Free Nycers F321 Form in PDF

The NYCERS F321 form serves as a vital tool for New York City Employees' Retirement System (NYCERS) members who wish to transfer their accumulated salary deductions—including accrued interest—to another retirement system within New York State. This document outlines the process and requirements for such a transfer, emphasizing the member's intent to release NYCERS from any liabilities associated with the transferred funds. Furthermore, the form plays a critical role for members transitioning between public service positions, allowing them to carry over their financial contributions to their new retirement system, thus preserving their pension rights and benefits. Specifically, the form addresses Tier 2 and Tier 4 members who took part in special programs under Chapter 96 of the laws of 1995, offering them a chance to reclaim additional member contributions. To complete the transfer, members must authorize NYCERS to issue a check to their new retirement system, providing pertinent information such as membership numbers and employment details, both past and current. Proper completion and notarization of the form are essential steps in initiating the transfer process, ensuring the member's requests are accurately documented and legally recognized.

Nycers F321 Sample

NYCERS USE ONLY |

F321 |

|

*321*

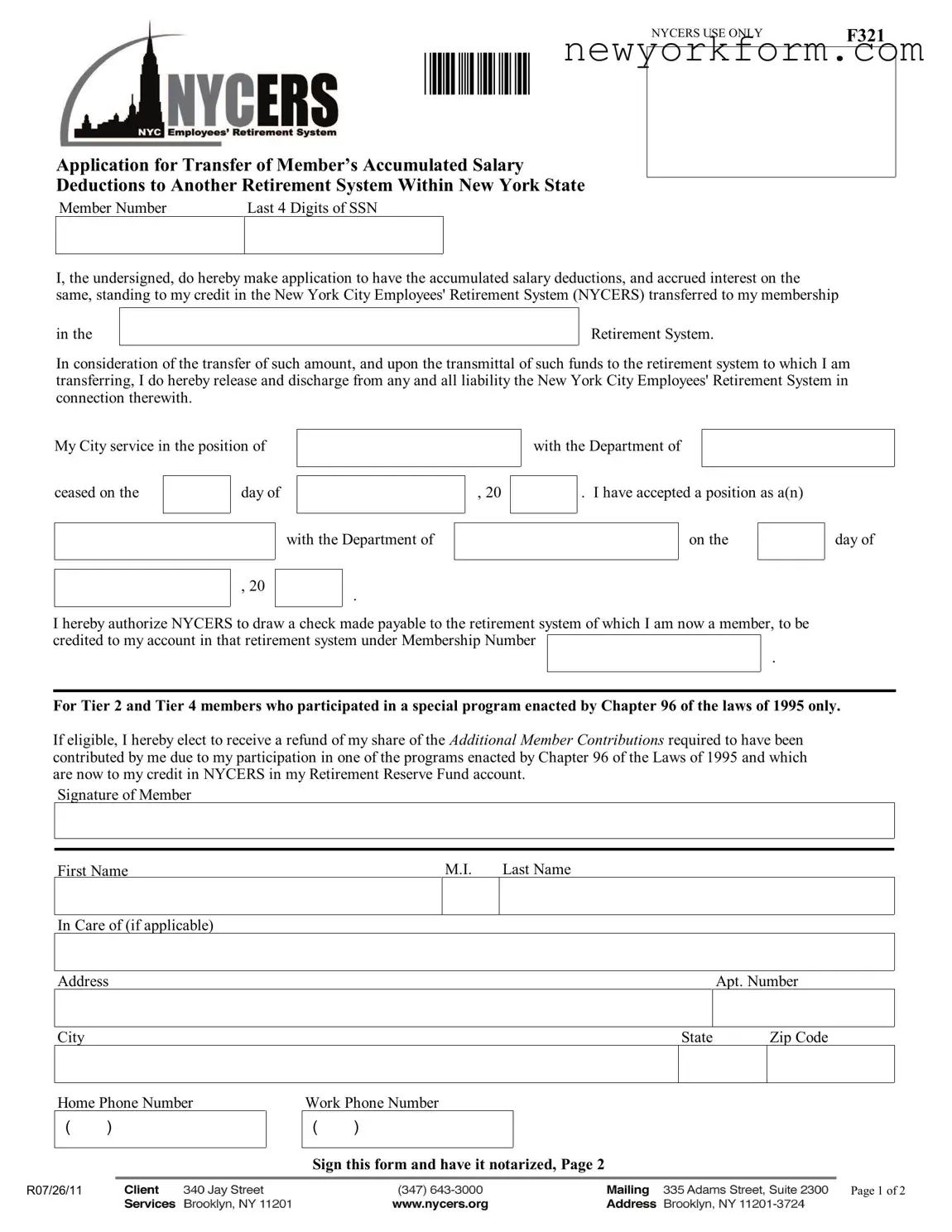

Application for Transfer of Member’s Accumulated Salary

Deductions to Another Retirement System Within New York State

Member Number Last 4 Digits of SSN

I, the undersigned, do hereby make application to have the accumulated salary deductions, and accrued interest on the same, standing to my credit in the New York City Employees' Retirement System (NYCERS) transferred to my membership

in the

Retirement System.

In consideration of the transfer of such amount, and upon the transmittal of such funds to the retirement system to which I am transferring, I do hereby release and discharge from any and all liability the New York City Employees' Retirement System in connection therewith.

My City service in the position of

ceased on the |

|

day of |

|

|

|

with the Department of

, 20

.

, 20

with the Department of

.I have accepted a position as a(n)

on the

day of

I hereby authorize NYCERS to draw a check made payable to the retirement system of which I am now a member, to be credited to my account in that retirement system under Membership Number

.

For Tier 2 and Tier 4 members who participated in a special program enacted by Chapter 96 of the laws of 1995 only.

If eligible, I hereby elect to receive a refund of my share of the ADDITIONAL MEMBER CONTRIBUTIONS required to have been contributed by me due to my participation in one of the programs enacted by Chapter 96 of the Laws of 1995 and which are now to my credit in NYCERS in my Retirement Reserve Fund account.

Signature of Member

First Name |

M.I. |

Last Name |

|

|

|

In Care of (if applicable)

Address |

|

|

Apt. Number |

|

|

|

|

|

|

City |

State |

|

Zip Code |

|

|

|

|

|

|

Home Phone Number

()

Work Phone Number

()

Sign this form and have it notarized, Page 2

R07/26/11 |

Page 1 of 2 |

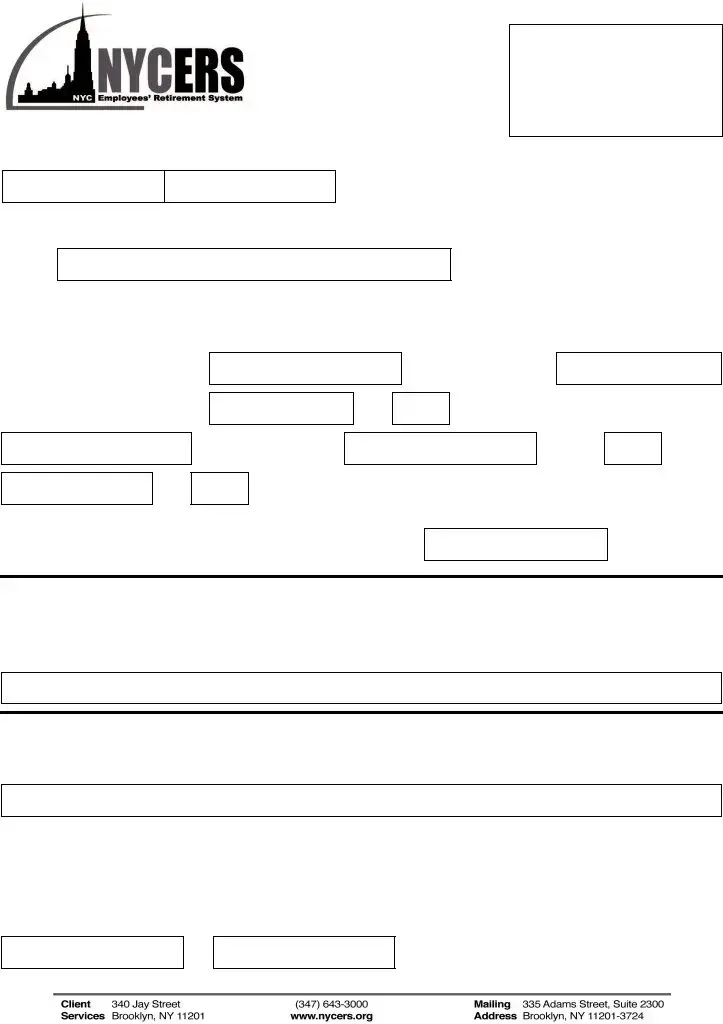

NYCERS USE ONLY |

F321 |

|

Member Number |

Last 4 Digits of SSN |

|

|

Signature of Member |

Date |

|

|

|

|

This form must be acknowledged before a Notary Public or Commissioner of Deeds

State of |

|

County of |

|

|

On this |

|

day of |

|

|

2 0 |

|

, personally appeared |

before me the above named, |

|

|

|

|

|

|

, to me known, and known to |

|||||

me to be the individual described in and who executed the foregoing instrument, and he or she acknowledged to me that he or she

executed the same, and that the statements contained therein are true. |

If you have an official seal, affix it |

||||

Signature of Notary Public or |

|

||||

|

|||||

Commissioner of Deeds |

|

||||

|

|

|

|

|

|

Official Title |

|

||||

|

|

|

|

|

|

Expiration Date of Commission |

|

||||

|

|

|

|

|

|

Sign this form and have it notarized, THIS PAGE

R07/26/11 |

Page 2 of 2 |

File Overview

| Fact | Detail |

|---|---|

| Form Name | F321 Application for Transfer of Member’s Accumulated Salary Deductions |

| Usage | Used by members of the New York City Employees' Retirement System (NYCERS) to transfer accumulated salary deductions and interest to another retirement system in New York State. |

| Applicable Members | For Tier 2 and Tier 4 members who participated in special programs enacted by Chapter 96 of the laws of 1995. |

| Form Requirement | Requires member signature and notarization. |

| Governing Law | Chapter 96 of the Laws of 1995, New York State |

| Release and Discharge | Members release and discharge NYCERS from any liability upon transfer of funds to the new retirement system. |

| Additional Contributions Refund | Eligible members can elect to receive a refund of additional member contributions required by Chapter 96 of the laws of 1995. |

| Form Revision Date | R07/26/11 |

Nycers F321: Usage Guidelines

When it comes time to transfer one's accumulated salary deductions from the New York City Employees' Retirement System (NYCERS) to another retirement system within New York State, the submission of the F321 form is required. This process involves the careful completion of the form, ensuring that all information is accurate and clearly written. The form contains sections that must be filled out by the member and then notarized to validate its authenticity. Following the provided steps ensures that the process is smooth and the transmission of funds to the new system is executed without delay.

- Start by filling out the Member Number and the last four digits of your Social Security Number (SSN) at the top of the form where indicated.

- In the section provided, print your name (First Name, Middle Initial, Last Name) clearly. If applicable, include the 'In Care of' name.

- Enter your complete address, including the apartment number if applicable, city, state, and zip code.

- Provide both your home and work phone numbers, including area codes.

- Fill in the details of your employment with NYCERS, including your position, the department you were with, and the date your service ceased.

- Next, provide the details of your new position, including the job title, the date you accepted the position, and the department it falls under in the new retirement system.

- If you participated in a special program enacted by Chapter 96 of the laws of 1995, and you're eligible, check the box to elect to receive a refund of your share of the additional member contributions.

- Sign and date the form in the presence of a Notary Public or Commissioner of Deeds. The 'Signature of Member' line needs your signature, and the adjacent line requires the date you signed the form.

- The Notary Public or Commissioner of Deeds must fill in the state and county, sign and title at the bottom of the form, including the date of acknowledgment. If the notary has an official seal, it should be affixed to the form.

After completing the above steps, the notarized form should then be sent to NYCERS as directed. It is crucial to keep a copy of the form for personal records. This formal request initiates the transfer of your accumulated salary deductions and accrued interest to your new retirement system membership. Ensuring accuracy and thoroughness during the completion process facilitates a smooth transition and helps avoid potential delays or complications.

FAQ

What is the purpose of the NYCERS F321 form?

The NYCERS F321 form is used to transfer a member's accumulated salary deductions and accrued interest from the New York City Employees' Retirement System (NYCERS) to another retirement system within New York State. This includes releasing and discharging NYCERS from any liability upon the transfer of funds to the new retirement system.

Who needs to complete the NYCERS F321 form?

Members of NYCERS who have ceased their City service and have accepted a position that qualifies them for membership in another New York State retirement system need to complete this form to transfer their accumulated salary deductions and interest.

What information is required to fill out the F321 form?

Members must provide their member number, the last 4 digits of their SSN, full name, address, phone numbers, and specific details about their employment transition. This includes the department they left, the date their city service ceased, and the new position they have accepted including its start date.

Is there any special provision for Tier 2 and Tier 4 members on the F321 form?

Yes, for Tier 2 and Tier 4 members who participated in a special program enacted by Chapter 96 of the laws of 1995, there is an option to elect a refund of additional member contributions required by their participation in the program, which are credited in their Retirement Reserve Fund account at NYCERS.

How does a member authorize the transfer of funds?

By completing and signing the F321 form, a member authorizes NYCERS to draw a check made payable to the new retirement system, to be credited to their account under the provided membership number.

What is the process to submit the NYCERS F321 form?

The form must be signed by the member and acknowledged before a Notary Public or Commissioner of Deeds. Once notarized, it should be submitted to NYCERS for processing.

Does the form require notarization?

Yes, the F321 form requires notarization. The member's signature must be acknowledged before a Notary Public or Commissioner of Deeds to ensure the form's authenticity and the member's identity.

What happens after the form is submitted?

Upon submission and approval, NYCERS will proceed with the transfer of the specified accumulated salary deductions and accrued interest to the member’s new retirement system. This finalizes the member's release and discharge of NYCERS from any liability associated with these funds. Members should follow up with their new retirement system to confirm the credit of transferred funds to their account.

Common mistakes

Filling out the NYCERS F321 form, a crucial document for transferring accumulated salary deductions to another retirement system within New York State, often seems straightforward. However, common mistakes can lead to delays or complications in processing. Here are nine typical errors people encounter:

- Failing to include the last four digits of the Social Security Number (SSN). This information is essential for identity verification and ensuring the accuracy of the transfer.

- Overlooking the member number. Both the NYCERS member number and the membership number for the new retirement system are vital for proper credit to the member's account in the new system.

- Omitting the exact date of service cessation with the New York City Department of the previous position. Precise dates are necessary for accurate record-keeping and processing.

- Negotiating the details of the new position, including the start date and the department it falls under. This information is crucial for establishing eligibility and the commencement of contributions in the new system.

- Incorrectly stating eligibility or misunderstanding the section regarding the refund of additional member contributions for special programs enacted by Chapter 96 of the laws of 1995. Misinterpretation here can affect financial outcomes.

- Leaving the signature of the member blank. A signature is a mandatory step to validate the request and confirm the member's agreement to the terms of the transfer.

- Not having the form notarized. Proper notarization is a legal requirement to authenticate the document, and lacking this can invalidate the entire application.

- Forgetting to provide a complete address, including the apartment number if applicable. This oversight can lead to issues in receiving correspondence related to the transfer.

- Providing outdated or incorrect phone numbers. Active, accurate contact information ensures that any queries or requirements for additional information can be promptly addressed.

Avoiding these mistakes not only streamlines the process but also reduces the stress and potential delay in having one's accumulated salary deductions transferred to a new retirement system within New York State. It's strongly recommended for individuals to review their application thoroughly, cross-checking all provided information and requirements before submission.

Understanding the significance of each section and instruction on the NYCERS F321 form is the first step toward a successful transfer. A meticulous approach, attention to detail, and adherence to procedures can make a substantial difference in the ease and speed with which such financial transitions are managed.

Documents used along the form

When completing the NYCERS F321 form, an application for the transfer of a member's accumulated salary deductions to another retirement system within New York State, there are several other forms and documents that you might need to submit along with it. These documents ensure that your application is processed efficiently and correctly by providing additional necessary information. Understanding what these documents are and their purpose can significantly streamline the transfer process.

- Birth Certificate: Used to verify the age of the member which can be crucial for determining eligibility and benefits in the new retirement system.

- Marriage Certificate (if applicable): Required for verifying marital status, which may affect beneficiary designations and survivor benefits in the new retirement system.

- Divorce Decree (if applicable): Necessary for updating beneficiary information and ensuring that any division of retirement benefits outlined in the decree is executed.

- Designation of Beneficiary Form: Allows members to designate or update their beneficiaries in the new retirement system.

- Statement of Earnings: A document that outlines a member's salary history, which can be critical for calculating contributions and benefits.

- Proof of Termination from Previous Employment: Confirms that a member has ended their service with their previous employer and is eligible to transfer their retirement accumulations.

- Application for Membership in the New Retirement System: Required to establish membership in the new system to which the funds are being transferred.

- Notarization Form: While the NYCERS F321 form itself needs to be notarized, additional documents provided may also require notarization to verify the authenticity of signatures and declarations.

Collecting and preparing these documents in advance can make the transfer process smoother and faster. Each item serves a specific purpose, from verifying personal information to ensuring that all legal and procedural requirements are met for the transfer of accumulated salary deductions. If you have any questions or need assistance with any of these forms, contacting NYCERS directly or consulting with a human resources representative from your current or former department can be helpful.

Similar forms

The F321 form for the New York City Employees' Retirement System (NYCERS) shares similarities with a Transfer of Service Credit form used in other retirement systems across various states. These forms allow employees to transfer their accumulated contributions and service credits from one retirement system to another, ensuring their benefits are not lost when they change jobs within the public sector. Both forms require personal information, employment details, and authorization for the transfer, highlighting how portable benefits can be within government employment.

Like the F321 form, a Direct Rollover Request form used by private retirement plans, such as 401(k)s or 403(b)s, facilitates the movement of retirement funds. This document ensures that employees can transfer their savings from one qualified retirement plan to another without incurring immediate taxes or penalties. Both documents require detailed account information and clear authorization from the account holder, underscoring the importance of maintaining the tax-deferred status of these assets.

The Beneficiary Designation form, often used in various retirement and life insurance policies, shares a common purpose with portions of the F321 form. It captures the member's intent on where they want their assets to go, though the latter's primary function relates to the transfer of accumulated deductions. Both forms require personal details and signatures to validate the member's wishes, ensuring that assets are directed according to the member’s instructions.

Loan Application forms from retirement systems have commonalities with the F321 form as they address the handling of a member's accumulated contributions. While the F321 form is focused on transferring funds between retirement systems, both types of documents deal with the management and use of these accumulated assets, stipulating strict conditions under which these funds can be accessed or moved.

Pension Plan Enrollment forms resemble the F321 form in that they initiate the member's relationship with a retirement benefit system. Both documents require detailed personal and employment information to establish or maintain the individual's benefits. The main difference lies in the purpose: while one is designed for joining a pension plan, the F321 facilitates the transfer of existing benefits to a different system.

Forms similar to an Application for Refund of Retirement Contributions, found in many retirement systems, mirror the option within the F321 form that allows for the refunding of additional member contributions under specific conditions. These documents manage the contributions made by members beyond the standard deductions, enabling the withdrawal or transfer of these funds under certain legal frameworks or conditions.

An Application for Disability Retirement shares a purposeful resemblance with the F321 form regarding the provision of member details and the need for authorization. However, the focus is on applying for benefits under the premise of disability rather than transferring accumulated funds. Both forms are vital in ensuring members' rights and benefits are preserved during significant personal and professional transitions.

Change of Address forms, although simpler, are crucial in the context of maintaining accurate records within retirement systems, akin to the information updates necessary for the F321 form. Ensuring current personal information is on file is essential for the administration of benefits, whether they're being transferred or maintained within the existing system. This parallels the F321 form's need for up-to-date contact details to facilitate the transfer process.

Finally, the Interfund Transfer form within investment platforms shows similarities with the F321. These forms allow investors to move assets between funds within the same platform, ensuring their investment strategies align with their changing goals. Like the F321 form, which facilitates the transfer of retirement funds for career mobility within the public sector, both documents streamline the process of reallocating assets according to the individual’s current needs.

Dos and Don'ts

When dealing with the NYCERS F321 form, an application for the transfer of a member’s accumulated salary deductions to another retirement system within New York State, it is crucial to approach the process with precision and understanding. The following outlines the recommended actions to take, as well as what to avoid, ensuring a smooth and efficient transfer process.

Do's:- Review the entire form before beginning: Ensure you understand every section and what is required.

- Gather necessary documentation beforehand: This may include your most recent pay stub, member identification, and information about the retirement system you are transferring to.

- Use black or blue ink: This is essential for clarity and to prevent any scanning issues.

- Ensure accuracy: Double-check all entered information, especially crucial details like member numbers, SSN digits, and transfer amounts.

- Sign and date the form: Your signature must be witnessed and notarized, indicating that you have attested to the truthfulness of the information provided.

- Keep a copy for your records: Before submitting the form, make a copy for your personal records.

- Consult with a financial advisor or retirement consultant if unsure: Before transferring funds, ensure this action aligns with your long-term financial goals.

- Do not overlook the notarization requirement: Failing to have your signature properly notarized can result in the rejection of your application.

- Do not use pencil or non-standard ink colors: This can cause legibility issues and may result in processing delays.

- Do not leave sections incomplete: Failure to provide all requested information can lead to delays or rejection of your transfer request.

- Do not guess on dates or figures: Inaccurate information can complicate the transfer process. If unsure, verify details before submitting.

- Do not submit without reviewing the form: Errors or omissions can be caught by taking the time to review your application prior to submission.

- Do not ignore the specific requirements for Tier 2 and Tier 4 members: If applicable, ensure you understand and meet these additional requirements.

- Do not hesitate to ask for help: If you encounter any confusion or issues, reach out to NYCERS or a legal consultant for guidance.

Misconceptions

There are several common misconceptions about the NYCERS Form F321, which is used to transfer accumulated salary deductions to another retirement system within New York State. Understanding these misconceptions can help ensure that individuals make informed decisions regarding their retirement contributions and transfers. Below are six misconceptions explained:

- The form cannot be used by all NYCERS members: One misconception is that the F321 form is available to all members of the New York City Employees' Retirement System (NYCERS). In reality, the form is specifically designed for members who are moving their accumulated salary deductions and accrued interest to another retirement system within New York State.

- The form automatically transfers employment service credit: Another misunderstanding is that completing the F321 form will automatically transfer the service credit for the time worked in the city to the new retirement system. However, the form is intended only for the transfer of accumulated salary deductions and accrued interest. Transferring service credits may require additional steps or forms.

- No fees are involved in the transfer: It is often assumed there are no costs associated with transferring accumulated salary deductions to another retirement system. While the F321 form itself does not include fees, the receiving retirement system may have its own costs or regulations regarding the acceptance of transferred funds.

- Interest stops accruing immediately upon submission of the form: Some believe that accrued interest stops the moment they submit the F321 form. The actual cessation of interest accrual depends on the processing times of NYCERS and the receiving retirement system. Interest typically continues to accumulate until the transfer is officially completed.

- The form is applicable for transfers to any retirement system outside of New York State: A common misbelief is that the F321 form can be used to transfer funds to retirement systems outside of New York State. In fact, this form is solely for transfers between retirement systems within New York State.

- A notarization is optional: Finally, there's a misconception that notarization of the F321 form is optional. The form clearly states that it must be acknowledged before a Notary Public or Commissioner of Deeds, making notarization a mandatory step for the processing and validation of the transfer request.

Understanding the specifics of the NYCERS F321 form helps prevent errors and ensures that members can effectively manage their retirement contributions when transitioning between employment within New York State's public retirement systems.

Key takeaways

Filling out and using the NYCERS F321 form is crucial for members of the New York City Employees' Retirement System (NYCERS) who intend to transfer their accumulated salary deductions to another retirement system within New York State. Here are some key takeaways to consider during this process:

- Understand the Purpose: The F321 form is specifically designed for transferring accumulated salary deductions, along with the accrued interest, from NYCERS to another retirement system within the state. This is an important step for individuals changing employment within public service sectors in New York State who wish to maintain their retirement contributions and benefits continuity.

- Eligibility for Special Programs: The form includes a provision for Tier 2 and Tier 4 members who participated in special programs enacted by Chapter 96 of the laws of 1995. These members have the option to request a refund of additional member contributions required due to their participation in these programs. Understanding and determining eligibility for such refunds or benefits is crucial before making any transfers.

- Release and Discharge Liability: By completing and submitting the F321 form, the member releasing and discharging NYCERS from any liability once the funds are transferred. This legal release is an important step in the transition process, acknowledging the transfer of financial responsibility to the receiving retirement system.

- Notarization is Required: It is mandatory for the member to sign the form and have it notarized. This legal acknowledgment ensures that the form is properly executed and the member's identity is verified, safeguarding against fraud and errors in the transfer process. Paying close attention to this step is imperative for a smooth transition.

Accurately completing the F321 form and understanding its implications are critical for NYCERS members looking to transfer their retirement contributions to another system within New York State. Ensuring eligibility, acknowledging the release of liability, and fulfilling the notarization requirement are essential steps in this process. Members are encouraged to reach out for assistance or clarification when needed to ensure a successful transfer of their accumulated salary deductions.

Common PDF Documents

Do You Have to Pay Taxes on Estate Inheritance - Helps establish the decedent's primary residence and ties to locations other than New York State.

New York State Tax Rate - A section for flexible benefits under IRC 125 allows taxpayers to report pre-tax contributions, influencing their net income.