Free Nyc Commercial Rents Tax Return Form in PDF

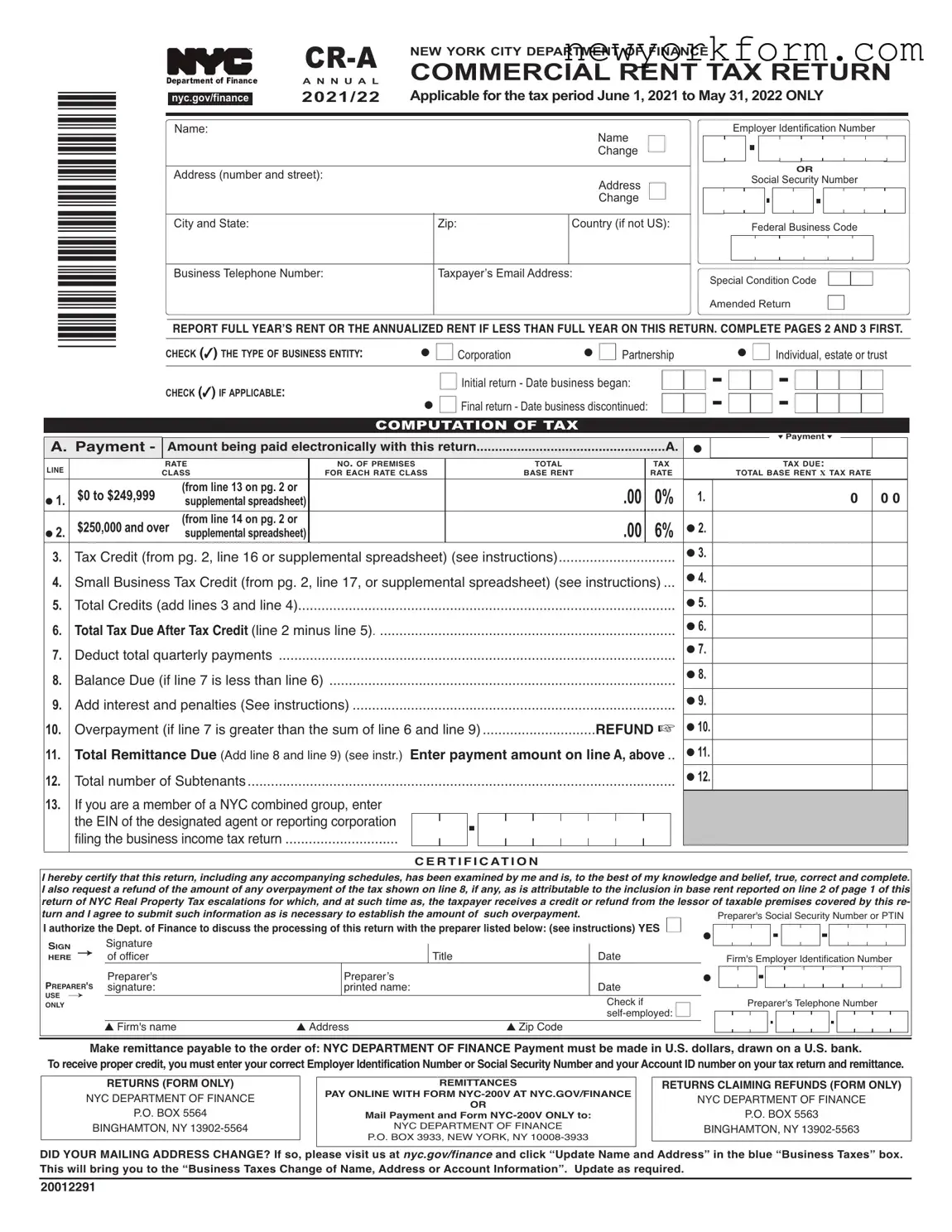

In New York City, commercial tenants are required to file an Annual Commercial Rent Tax Return, known officially as Form CR-A, for tax periods specified by the New York City Department of Finance. This form applies to the tax period from June 1, 2020, to May 31, 2021, and is designed for businesses operating within the city that pay rent for their commercial spaces. It encompasses various sections including the firm’s Employer Identification Number, the Preparer’s details, and specifics about the taxpayer's business such as name, address, and the type of business entity. Furthermore, it requires detailed information on the rent paid throughout the year or the annualized rent if the premises were not rented for the full year. The form intricately breaks down the computation of the tax due, highlighting essential elements such as base rent, rate class, tax rate, and applicable credits including a small business tax credit for eligible businesses. Additionally, it allows for amendments, indicating initial or final returns and includes a section for certification by the taxpayer. This meticulous documentation is pivotal for ensuring compliance with the city’s taxation laws on commercial rents, providing a structured outline for businesses to report their rent-related expenses accurately.

Nyc Commercial Rents Tax Return Sample

*20012291*

|

|

NEW YORK CITY DEPARTMENT OF FINANCE |

|

|

|

A N N U A L |

COMMERCIAL RENT TAX RETURN |

|

|

2021/22 |

ApplicableforthetaxperiodJune1,2021toMay31,2022ONLY |

|

nyc.gov/finance |

||

|

|

|

|

Name: |

Employer Identification Number |

|

ChangeName |

■ |

|

Address (number and street): |

OR |

|

Social Security Number |

||

ChangeAddress |

||

■ |

City and State: |

Zip: |

Country (if not US): |

|

Federal Business Code |

||||||

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Telephone Number: |

Taxpayer’s Email Address: |

Special Condition Code |

■■ |

|||||||

|

|

|

||||||||

|

|

|

Amended Return |

■ |

||||||

|

|

|

|

|

|

|

|

|

|

|

REPORT FULL YEAR’S RENT OR THE ANNUALIZED RENT IF LESS THAN FULL YEAR ON THIS RETURN. COMPLETE PAGES 2 AND 3 FIRST.

CHECK (✓)THE TYPE OF BUSINESS ENTITY: |

● ■Corporation |

● ■ Partnership |

● ■ Individual, estate or trust |

CHECK (✓)IF APPLICABLE:

■Initial return - Date business began:

● ■Final return - Date business discontinued:

COMPUTATION OF TAX

|

|

|

|

|

|

|

|

|

|

|

|

|

▼ Payment ▼ |

|

|

A. Payment - |

Amount being paid electronically with this return |

|

A. |

● |

|

|

|

|

|||||||

LINE |

|

RATE |

|

NO. OF PREMISES |

|

TOTAL |

|

TAX |

|

|

|

TAX DUE: |

|||

|

CLASS |

|

FOR EACH RATE CLASS |

|

BASE RENT |

|

RATE |

|

|

TOTAL BASE RENT X TAX RATE |

|||||

|

$0 to $249,999 |

|

(from line 13 on pg. 2 or |

|

|

|

|

.00 |

0% |

|

1. |

0 |

0 0 |

||

● 1. |

|

supplemental spreadsheet) |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$250,000 and over |

(from line 14 on pg. 2 or |

|

|

|

|

.00 |

6% |

● |

2. |

|

|

|

|

|

● 2. |

supplemental spreadsheet) |

|

|

|

|

|

|

|

|

||||||

3. |

Tax Credit (from pg. 2, line 16 or supplemental spreadsheet) (see instructions) |

|

|

● |

3. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|||||||||

4. |

Small Business Tax Credit (from pg. 2, line 17, or supplemental spreadsheet) (see instructions) |

● |

4. |

|

|

|

|

||||||||

|

|

|

|

|

|

||||||||||

5. |

Total Credits (add lines 3 and line 4) |

|

|

|

|

|

● |

5. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|||||||

6. |

Total Tax DueAfter Tax Credit(line 2 minus line 5) |

|

|

|

● |

6. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

7. |

Deduct total quarterly payments |

|

|

|

|

|

● |

7. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

8. |

Balance Due (if line 7 is less than line 6) |

|

|

|

|

|

● |

8. |

|

|

|

|

|||

......................................................................................... |

|

|

|

|

|

|

|

|

|

|

|||||

9. |

Add interest and penalties (See instructions) |

|

|

|

● |

9. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

10. |

Overpayment (if line 7 is greater than the sum of line 6 and line 9) |

REFUND ☞ |

● 10. |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||

11. |

Total Remittance Due (Add line 8 and line 9) (see instr.) Enter payment amount on lineA, above.. |

● 11. |

|

|

|

|

|||||||||

12. |

Total number of Subtenants |

|

|

|

|

|

● |

12. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

13.If you are a member of a NYC combined group, enter the EIN of the designated agent or reporting corporation filing the business income tax return .............................

CERTIFICATION

I hereby certify that this return, including any accompanying schedules, has been examined by me and is, to the best of my knowledge and belief, true, correct and complete. I also request a refund of the amount of any overpayment of the tax shown on line 8, if any, as is attributable to the inclusion in base rent reported on line 2 of page 1 of this return of NYC Real Property Tax escalations for which, and at such time as, the taxpayer receives a credit or refund from the lessor of taxable premises covered by this re- turn and I agree to submit such information as is necessary to establish the amount of such overpayment.

I authorize the Dept. of Finance to discuss the processing of this return with the preparer listed below: (see instructions) YES ■

HERESIGN |

Signature |

→ of officer |

Preparer's PREPARER'S signature:

USE →

ONLY

|

Title |

Date |

Preparer’s |

|

|

printed name: |

Date |

|

|

|

|

Check if

▲ Firm's name |

▲ Address |

▲ Zip Code |

Make remittance payable to the order of: NYC DEPARTMENT OF FINANCE Payment must be made in U.S. dollars, drawn on a U.S. bank.

Toreceivepropercredit,youmustenteryourcorrectEmployerIdentificationNumberorSocialSecurityNumberandyourAccountIDnumberonyourtaxreturnandremittance.

RETURNS (FORM ONLY)

NYC DEPARTMENT OF FINANCE

P.O. BOX 5564

BINGHAMTON, NY

REMITTANCES

PAY ONLINE WITH FORM

OR

Mail Payment and Form

NYC DEPARTMENT OF FINANCE

P.O. BOX 3933, NEW YORK, NY

RETURNS CLAIMING REFUNDS (FORM ONLY)

NYC DEPARTMENT OF FINANCE

P.O. BOX 5563

BINGHAMTON, NY

DID YOUR MAILING ADDRESS CHANGE? If so, please visit us at nyc.gov/finance and click “Update Name and Address” in the blue “Business Taxes” box. This will bring you to the “Business Taxes Change of Name, Address or Account Information”. Update as required.

20012291

Form |

Page 2 |

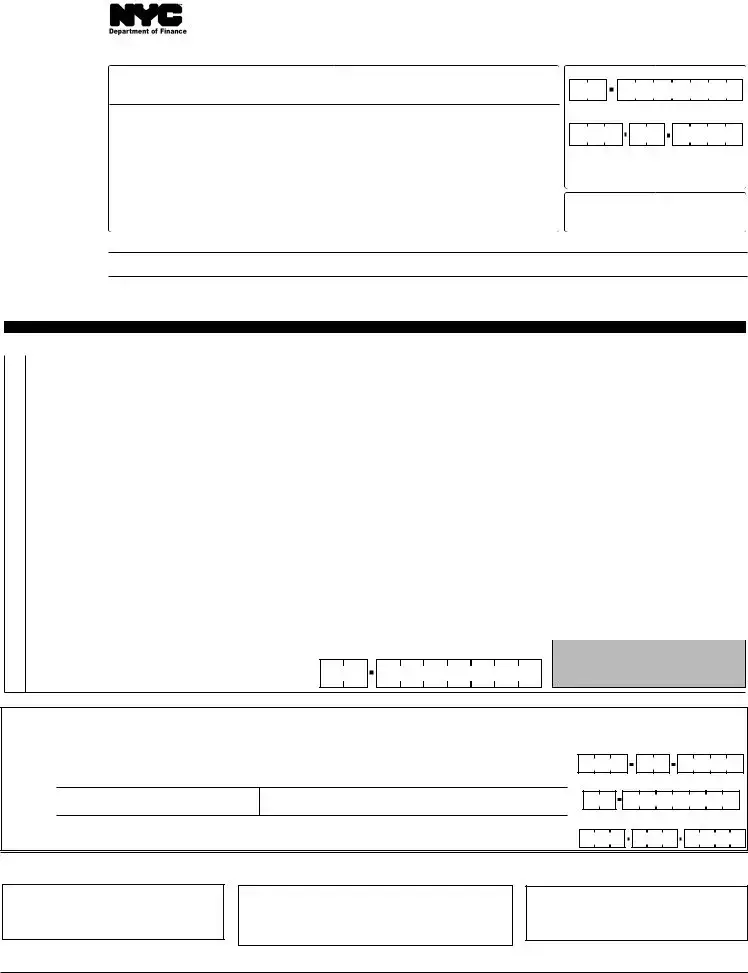

YOU MAY FILE ELECTRONICALLY AT NYC.GOV/ESERVICES. IF YOU ARE FILING ON PAPER, USE THIS PAGE IF YOU HAVE THREE OR LESS PREM- ISES/SUBTENANTS OR MAKE COPIES OF THIS PAGE IF YOU HAVE ADDITIONAL PREMISES/SUBTENANTS. IF YOU CHOOSE TO USE A SPREADSHEET, YOU MUST USE THE CRA.FINANCE SUPPLEMENTAL SPREADSHEET WHICH YOU CAN DOWNLOAD FROM OUR WEBSITE AT WWW.NYC.GOV/CRTINFO.

EACH LINE MUST BE ACCURATELY COMPLETED. YOUR DEDUCTION WILL BE DISALLOWED IF INACCURATE INFORMATION IS SUBMITTED.

LINE |

DESCRIPTION |

PREMISES 1 |

PREMISES 2 |

PREMISES 3 |

||||

● 1a. |

Street Address ................................................................ 1a. |

|

|

|

|

|

|

|

1b. |

Zip Code ..........................................................................1b. |

________________________________________________________________________________________ |

||||||

1c/d. Block and Lot Number ...............................................1c/1d. ________________________________________________________________________________________ |

||||||||

|

|

|

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

● 2. |

Gross Rent Paid (see instructions) |

2. |

________________________________________________________________________________________ |

3. |

Rent Applied to Residential Use |

3. |

________________________________________________________________________________________ |

4a1. |

SUBTENANT'S NameifPartnershiporCorporation |

|

|

|

(if more than one subtenant, see instructions) |

4a1. |

________________________________________________________________________________________ |

●4a2. Employer Identification Number (EIN) for

|

partnerships or corporations |

4a2. |

● EIN ________________________ ● EIN ________________________ ● EIN _______________________ |

|||||

4b1. |

SUBTENANT'S NameifIndividual |

4b1. |

________________________________________________________________________________________ |

|||||

4b2. |

Social Security Number (SSN) for individuals |

4b2. |

● SSN _______________________ ● SSN _______________________ ● SSN _______________________ |

|||||

4c. |

RentreceivedfromSUBTENANT |

|

|

|

|

|

|

|

|

(if more than one subtenant, see instructions) |

4c. |

___________________________________________________________________________________________________ |

|||||

4d1. |

Is this rent paid for a period less than 12 months? .. |

4d1. |

YES ■ |

NO ■ |

YES ■ |

NO ■ |

YES ■ |

NO ■ |

4d2. |

If YES, how many months? |

4d2. |

Total number of months:_______________ |

Total number of months:_______________ |

Total number of months:_______________ |

|||

5a. |

Other Deductions (attach schedule) |

5a. |

________________________________________________________________________________________ |

|||||

5b. |

Commercial Revitalization Program |

|

|

|

|

|

|

|

|

special reduction (see instructions) |

5b. |

________________________________________________________________________________________ |

|||||

6. |

Total Deductions (add lines 3, 4c, 5a and 5b) |

6. |

________________________________________________________________________________________ |

|||||

7.Base Rent Before Rent Reduction (line 2 minus line 6)...7. ________________________________________________________________________________________

4If the line 7 amount represents rent for less than the full year, proceed to line 10, or

NOTE 4If the line 7 amount plus the line 5b amount is $249,999 or less and represents rent for a full year, transfer line 9 to line 13, or 4If the line 7 amount plus the line 5b amount is $250,000 or more and represents rent for a full year, transfer line 9 to line 14

8. |

35% Rent Reduction (35% X line 7) |

8. |

________________________________________________________________________________________ |

||||||

9. |

Base Rent Subject to Tax (line 7 minus line 8) |

9. |

________________________________________________________________________________________ |

||||||

|

|

|

|

|

|

|

|

|

|

|

COMPLETE LINES 10 THROUGH 12 ONLY IF YOU RENTED PREMISES FOR LESS THAN THE FULL YEAR |

||||||||

10. |

Tenants whose rent is not paid on a monthly basis, check box |

|

■ |

■ |

■ |

||||

|

and see instructions. Others complete lines 10a through12. ... |

10. |

__________________________________________________________________________________________ |

||||||

10a. |

Number of Months at Premises during the tax period |

10a. # of months |

10b. From: |

10a. # of months |

10b. From: |

10a. # of months |

10b. From: |

||

|

|

|

|

10c. To: |

|

10c. To: |

|

|

10c. To: |

|

|

|

|

_________________________________________________________________________________________________________________ |

|

||||

11.Monthly Base Rent before rent reduction

(line 7 plus line 5b divided by line 10a) |

11. ________________________________________________________________________________________ |

12.Annualized Base Rent before rent reduction

(line 11 X 12 months or line 4 from worksheet on page 3) .12. ________________________________________________________________________________________

■If the line 12 amount is $249,999 or less, transfer the line 9 amount (not the line 12 amount) to line 13

■If the line 12 amount is $250,000 or more, transfer the line 9 amount (not the line 12 amount) to line 14

*20022291*

|

RATE CLASS |

|

TAX RATE |

|

TRANSFER THE AMOUNTS FROM LINES 13 THROUGH 16 TO THE CORRESPONDING LINES ON PAGE 1 |

|

|

|

|

|

|

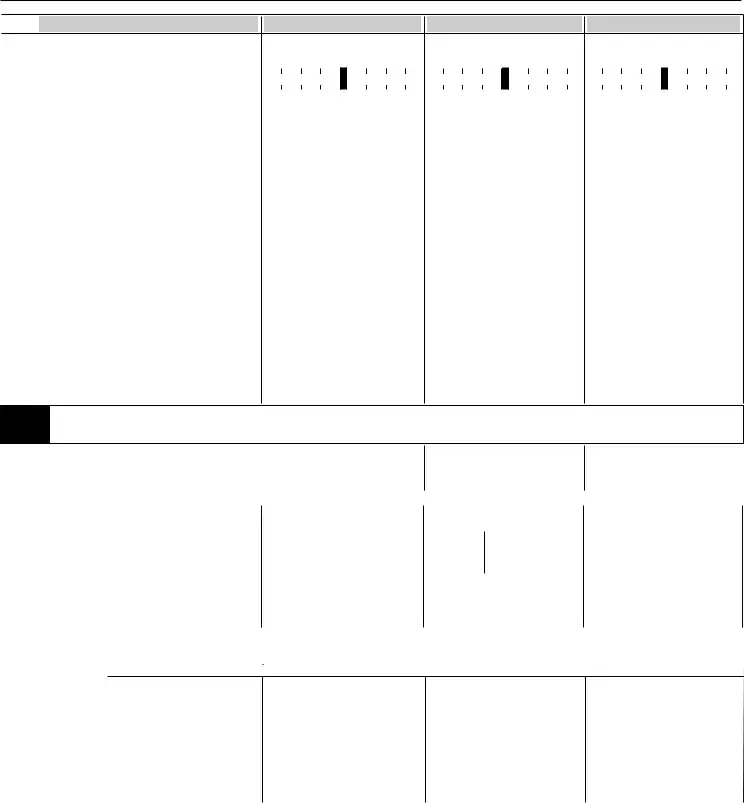

13.($0 - 249,999) .........0%.......13.________________________________________________________________________________________

14.($250,000 or more)... 6%.......14.________________________________________________________________________________________

15.Tax Due before credit

(line 14 multiplied by 6%) ........15.________________________________________________________________________________________

16.Tax Credit (see worksheet below) .16.________________________________________________________________________________________

17.Small Business Tax Credit (from pg. 3, or supplemental

spreadsheet) (see instructions)....17.________________________________________________________________________________________

Note: The tax credit only applies if line 7 plus line 5b (or line 12, if applicable) is at least $250,000, but is less than $300,000. All others enter zero.

|

|

TAX CREDIT COMPUTATION WORKSHEET |

|

■ If the line 7 amount represents rent for the full 12 month period, your credit is calculated as follows: |

|

|

Amount on line 15 |

X ($300,000 minus the sum of lines 7 and 5b) = ___________________= your credit |

|

|

$50,000 |

|

■ If the line 7 amount represents rent for less than the full 12 month period, your credit is calculated as follows: |

|

20022291 |

Amount on line 15 |

X ($300,000 minus line 12) = ___________________ = your credit |

|

||

|

|

$50,000 |

|

|

|

Form |

Page 3 |

IF YOU ARE FILING ON PAPER, USE THIS PAGE IF YOU HAVE THREE OR LESS PREMISES OR MAKE COPIES IF YOU HAVE ADDITIONAL PREMISES. IF YOU CHOOSE TO USE A SPREADSHEET, YOU MUST USE THE SUPPLEMENTAL SMALL BUSI- NESS TAX CREDIT WORKSHEET WHICH YOU CAN DOWNLOAD FROM OUR WEBSITE AT WWW.NYC.GOV/CRTINFO.

TO QUALIFY FOR SMALL BUSINESS TAX CREDIT

A. Is your "total income" as defined by Ad. Code Section |

■ YES |

■ NO |

If your answer to Question A is NO, you are not eligible for this credit. |

|

|

B. Is your "Base Rent Before Rent Reduction" (page 2, line 7) for any premises at least $250,000 but less than $550,000?...... ■ YES ■ NO

If the answer to this Question is NO for any of the premises, you are not eligible for this credit for those premises whose Base Rent

BeforeReductioniseitherlessthan$250,000 orequaltoorgreaterthan$550,000 andyoushouldnotcompletethisworksheetforthosepremises.

INCOME FACTOR CALCULATIONS - Complete either lines 1a and 1b OR lines 2a and 2b |

||||||||||||||||

1a. Enter amount of total income, if total income is $5,000,000 or less (see instructions) |

|

1a. |

______________________________________ |

|||||||||||||

1b. Income factor (see instructions) |

|

|

|

|

|

|

1b. |

______________________________________ |

||||||||

2a. Enter amount of total income if total income is more than $5,000,000 |

|

|

|

|

|

|

|

|

|

|||||||

but less than $10,000,000 (see instructions) |

|

|

|

|

|

|

2a. |

______________________________________ |

||||||||

2b. If total income is more than $5,000,000 but less than $10,000,000: |

|

|

|

|

|

|

|

|

|

|||||||

Income Factor is (10,000,000 - line 2a) / 5,000,000 |

|

2b. |

______________________________________ |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

RENT FACTOR CALCULATIONS - Complete either lines 3a and 3b OR lines 4a and 4b |

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3a. Enter amount of base rent, if base |

|

PREMISES |

|

|

|

|

PREMISES |

|

|

|

|

PREMISES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

rent from Page 2, line 7 is less |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

than $500,000 |

|

3a. |

_________________________________________________________________________________________ |

|||||||||||||

3b. Rent factor (see instructions) |

3b. |

_________________________________________________________________________________________ |

||||||||||||||

4a. Enter amount of base rent if base rent |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

from Page 2, line 7 is at least |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$500,000 but less than $550,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(see instructions) |

4a. |

_________________________________________________________________________________________ |

||||||||||||||

4b. If base rent from Page 2, line 7 is at least |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$500,000 but less than $550,000: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rent Factor is ($550,000 - line 4a) / 50,000 |

4b. |

_________________________________________________________________________________________ |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CREDIT CALCULATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5a. Page 2, line 15 (Tax at 6%) |

5a. |

_________________________________________________________________________________________ |

||||||||||||||

5b. Page 2, line 16 (Tax Credit from Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Credit Computation Worksheet on Page 2) |

5b. |

_________________________________________________________________________________________ |

||||||||||||||

5c. (line 5a - line 5b) X (line 1b or 2b) X (line 3b or 4b). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter here and on Page 2, line 17 |

5c. |

_________________________________________________________________________________________ |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WORKSHEET FOR TENANTS WHO PAY RENT FOR A PERIOD OTHER THAN ONE MONTH |

|||||||||||||||

|

To determine the annualized rent, divide the rent paid during the tax period by the number of days for which the rent was paid and multiply |

|||||||||||||||

|

the result by the number of days in the tax year. Enter the result on line 4 here and on Form |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PREMISES |

|

|

PREMISES |

|

|

|

|

PREMISES |

|

||||

*20032291* |

1. Amount of rent paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

for the period ................... 1. |

_____________________________________________________________________________________ |

||||||||||||||

|

2. Number of days in the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

rental period for which |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

rent was paid................... 2. |

_____________________________________________________________________________________ |

||||||||||||||

|

3. Rent per day (divide |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

line 1 by line 2. Round to |

|

|

|

|

|

|

|

|

|

|

|||||

|

the nearest whole dollar). 3. |

_____________________________________________________________________________________ |

||||||||||||||

|

4. Annualized rent (multiply |

|

|

|

|

|

|

|

|

|

|

|||||

|

rent per day, line 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by 365. In case of a leap |

|

|

|

|

|

|

|

|

|

|

|||||

|

year, multiply by 366. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Round to the nearest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

whole dollar).................... 4. |

_____________________________________________________________________________________ |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20032291 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

File Overview

| Fact | Detail |

|---|---|

| Form Identifier | CR-A |

| Relevant Period | June 1, 2020, to May 31, 2021 |

| Applicable Entity | New York City Department of Finance |

| Purpose | Annual Commercial Rent Tax Return |

| Governing Law | New York City Administrative Code |

Nyc Commercial Rents Tax Return: Usage Guidelines

Filling out the New York City Commercial Rent Tax Return for the tax period of June 1, 2020, to May 31, 2021, is a crucial task for businesses that are subject to this tax. This process requires careful attention to detail and accurate information entry to ensure that your business complies with local tax laws. The instructions outlined below are designed to guide you through this process step by step, helping to simplify the completion of the form and reduce the likelihood of errors.

- Start by entering your business name and indicate if there has been a change to the Employer Identification Number (EIN) or address since the last filing.

- Fill in the business address, including the city, state, zip code, and country if outside the US.

- Provide the Federal Business Code and the Business Telephone Number.

- Enter the Taxpayer’s Email Address to ensure you receive pertinent information related to your return.

- Check the applicable box for the type of business entity (Corporation, Partnership, or Individual, estate, or trust).

- If it's the first or final return, indicate the date the business began or discontinued.

- Complete the computation of tax section by filling in the payment amount being paid electronically with this return.

- Determine the total base rent and apply the correct tax rate based on the rent amount to compute the total tax due.

- Calculate and enter any tax credits, including the small business tax credit, and total them up.

- Subtract total credits from the tax due to get the total tax due after credits.

- Enter any quarterly payments made during the tax period.

- Calculate the balance due or overpayment, and add any interest and penalties if applicable.

- Provide the total number of subtenants, if applicable.

- If part of a NYC combined group, enter the EIN of the designated agent or reporting corporation.

- Sign and date the return, certifying that the information is true, correct, and complete. The preparer should also sign and date the return if applicable.

- If payment is due, make the remittance payable to the NYC Department of Finance, ensuring it is drawn on a U.S. bank and in U.S. dollars. Enter your correct EIN or Social Security Number and your Account ID number on your tax return and remittance for proper credit.

- Mail the return to the appropriate address based on whether you are making a payment or claiming a refund. For electronic payments, use Form NYC-200V available on the NYC.gov/finance website.

It's imperative to ensure that all information provided on the form is accurate and complete. An incomplete or incorrect form may result in processing delays or potential fines. For any updates or changes to business information such as mailing addresses, visit the NYC.gov/finance website.

FAQ

What is the New York City Annual Commercial Rent Tax Return (Form CR-A)?

The New York City Annual Commercial Rent Tax Return (Form CR-A) is a document that businesses leasing premises in certain parts of New York City must complete and submit to the NYC Department of Finance. This form is applicable for the tax period from June 1, 2020, to May 31, 2021. It's designed to calculate and report the tax due based on commercial rents paid. This tax is specific to businesses operating within Manhattan (south of the northern boundary of Murray Hill), and there are certain thresholds and tax rates that apply, which can result in tax credits for smaller businesses.

Who needs to file the Annual Commercial Rent Tax Return, and when is it due?

Businesses operating within the specified areas of Manhattan with an annualized rent payment over certain thresholds are required to file the Annual Commercial Rent Tax Return. This includes corporations, partnerships, individuals, estates, or trusts. The form is due annually, and for the specific tax period covered by this form (June 1, 2020, to May 31, 2021), the submission deadline would typically fall in the summer following the end of the tax period. Specific due dates can be found on the NYC Department of Finance website or by contacting them directly.

How is the tax calculated on the form?

Tax calculation involves several steps outlined in the form and depends on the total base rent paid. Initially, businesses must report their gross rents and deduct any applicable exclusions or reductions, such as rent applied to residential use or other permissible deductions. The resulting base rent is then categorized under two rate classes, with different tax rates applied: 0% for $0 to $249,999, and 6% for $250,000 and over. Small businesses may also qualify for tax credits, which can reduce the amount of tax due.

Are there any credits or deductions available?

Yes, there are deductions and credits available that can reduce the taxable amount or the tax due. These include the small business tax credit for businesses with total incomes of $10 million or less and whose base rent before rent reduction falls within a specific range. Other deductions may include rent applied to residential use and the commercial revitalization program special reduction. Detailed instructions for calculating these deductions and credits are provided in the form instructions and the supplemental worksheets available on the NYC Department of Finance website.

Common mistakes

Filling out the NYC Commercial Rent Tax Return form can be a straightforward process, but several common mistakes can lead to errors in filing. Here’s a look at nine errors people often make:

- Not updating personal and business information: Failing to update the address or name due to a change can lead to miscommunication or lost mail.

- Incorrect Employer Identification Number or Social Security Number: Mixing up these numbers or entering them incorrectly can cause significant delays or misprocessing of the return.

- Not accurately reporting the full year’s rent or the annualized rent if the premises were rented for less than a full year: This mistake can lead to incorrect tax calculations.

- Selecting the wrong business entity type: Whether the business is a corporation, partnership, or individual entity, marking the wrong type can affect tax obligations.

- Overlooking the Special Condition Codes, such as noting if the return is amended, an initial return, or a final return: Not checking the appropriate box can cause incorrect processing of the return status.

- Miscalculating tax dues: This includes errors in applying tax rates to the base rent, leading to either underpayment or overpayment of taxes.

- Failing to apply for applicable tax credits, such as the small business tax credit, when eligible: Missing out on these credits can lead to loss of potential savings.

- Incorrect calculation of subtenant information or rent received from subtenants, including failing to report this income: This can lead to inaccurate tax liability calculations.

- Forgetting to sign and date the certification section or not authorizing the Department of Finance to discuss the return with the preparer, if applicable: An unsigned or undated form is not valid and will not be processed.

Avoiding these mistakes requires careful review of the form before submission. Here are some additional tips:

- Double-check all entered information for accuracy.

- Consult the instructions for each section if there’s any uncertainty.

- Consider hiring a professional preparer if the tax scenario is complex.

Proper attention to detail can ensure the return is processed smoothly, avoiding delays and possible penalties for errors. Always keep a copy of the submitted form and any corresponding documentation for your records.

Documents used along the form

When filing a NYC Commercial Rents Tax Return form, it's critical to have a grasp of the supplementary forms and documents that might be necessary to complete the process accurately. Each document plays a specific role in confirming the details of your submission or adding additional information that can impact the computation of your tax. Here's a brief overview of several important documents often utilized alongside the Commercial Rents Tax Return.

- Form NYC-200V: This form is crucial for those opting to make their payment electronically following the submission of their Rent Tax Return. It serves as a payment voucher, ensuring that the payment is correctly applied to your account.

- Supplemental Spreadsheet for Commercial Rent Tax: For businesses with multiple premises or subtenants, this digital spreadsheet is provided by the NYC Department of Finance to accurately report and calculate rents and deductions for each location in a consolidated manner.

- Commercial Revitalization Program Deduction Sheet: If your business qualifies for deductions under the Commercial Revitalization Program, this document is used to detail and apply those benefits to reduce your taxable amounts appropriately.

- Small Business Tax Credit Worksheet: This worksheet helps small businesses determine their eligibility for tax credits and calculate the exact amount that can be deducted from their total tax. The eligibility often hinges on specific criteria such as total income and base rent before reduction.

Each document intertwined with the NYC Commercial Rents Tax Return serves to clarify, reduce, or substantiate claims that affect your final tax responsibilities. It's advisable to review the requirements and have these forms at hand before starting your tax return process to ensure a smooth and accurate filing experience.

Similar forms

The New York City Commercial Rent Tax Return (CR-A) form shares similarities with the IRS Form 1120, U.S. Corporation Income Tax Return. Both forms are designed for entities to report their financial activities to a governing tax authority, with the CR-A specifically for commercial tenants in New York City and Form 1120 for corporations operating within the United States. While the CR-A focuses on rent paid for commercial space, Form 1120 covers a broader spectrum of corporate financial activities, including income, gains, losses, deductions, and credits. Each form requires detailed financial information to accurately calculate the tax liability, offering deductions and credits specific to their respective regulatory frameworks.

Similar to the Schedule E (Form 1040), Supplemental Income and Loss, the CR-A form is used by taxpayers to report income and expenses related to a specific category of taxable activity. Schedule E is utilized by individuals to report rental income from real estate, along with royalties, partnerships, S corporations, estates, and trusts. Both forms allow for the deduction of expenses incurred in the operation of the reported activity, such as rent, utilities, and maintenance for Schedule E, compared to the rent paid on commercial space for the CR-A. The primary distinction lies in the type of taxpayer and income source: Schedule E is for individual taxpayers with supplementary income sources, whereas the CR-A targets businesses operating within commercial real estate in NYC.

The Sales and Use Tax Return forms, found in various states, resemble the NYC Commercial Rent Tax Return (CR-A) in their purpose to collect tax on business activities, though focusing on sales transactions rather than rent. These forms calculate tax due based on the value of goods and services sold within the state's jurisdiction, applying a percentage rate similar to how the CR-A applies a rate to the base rent of commercial properties. Both forms contribute to local government revenues but diverge in their tax bases, with sales tax forms affecting a broader range of businesses through sales activities versus the more specific scope of commercial tenants under the CR-A.

Comparable to the CR-A, the Property Tax Return forms used by municipalities across the country aim to assess tax based on the value of property or use of space. Property tax returns often require the property owner to declare the value of real property, which is then used to determine tax liability. While both the CR-A and property tax returns involve real estate, the CR-A is unique to commercial renters in New York City, focusing on rented space rather than property ownership. The distinction highlights how different tax forms address various participants in the real estate market—from owners reporting property values to commercial renters reporting leased space usage.

The Unincorporated Business Tax (UBT) Return, specific to certain localities, shares similarities with the CR-A by targeting business activities, although the UBT is levied on the income of unincorporated businesses. Like the CR-A, the UBT Return requires detailed reporting of business operations to calculate tax owed, albeit on business income instead of rent. Both forms are designed to ensure businesses contribute to the local tax base, with the key difference being the CR-A's focus on the commercial rental sector versus the broader application of the UBT to unincorporated businesses’ income. This variance illustrates the tailored approaches municipalities use to tax different facets of business operations.

Dos and Don'ts

When filling out the New York City Commercial Rent Tax Return form, certain practices can facilitate the process and minimize errors. Below is a compiled list of dos and don'ts:

- Do ensure that all the firm and preparer identification numbers, including the Employer Identification Number and Preparer’s Tax Identification Number, are accurately reported.

- Do thoroughly check the type of business entity and mark the applicable box clearly; accurate identification affects tax calculation.

- Do accurately report the full year's rent or the annualized rent if the premises was rented for less than a full year, to ensure proper tax computation.

- Do include accurate computation of all applicable credits such as Small Business Tax Credit to reduce the total tax due.

- Do confirm the accuracy of all deductions claimed, including subtenant rents and any applicable special reductions, as inaccuracies can lead to deductions being disallowed.

- Don't overlook the need to complete supplemental spreadsheets for premises if you have more than what a single form allows or qualifies for specific credits; accuracy in these supplements is crucial.

- Don't leave the certification section at the end of the form incomplete. The signature and date by the authorized person are mandatory for the return to be processed.

- Don't forget to review the section regarding payment and remittance instructions carefully. Ensure that the payment is made correctly and to the right place, whether electronically or by mail.

- Don't ignore the instructions on the form regarding updates to mailing addresses or other contact information. Keeping records up to date is vital for receiving timely communication from the Department of Finance.

Adhering to these guidelines can simplify the process of filing the NYC Commercial Rent Tax Return and help avoid common pitfalls that lead to processing delays or inaccuracies in tax obligations.

Misconceptions

Understanding the intricacies of the New York City Commercial Rent Tax (CRT) can be a complex process, filled with misconceptions that can lead to errors in compliance and reporting. Here is a breakdown of 10 common misconceptions about the NYC Commercial Rents Tax Return form:

- Only corporations need to file: It's a common mistake to think that only corporations are required to file a Commercial Rent Tax Return. In reality, partnerships, individuals, estates, and trusts engaging in commercial activities within certain areas of Manhattan are also subject to this tax and must file if they meet the criteria.

- Rent reporting is annual only: While the tax is for the fiscal year, businesses need to report their full year's rent on this return, or the annualized rent if the property was not rented for the full year, not just the amount paid annually.

- No tax if rent is under $250,000: There's a widespread belief that if your rent is under $250,000, you won't owe any tax. While it's true that the tax rate for rents under $250,000 is 0%, you are still required to file the return if your gross rent meets the minimum threshold for filing.

- Tax credits don't apply to small businesses: Actually, there are specific tax credits available for small businesses, including a Small Business Tax Credit that can significantly reduce the amount of tax due.

- Subtenant income is irrelevant: This is not true. Rent received from subtenants needs to be reported and can affect your tax computation, including possible deductions.

- Electronic filing is optional: While paper filing is still accepted, New York City encourages electronic filing for quicker processing and for environmental reasons. In some cases, electronic filing might be mandated in the future.

- All premises are taxed equally: The amount of tax due can vary significantly based on the type of premises, the location, and specific rent arrangements, such as deductions for subtenants or revitalization credits.

- Only direct rent payments are taxable: This is not the case. The commercial rent tax calculation considers not just direct rent payments but also other rent-related expenses, potentially including property tax escalations, depending on the specific lease agreements.

- Preparations for filing are straightforward: Preparing to file the CRT return can be quite complex, particularly for businesses with multiple premises, subtenants, or those eligible for various deductions and credits. Thorough preparation and understanding of the form are crucial.

- Amended returns are only for correcting mistakes: While it's true that amended returns are often filed to correct errors, they can also be used to claim a refund or report additional tax due if the initial filing was incorrect or incomplete in other ways.

It's essential for businesses operating in qualifying areas of Manhattan to gain a comprehensive understanding of the Commercial Rent Tax to ensure compliance and optimize their tax liability. Seeking guidance from a tax professional or the NYC Department of Finance is advisable for clarifications on complex situations.

Key takeaways

When dealing with the NYC Commercial Rents Tax Return form, it's important to have all your information ready and to follow these key guidelines to ensure a smooth process:

- Make certain you report your firm's Employer Identification Number accurately—this is crucial for identifying your business with the Department of Finance.

- Be ready to provide the preparer's contact details, including telephone number and Social Security Number or PTIN, to facilitate communication if needed.

- Identify the type of business entity you are filing for—whether it's a corporation, partnership, or individual entity. This affects how taxes are calculated and processed.

- Check if any special conditions apply, such as filing an amended return, and ensure you tick the appropriate box to indicate this on the form.

- Calculate your total tax due carefully by taking into account the base rent rate and applicable tax rate, and remember to apply any eligible tax credits and deductions.

- If your business qualifies for a Small Business Tax Credit, make sure to accurately calculate and claim this on your return to reduce the amount of tax payable.

- For firms with a change of address or Employer Identification Number, promptly update your information with the NYC Department of Finance to ensure accurate records and communication.

- Filing electronically via NYC.gov/eServices is encouraged for efficiency, but if you're filing on paper, double-check that you have completed all necessary sections and attached any required documentation or schedules.

Adhering to these key points will help ensure that your Commercial Rents Tax Return is completed accurately and submitted in compliance with NYC Department of Finance requirements.

Common PDF Documents

New York Bonus Depreciation - Adjustments made on this form ensure fair tax treatment of properties impacted by post-9/11 legislation.

Uft per Session Time Sheet - Integral for ensuring that per session employment remains within regulated boundaries.