Free Nyc 579 Gct Form in PDF

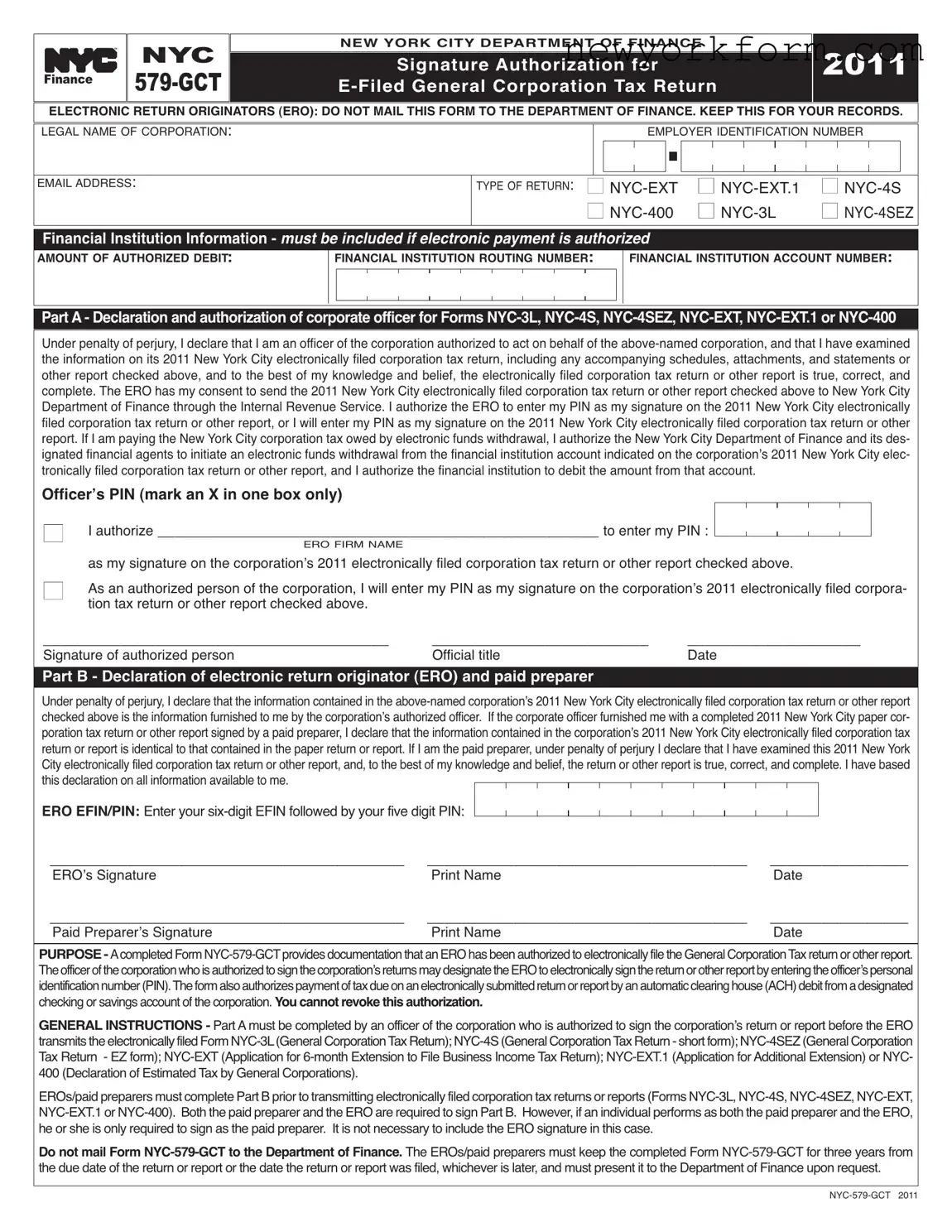

In navigating the complexities of tax compliance, corporations in New York City face the essential task of accurately submitting their General Corporation Tax (GCT) returns. The NYC 579-GCT form plays a critical role in this process, serving as the Signature Authorization for E-Filed General Corporation Tax Return. This form is a bridge between the corporation and the New York City Department of Finance, enabling the electronic filing of important tax documents without the need to mail physical forms. Specifically tailored for the 2011 tax year, it encompasses various types of returns such as NYC-EXT, NYC-EXT.1, NYC-4S, NYC-400, NYC-3L, and NYC-4SEZ. This form not only facilitates the declaration and authorization by a corporate officer to submit these forms electronically but also includes provisions for the electronic payment of taxes through automatic clearinghouse (ACH) debit, thereby requiring financial institution information to process such transactions. Notably, the form underscores the importance of accountability and accuracy by requiring declarations under penalty of perjury from both the corporate officer and the electronic return originator (ERO) or paid preparer, ensuring that the information filed is true, correct, and complete. It explicitly states that EROs should not mail this form to the Department of Finance but rather retain it for their records, emphasizing the form’s function as an internal document crucial for streamlining the tax filing process, enhancing operational efficiency, and ensuring compliance with tax obligations without the physical limitations of paper filing.

Nyc 579 Gct Sample

FINANCE

NYC

NEW YORK CITY DEPARTMENT OF FINANCE

Signature Authorization for

2011

2011

ELECTRONICRETURNORIGINATORS(ERO):DONOTMAILTHISFORMTOTHEDEPARTMENTOFFINANCE. KEEPTHISFORYOURRECORDS.

LEGAL NAME OF CORPORATION:

EMPLOYER IDENTIFICATION NUMBER

EMAILADDRESS:

TYPE OF RETURN: ■ |

■ |

■ |

■ |

■ |

■ |

Financial Institution Information - must be included if electronic payment is authorized

AMOUNT OF AUTHORIZED DEBIT:

FINANCIAL INSTITUTION ROUTING NUMBER:

FINANCIAL INSTITUTION ACCOUNT NUMBER:

Officerʼs PIN (mark an X in one box only)

■ |

I authorize ___________________________________________________ to enter my PIN : |

|

|

|

|

|

|

|

|

|

|

||

|

ERO FIRM NAME |

|||||

|

as my signature on the corporationʼs 2011 electronically filed corporation tax return or other report checked above. |

|||||

■As an authorized person of the corporation, I will enter my PIN as my signature on the corporationʼs 2011 electronically filed corpora- tion tax return or other report checked above.

________________________________________ |

_________________________ |

____________________ |

Signature of authorized person |

Official title |

Date |

Part B - Declaration of electronic return originator (ERO) and paid preparer

ERO EFIN/PIN:

_________________________________________ |

_____________________________________ |

________________ |

EROʼs Signature |

Print Name |

Date |

_________________________________________ |

_____________________________________ |

________________ |

Paid Preparerʼs Signature |

Print Name |

Date |

File Overview

| Fact | Description |

|---|---|

| Form Name and Year | NYC 579-GCT for the year 2011 |

| Purpose | Form NYC 579-GCT is used for the authorization of electronic filing and payment of the New York City General Corporation Tax. |

| Requirements | The form must be signed by an officer of the corporation who is authorized to represent the corporation and give consent for electronic filing and payment. |

| Storage Guidance | Electronic Return Originators (EROs) and paid preparers are instructed not to mail this form to the Department of Finance but to keep it in their records for three years after the return or report due date or the date it was filed, whichever is later. |

| Governing Law | The form is regulated under New York City's Department of Finance rules regarding the filing and payment of General Corporation Tax. |

Nyc 579 Gct: Usage Guidelines

Filling out the NYC 579-GCT form is a step required for corporations filing their General Corporation Tax return electronically. This form serves to authorize an Electronic Return Originator (ERO) to file the return on behalf of the corporation and to allow for the electronic payment of taxes due. Ensuring this form is completed accurately is essential to the tax filing process. Follow the step-by-step instructions below to accurately complete this form.

- Start with the section labeled "Legal Name of Corporation." Write the official name of your corporation as recognized by the state and any governing bodies.

- Enter the Employer Identification Number (EIN) of your corporation in the designated space.

- Provide the email address associated with the corporation or the officer completing the form.

- In the "Type of Return" section, mark the appropriate box to indicate the specific form your corporation is submitting. Options include NYC-3L, NYC-4S, NYC-400, NYC-4SEZ, NYC-EXT, or NYC-EXT.1.

- If your corporation is authorizing an electronic payment, fill in the "Amount of Authorized Debit" with the amount of tax due.

- Provide your financial institution's routing number and account number from which the authorized debit will be withdrawn.

- In Part A, asserting the declaration and authorization, the corporate officer must declare their role and acknowledgment of the return’s accuracy and completeness under penalty of perjury.

- Decide on the method of signing the authorization. If an ERO is authorized to enter the PIN, check the appropriate box and provide the ERO firm's name. Alternatively, if the officer is signing directly, check the second box and be ready to enter your PIN on the electronic return.

- Complete the signature section with the name of the authorized officer, their official title, and the date.

- In Part B, the ERO or paid preparer must declare the accuracy of the information provided to the best of their knowledge after reviewing the materials furnished by the corporation's authorized officer.

- The ERO or paid preparer then enters their EFIN/PIN as required.

- Both the ERO and the paid preparer must sign and date the bottom of the form, providing print names for clarification.

Upon completion of the NYC 579-GCT form, remember not to mail this document to the Department of Finance. Instead, it should be kept for records for three years after the due date of the return or the date the report was filed, whichever is later. Being ready to present it upon request is crucial. This precaution ensures compliance and verifies the authorization for electronic dealings with the New York City Department of Finance.

FAQ

- What is the NYC 579-GCT form?

- Who needs to complete the NYC 579-GCT form?

- What types of returns can be filed using the NYC 579-GCT form?

- NYC-3L (General Corporation Tax Return)

- NYC-4S (Short Form General Corporation Tax Return)

- NYC-4SEZ (General Corporation Tax Return - EZ form)

- NYC-EXT (Application for 6-month Extension to File Business Income Tax Return)

- NYC-EXT.1 (Application for Additional Extension)

- NYC-400 (Declaration of Estimated Tax by General Corporations)

- Is it mandatory to authorize electronic payment when filing electronically using the NYC 579-GCT form?

- How does a corporation authorize an ERO to file on their behalf?

- What is the retention period for the NYC 579-GCT form?

- Can the authorization to debit an account be revoked once given?

- What happens if both the ERO and a paid preparer are involved in the electronic filing process?

The NYC 579-GCT form is a document used by the New York City Department of Finance for General Corporation Tax (GCT) returns. It is specifically for electronic filing and serves as a signature authorization. The form allows Electronic Return Originators (EROs) to file a corporation tax return electronically on behalf of a corporation. It includes the legal name of the corporation, Employer Identification Number, email address, type of return, financial institution information for electronic payments, and declarations from both the corporate officer and the ERO or paid preparer.

Any corporation that is filing their General Corporation Tax return electronically with the New York City Department of Finance should complete this form. It must be filled out by an authorized officer of the corporation and the Electronic Return Originator (ERO) or paid preparer managing the electronic filing.

The form supports various types of GCT returns, including but not limited to:

While the form includes sections for financial institution information to authorize electronic payment, it is not mandatory to opt for electronic payment. However, it streamlines the process by allowing for the automatic debit of tax owed from the corporation's designated account, making it an efficient option for many corporations.

The authorized officer of the corporation can authorize an ERO to file on their behalf by completing Part A of the form. This section includes declaring, under the penalty of perjury, that the officer is authorized to act on behalf of the corporation and that the information on the tax return is true, correct, and complete. The officer must also authorize the ERO to use their Personal Identification Number (PIN) as their signature for the electronic filing.

EROs and paid preparers who handle the electronic filing must keep the completed NYC 579-GCT form for three years from the due date of the tax return or report, or the date it was filed, whichever is later. It’s important to note that the form is not to be mailed to the Department of Finance but must be presented upon request.

No, once you authorize the New York City Department of Finance and its designated financial agents to initiate an electronic funds withdrawal from the indicated account, this authorization cannot be revoked.

In cases where both an ERO and a paid preparer are involved, both individuals are required to sign Part B of the form. However, if a single individual performs as both the ERO and the paid preparer, then they only need to sign the form as the paid preparer; the ERO signature is not necessary in this instance.

Common mistakes

Filling out the NYC 579 GCT form, which is a critical document for electronic filing of General Corporation Tax returns in New York City, involves a detailed process that is pivotal for any corporation. Unfortunately, errors can occur, leading to complications or delays in processing. Couple this complexity with the busy life of a corporate officer, and you have a recipe for some common mistakes. Here’s a closer look at five frequent slips people make when handling this document.

- Incorrect or Incomplete Financial Institution Information: Since the form allows corporations to pay their tax due via electronic funds withdrawal, filling out accurate financial details is paramount. The most common error in this section includes providing incorrect financial institution routing or account numbers. An error here can result in failed payment transactions.

- Failure to Correctly Authorize the Electronic Return Originator (ERO): Part B of the form requires the declaration and authorization of the ERO and paid preparer. Often, signatories might skip this part or not provide clear authorization, leading to validation issues in the electronic filing process.

- Not Reviewing the Form for Accuracy and Completeness: Before submission, it's vital to ensure that all information on the form is true, correct, and complete under penalty of perjury. A rushed review can lead to errors in tax return information, which, in the worst case, could be construed as filing false statements.

- Omitting the PIN for Electronic Signature: One crucial aspect of the NYC 579 GCT is the use of PIN as a signature for the corporation's electronically filed tax return. It is not uncommon for individuals to overlook the entry of the PIN in the designated section, leading to processing delays.

- Keeping Inaccurate Records: EROs and paid preparers must keep the completed forms for three years. However, poor record-keeping practices can make it challenging to retrieve these documents when requested by the Department of Finance, leading to compliance issues.

To avoid these mistakes, thorough review and understanding of each section before filling out the form can save time and prevent potential headaches with tax filings. Ensuring that all involved parties, including the authorized officer and the ERO, are well-informed and diligent in their roles is equally crucial. After all, accurate and prompt filing benefits not just the corporation, but also contributes to a smoother operation within the city’s financial framework.

Indeed, the NYC 579 GCT form is more than just paperwork; it’s a responsibility. Getting it right the first time not only demonstrates compliance but also reflects on the corporation's commitment to maintaining upstanding financial operations within New York City.

Documents used along the form

When preparing taxes for a corporation in New York City, it is essential to use the correct forms to ensure accurate filing and compliance with tax laws. The NYC 579-GCT form, a key document for e-filing the General Corporation Tax return, is often used alongside several other forms. These documents serve to streamline the tax filing process, ensure proper reporting of income, and facilitate payments and extensions. Highlighting each form's purpose provides clarity on their roles in corporate tax preparation.

- NYC-3L: General Corporation Tax Return: This form is designed for corporations to report their income, calculate their tax liability, and summarize their financial activities over the fiscal year.

- NYC-4S: General Corporation Tax Return (Short Form): A simplified version of the NYC-3L, intended for smaller corporations that meet certain criteria, making the tax filing process more straightforward.

- NYC-4SEZ: General Corporation Tax Return - EZ Form: For qualifying corporations, this form offers an even more streamlined filing option, simplifying compliance and reporting requirements.

- NYC-EXT: Application for 6-month Extension to File Business Income Tax Return: Corporations that need more time to complete their tax returns can file this form to request an extension.

- NYC-EXT.1: Application for Additional Extension: In circumstances where more time beyond the initial 6-month extension is necessary, this form can be submitted to request additional time.

- NYC-400: Declaration of Estimated Tax by General Corporations: Corporations are required to estimate and pay their taxes quarterly. This form facilitates the declaration and payment of estimated taxes.

- NYC- UBT: Unincorporated Business Tax Return: Although primarily for unincorporated businesses, corporations involved in certain partnership activities might also need to file this form.

- NYC-202: Bi-annual Statement of Estimated Tax: Similar to the NYC-400, this form is used for bi-annual updates and estimates of tax liability, ensuring payments are aligned with actual income.

Understanding each of these documents and their specific requirements is instrumental in navigating the complexity of corporate taxation in New York City. Working in concert, they ensure a corporation fulfills its tax obligations efficiently and accurately. Keeping these forms and their purposes in mind can significantly ease the process of tax preparation and filing for corporations and their preparers.

Similar forms

The NYC 579 GCT form is closely related to the IRS Form 8879, IRS e-file Signature Authorization. This similarity is because both forms serve the purpose of authorizing electronic signatures for tax filings. The NYC 579 GCT is specific to New York City's General Corporation Tax returns, while Form 8879 applies to federal tax returns. Each document is critical for validating the electronic submission of tax returns, ensuring that the electronically filed documents are as legally binding as paper documents signed in ink.

Another document comparable to the NYC 579 GCT form is the Form NYC-3L, General Corporation Tax Return. While NYC 579 GCT authorizes signatures and electronic payments for such tax submissions, NYC-3L is the actual tax return form for corporations that are subject to the General Corporation Tax in New York City. Both forms work in conjunction, as the NYC 579 GCT form supports the electronic filing and payment authorization for the tax reported on Form NYC-3L.

Form NYC-4S, the General Corporation Tax Return - short form, also shares a connection with the NYC 579 GCT form. Specifically designed for smaller corporations eligible to file a more succinct version of the tax return, the NYC-4S requires proper authorization for electronic filing and payment, facilitated by the NYC 579 GCT. This illustrates how different types of tax return forms, based on the size and nature of the corporation, still necessitate a consistent process for electronic authorization.

Similarly related is the Form NYC-EXT, Application for 6-month Extension to File Business Income Tax Return. This document is used when corporations need more time to prepare their comprehensive tax return. The NYC 579 GCT form's role in authorizing electronic submission and payment directly impacts how extensions like the NYC-EXT are filed and processed, ensuring that even extended filings are handled efficiently in an electronic environment.

Form NYC-EXT.1, an Application for Additional Extension, works in tandem with the NYC 579 GCT form for corporations that find themselves needing further extension beyond the initial 6-month period allowed by Form NYC-EXT. The authorization for electronic filing and payment provided by the NYC 579 GCT ensures that these additional requests for extensions can be submitted efficiently and securely in an electronic format.

The Form NYC-400, Declaration of Estimated Tax by General Corporations, is another document related to the NYC 579 GCT. Estimated taxes, which are payments made in advance of the annual tax return filing, require precise documentation and authorization for electronic processing, facilitated by the NYC 579 GCT form. This demonstrates the form's broader applicability in various tax payment scenarios beyond the final tax return filing.

Form NYC-4SEZ, General Corporation Tax Return - EZ Form, shares similarities with the NYC 579 GCT in that it is another version of the tax return tailored for corporations that meet certain criteria allowing for a simplified filing process. Like with other return forms, the seamless and secure electronic filing and payment of the taxes declared in the NYC-4SEZ are authorized by the NYC 579 GCT form.

The Electronic Filing Identification Number (EFIN) application process, while not a form identical to the NYC 579 GCT, is a prerequisite for tax preparers that intend to submit tax returns electronically. The need for an EFIN underscores the importance of authorized electronic processes embodied by the NYC 579 GCT, ensuring that those filing electronically are qualified and the submissions are secure.

Lastly, the Electronic Federal Tax Payment System (EFTPS) Enrollment Form, although more broadly applicable and federal in scope, shares conceptual similarities with the NYC 579 GCT form. Both facilitate electronic payments tied to tax obligations, with the EFTPS being used for a variety of tax types across the United States and the NYC 579 GCT specifically authorizing payments for New York City's corporation taxes. This highlights the widespread move towards electronic processes in tax administration.

Dos and Don'ts

When preparing to fill out the NYC 579 GCT form for General Corporation Tax Return through electronic filing, it's vital to pay close attention to detail and follow the specific instructions provided. To ensure accuracy and compliance, here's a compiled list of actions to take and avoid.

Do:

- Ensure that the legal name of the corporation and the employer identification number is correctly entered, as these are crucial for identification.

- Verify the financial institution information, including the routing and account number, if you authorize an electronic payment, to avoid any issues with payment processing.

- Check the appropriate type of return box(es) to indicate which form(s) you are filing electronically with the city.

- Complete Part A of the form with great care, making sure that an authorized corporate officer signs and dates it, as it includes a declaration under penalty of perjury regarding the truth and completeness of the return.

- Obtain the officer's PIN for electronic signing purposes, ensuring authorization is accurately recorded whether carried out by the Electronic Return Originator (ERO) or the officer directly.

- Have both the paid preparer (if applicable) and the ERO sign Part B of the form to acknowledge their examination and validation of the return's correctness and completeness.

- Keep the completed NYC 579 GCT form for your records for at least three years from the due date of the return or the date it was filed, whichever is later.

- Be ready to present the completed form to the Department of Finance upon request, even though it should not be mailed to them.

- Carefully read through the entire form before starting to fill it out to ensure all requirements are understood.

- Review the form thoroughly before finalizing to catch and correct any possible errors or omissions.

Don't:

- Do not mail this form to the Department of Finance as it is intended for your records and may be requested for verification.

- Avoid rushing through the filling of the form to minimize the risk of mistakes that could delay processing.

- Do not overlook the authorization sections for electronic payments and signing, as these are critical for a valid submission.

- Refrain from leaving any required fields blank; ensure all applicable sections are completed.

- Avoid guessing or estimating information; ensure all provided data is accurate and verifiable.

- Do not use unauthorized personnel to fill or sign the form; only authorized officers and EROs/preparers should complete it.

- Avoid discarding the form after submission; it needs to be retained for the specified period.

- Do not share your officer’s PIN or any sensitive financial information with unauthorized individuals.

- Avoid mixing information from different tax years or forms, which could lead to improper processing of your electronic filing.

- Do not ignore the general instructions provided with the form, as adherence is essential for compliance and successful filing.

Misconceptions

There are several misconceptions about the New York City 579 GCT form that need to be clarified for better understanding and compliance. Here are four of the most common misunderstandings:

- Misconception 1: The NYC 579 GCT form must be mailed to the Department of Finance. In reality, electronic return originators (EROs) are instructed not to mail this form to the Department of Finance. Instead, they are required to keep it in their records for a specified period.

- Misconception 2: Any corporate employee can complete and sign the NYC 579 GCT form. This form must be completed and signed by an officer of the corporation who is authorized to act on behalf of the corporation. This ensures that the information submitted is accurate and authorized at the corporate level.

- Misconception 3: Signing the NYC 579 GCT form authorizes the ERO to perform any actions on behalf of the corporation. The authorization given to the ERO is specifically to send the corporation’s electronically filed tax return or other report to the New York City Department of Finance through the IRS and, if applicable, to authorize electronic funds withdrawal for tax payment. It does not extend to other actions not related to the submission of electronic tax returns or payments.

- Misconception 4: Once submitted, the authorization on the NYC 579 GCT form cannot be revoked. The form clearly states that the authorization to electronically sign the return or other report and to initiate an electronic funds withdrawal cannot be revoked. This emphasizes the importance of being certain about the details and implications before the form is signed.

Understanding these aspects of the NYC 579 GCT form is crucial for corporations operating in New York City, as it ensures compliance with tax submission processes and helps avoid potential issues with the Department of Finance.

Key takeaways

Filling out and using the NYC 579-GCT form, essential for General Corporation Tax (GCT) returns in New York City, requires precise attention to detail and an understanding of its purpose and requirements. Here are some key takeaways to ensure the process is handled correctly.

- The NYC 579-GCT form is specifically designed for Electronic Return Originators (EROs) who file general corporation tax returns electronically on behalf of corporations. It's crucial not to mail this form to the Department of Finance but to keep it for records instead.

- When filling out the form, an officer of the corporation who is authorized to act on behalf of the corporation must complete Part A. This part includes a declaration and authorization for forms such as NYC-3L, NYC-4S, NYC-4SEZ, NYC-EXT, NYC-EXT.1, or NYC-400, verifying under penalty of perjury that the information provided is accurate and complete.

- The form requires the specification of a personal identification number (PIN) as a means of authorization for the ERO to electronically sign the tax return or other report. This highlights the importance of security and the need for careful handling of authorization credentials.

- Payment of taxes owed can be facilitated through electronic funds withdrawal authorized within the form. This section mandates the inclusion of financial institution information, such as routing and account numbers, emphasizing the need for accuracy to ensure the correct processing of tax payments.

- Part B of the NYC 579-GCT form is meant for the ERO and, if applicable, the paid preparer to complete. It serves as a declaration that all the information contained in the filed corporation tax return or report is true and furnished by the corporation's authorized officer. This part reinforces the accountability of both the corporation filing the report and the preparer handling the electronic submission.

Remember: Keeping the completed NYC 579-GCT form for at least three years from the due date of the return or the date the return was filed, whichever is later, is essential. The form must be presented to the Department of Finance upon request, highlighting the importance of proper record-keeping and compliance with local tax laws.

Common PDF Documents

How Does Medicaid Work in Ny - Applicants are encouraged to seek assistance from health care professionals or social workers when filling out this form.

Gen 215b - Clarifies the necessary qualifications for testers and installers of backflow prevention devices in New York City.