Service Income that doesn't fall under the exemptions listed by NYCERS. This income includes earnings from both public and private sectors that are not already excluded by categories such as the NYCERS’ Pension Check, Social Security, Workers’ Compensation, and income from rentals, stocks, bonds, IRAs, and bank interest. Overlooking or misunderstanding what constitutes as reportable Personal Service Income can lead to inaccurately filled sections and potential problems with benefit eligibility.

Another error involves the submission of supporting documents. Applicants must include a copy of their Federal Income Tax Return for the year, along with W-2 forms. If married and filing jointly, it's required to also submit a spouse’s W-2 forms. Failing to attach these documents, or submitting incomplete records, can suspend the processing of benefits. Moreover, individuals who did not file taxes must still provide any W-2 forms received, a detail often overlooked.

- Not thoroughly completing the form, particularly by failing to answer all required questions or leaving income amounts blank.

- Misunderstanding which sources of income are to be reported and which are exempt, leading to either over-reporting or under-reporting Personal Service Income.

- Forgetting to sign the form before submission and not having it properly notarized, rendering the document unofficial and incomplete in the eyes of NYCERS.

- Omitting necessary document attachments such as the Federal Income Tax Return and W-2 forms, or in the case of not filing taxes, neglecting to state this clearly and provide any applicable W-2 forms.

- Providing inaccurate details regarding income, either by miscalculation or misunderstanding of what constitutes as income for the purposes of this affidavit, potentially leading to wrongful benefit calculation.

To avoid these mistakes, it’s important to carefully review the instructions provided with the NYCERS F351 form, double-check all filled-in information for accuracy, and ensure that all required documents are complete and attached before submission. Paying close attention to the details and requirements can save a lot of time and hassle, helping to maintain one's benefits without interruption.

Documents used along the form

The process of verifying eligibility for continued disability benefits through NYCERS involves more than just the submission of the F351 form. Individuals must often provide additional documentation to ensure their eligibility is correctly assessed and maintained. Below is a list of some commonly required forms and documents that accompany the NYCERS F351 form.

- Federal Income Tax Return: A comprehensive document reflecting the individual's income and tax filings for the year. If the individual has filed taxes, a copy of this return along with the F351 form is required to accurately report personal service income.

- W-2 Forms: Wage and tax statements provided by employers that detail the individual's earnings and taxes withheld throughout the year. These forms support the reported personal service income and are required whether or not the individual has filed a tax return.

- 1099 Forms: These forms report various types of income other than wages, salaries, and tips. They are particularly relevant for freelancers, independent contractors, and individuals receiving retirement benefits from sources other than NYCERS.

- Documentation of Workers’ Compensation: For individuals receiving workers' compensation, documentation verifying these payments is essential. It helps differentiate between personal service income and benefits not considered as such.

- Social Security Benefit Statements: These statements provide details on social security benefits received. Since social security is excluded from personal service income, providing this document clarifies total income composition.

- Proof of Disability Status: Documented evidence of an individual's disability status is critical, especially for newer applicants or cases under review. This can range from medical records to official disability determinations from other agencies.

- Marriage Certificate: In instances where an individual files joint taxes, a marriage certificate might be requested to verify the relationship and relevant tax status.

- Notarization Services: As the F351 form must be signed in the presence of a Notary Public or Commissioner of Deeds, the engagement of notarization services becomes a necessary part of the submission process.

Each of these documents plays a vital role in ensuring that individuals accurately report their income and maintain eligibility for their disability benefits. The complexity of each case can vary, and thus, the need for additional forms or documentation can arise. Facilitating this process effectively guarantees that benefits are distributed fairly and accurately, aligning with the purpose of the NYCERS system to support those in need.

Similar forms

The IRS Form 1040, the U.S. Individual Income Tax Return, shares similarities with the NYCERS F351 form in its function of reporting income. While the IRS Form 1040 encompasses a broader scope, requiring details on all taxable income for the year, the F351 specifically targets disability retirees to affirm their eligibility for benefits by disclosing personal service income. Both documents necessitate accuracy and honesty, with severe penalties for misrepresentation. Furthermore, the requirement to attach supporting W-2 forms for verification parallels the F351’s stipulation for accompanying tax returns and W-2s to validate reported earnings.

Form SSA-1099, the Social Security Benefit Statement, serves a different purpose but is connected in concept to the F351 form. This document outlines the Social Security benefits received, which are excluded from personal service income on the F351. SSA-1099 highlights government-provided income, whereas the F351 form allows disability retirees to report earned income, distinguishing between public and private sector earnings. Both forms contribute to the overall financial assessment of individuals, ensuring correct benefit and tax calculations.

The W-2 Form, the Wage and Tax Statement, directly correlates with information required in the F351 form. It presents a detailed account of an employee's annual wages and taxes withheld, similar to how the F351 gathers information on personal service income. Recipients use the W-2 to report their income, fitting into the F351's structure by providing evidence of earned income outside of excluded categories. This verification aids NYCERS in determining the accuracy of the income reported and the rightful eligibility for disability benefits.

The SSDI (Social Security Disability Insurance) Benefits form also bears resemblance to the NYCers F351 form in its aim to assess eligibility for benefits based on income. However, the SSDI form's focus is on determining eligibility for federal disability benefits by evaluating one's inability to work due to a medical condition. The linkage comes through the scrutiny of income and its impact on benefit eligibility, a core concern of both documents, although they pertain to different systems of benefits—the former to federal disability insurance, and the latter to city retirement benefits.

The 1099-MISC form, used to report miscellaneous income, extends the reporting scope beyond traditional employment wages, encompassing freelancing, contracting, or other non-employee compensation. This form's relevance to the F351 comes into play when individuals receiving disability retirement benefits from NYCERS earn money outside the realms of regular employment that must be reported. Both documents serve to ensure a comprehensive income reporting, ensuring that benefits are allocated based on accurate financial pictures.

The Unemployment Compensation Benefit Notice parallels the F351's efforts to report and assess income. This notice details the amount of unemployment benefits received, which, similarly to certain incomes reported on the F351, may affect the eligibility for other financial benefits. While the F351 form focuses on earned income during retirement for disability, both documents address the need to report income changes that could impact financial support levels from government or public entities.

Pension Benefit Statements from private or other public sector pensions offer a reporting mechanism comparable to the F351 form. These statements detail the income retirees receive from their pension plans, aiding in their financial planning. The correlation to the F351 form arises from the shared goal of providing a clear understanding of retirement incomes which, albeit from different sources, contribute to the overall financial status of a retiree. Both necessitate full disclosure of income sources to maintain transparency and accuracy in benefits allocation.

Lastly, the Worker's Compensation Benefit Verification form is somewhat analogous to the F351, as both involve reporting income that could affect eligibility for benefits. Worker's Compensation benefits, explicitly excluded from the F351's reportable income, represent another form of support for individuals unable to work due to injury. The requirement to report such incomes or, in the case of the F351, specifically exclude them, underscores the comprehensive effort to gauge financial status accurately, ensuring fair and appropriate distribution of benefits based on total income.

Dos and Don'ts

When it comes to filling out the NYCERS F351 form, which is a crucial document for Tier 3 and Tier 4 Disability Retirees, there are specific steps you should follow to ensure everything is completed accurately. This document is key to verifying your eligibility for continued disability benefits by reporting any Personal Service Income received throughout the year. Here’s a guide to help you navigate the process.

Things You Should Do:

- Review the instructions carefully before you start filling out the form to ensure you understand what is required.

- Gather all necessary documents beforehand, including your Federal Tax Return and any W-2 forms for the year in question, to ensure you have all the information needed to fill out the form accurately.

- Answer all questions truthfully, excluding the income types specifically mentioned in the form instructions, as failing to report certain incomes can lead to penalties.

- Double-check the calculations for your Personal Service Income to ensure the amounts placed in the boxes are accurate.

- Ensure the form is notarized, as this is a crucial step in the process. Your submission will not be considered valid without notarization.

- Keep a copy of the completed form and all accompanying documents for your records.

- Submit the form and documents before the deadline to avoid any interruptions to your benefits.

Things You Shouldn't Do:

- Don’t leave any sections incomplete. If a section does not apply, mark it accordingly to indicate it was not overlooked.

- Avoid guessing on income amounts; use your documents to report exact figures.

- Don’t ignore the exclusions list when reporting your income. Income such as your NYCERS’ Pension Check, Social Security, etc., should not be included.

- Do not submit the form without having it notarized, as it is a required step for the affidavit to be accepted.

- Resist the urge to wait until the last minute to fill out and send your form. Procrastination may lead to rushed errors or missed deadlines.

- Don’t forget to sign and date the form in the designated area, as an unsigned form is incomplete.

- Never provide false information, as doing so is a serious offense that can lead to penalties, including imprisonment.

By following these do’s and don’ts, you can ensure a smoother process in completing and submitting your NYCERS F351 form, aiding in the continued receipt of your disability benefits without interruption or issue.

Misconceptions

There are several common misconceptions regarding the NYCERS Form F351, which is vital for Tier 3 and Tier 4 Disability Retirees. Understanding these misconceptions is crucial for ensuring compliance and maintaining one's benefits without unwarranted interruptions. Below are nine clarifications on widespread misunderstandings:

- Misconception #1: Filing this form is optional for those who believe they have not earned any Personal Service Income. In reality, all Tier 3 and Tier 4 Disability Retirees are required to complete this form annually, regardless of whether they've earned additional income or not.

- Misconception #2: All types of income must be reported on the F351. This is incorrect; the form specifically excludes certain types of income such as Social Security benefits, NYCERS’ Pension Checks, Workers’ Compensation, income from rental property, stocks, bonds, IRAs, and interest earned on deposits in bank accounts.

- Misconception #3: Filing a Federal Income Tax Return negates the need to file Form F351. Despite one's tax filing status, the F351 form must be submitted annually to report any Personal Service Income not accounted for in one's tax return.

- Misconception #4: Married individuals can report combined income on a single Form F351. Each retiree must submit their own form, even if they filed a joint tax return. If married and filing jointly, the spouse’s W-2 forms must also be attached, if applicable.

- Misconception #5: The income threshold for reporting on this form is unclear. In fact, there is no minimum threshold; all Personal Service Income outside the specified exclusions must be reported, regardless of amount.

- Misconception #6: Digital submission of this form is acceptable. Currently, the form must be signed, notarized, and submitted in hard copy form to ensure the retiree’s compliance with NYCERS requirements.

- Misconception #7: Non-compliance with filing the F351 has no legal consequences. On the contrary, failure to submit the form or providing false information constitutes a felony, which can lead to imprisonment of up to four years.

- Misconception #8: F351 only needs to be filed if contacted by NYCERS. This form must be submitted annually without prompt from NYCERS as part of the mandatory reporting obligations for all Tier 3 and Tier 4 Disability Retirees.

- Misconception #9: Past submission of the F351 guarantees no need for future submissions. Every year presents a new obligation to reconfirm eligibility for continued disability benefits through the submission of an updated F351 form.

Understanding the importance of the NYCERS Form F351 and dispelling common misconceptions ensures that Tier 3 and Tier 4 Disability Retirees comply with reporting requirements, thus avoiding unnecessary disruptions to their benefits. Clarity on these matters supports retirees in their ongoing eligibility and underscores the significance of accurate and timely submissions.

Key takeaways

Completing and using the NYCERS F351 form accurately is essential for Tier 3 and Tier 4 Disability Retirees to maintain their eligibility for continued disability benefits. Here are key takeaways to ensure compliance and avoid potential suspension of benefits:

- Annual submission of the F351 form is required for all Tier 3 and Tier 4 Disability Retirees to report Personal Service Income.

- Personal Service Income includes income earned from both the public and private sectors but excludes pension checks from NYCERS, Social Security benefits, Workers’ Compensation, and income from rental property, stocks, bonds, IRAs, and interest on bank deposits.

- Failure to submit the form and appropriate documents may result in the suspension of retirement benefits until the requested information is provided.

- Verification of Personal Service Income requires disclosure of income not listed as exclusions, and this information must be calculated and reported for the specified year.

- The form requires notarization; thus, after completion, it must be signed in the presence of a Notary Public or Commissioner of Deeds.

- If a Federal Income Tax Return was filed for the year in question, copies of the return and all W-2 forms received should be submitted with the F351 form. This includes W-2 forms of a spouse if a joint return was filed.

- For those who did not file a tax return for the specified year but received W-2 forms, these forms must still be submitted to verify income.

- For individuals who did not file a tax return and have no Personal Service Income or W-2 forms to submit, acknowledgment of this status is required on the form to verify eligibility for continued benefits.

- Submitting false information on the F351 form is a serious offense that may lead to felony charges, with penalties including imprisonment for up to four years, emphasizing the importance of accurate and honest reporting.

For further assistance or clarification regarding the F351 form or the reporting process, contacting the NYCERS Call Center is recommended. Ensuring precise completion and timely submission of this form is crucial for maintaining disability retirement benefits without interruption.

Common PDF Documents

Nys S Corp Minimum Tax - Essential for regulatory compliance, the CT-245 aids foreign corporations in cataloguing their New York activities and associated maintenance fees comprehensively.

Who Has to File Income Tax - A vital document for enforcing labor laws within NYC Parks & Recreation's construction activities, ensuring fair treatment of workers.

Uft per Session Time Sheet - Contains declarations and signatures to verify the request's accuracy and compliance.