Free Nyc 400 Form in PDF

Understanding the intricacies of New York City's tax code is essential for corporations looking to comply with local tax obligations, and the Form NYC-400 emerges as a critical document in this landscape. Designed for general corporations to declare their estimated taxes for either the calendar year 2014 or a fiscal year beginning and ending on specified dates, this form underlines the necessity for entities whose tax estimates exceed $1,000 to make a declaration. The necessity to file this form isn’t limited to longstanding entities but also applies to new businesses in the city that foresee their tax liabilities surpassing the minimum threshold. It details a process for corporations to follow, including the initial declaration and successive installment payments based on tax liabilities from the previous year. Moreover, the form accommodates amendments for any corrections to tax estimates or payments, emphasizing the city's flexible approach to ensuring accurate tax collection. Notably, the form also highlights the implications of late filings, underscoring the financial repercussions that corporations may face if they fail to comply with the designated time frames. Filing the NYC-400 form is made simpler with the option for electronic filing, encouraging a more streamlined, secure, and efficient process for both first-time filers and seasoned businesses. This move towards digital solutions reflects New York City’s commitment to leveraging technology for better governance and taxpayer convenience.

Nyc 400 Sample

*30311491*

NEWYORK CITYDEPARTMENT OF FINANCE

TM |

ESTIMATEDTAXBYGENERALCORPORATIONS |

2014 |

||||||||||||||||||||||

FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For CALENDAR YEAR 2014 or FISCAL YEAR beginning _______________, _______ and ending _______________, ________ |

||||||||||||||||||||||||

Print or Type: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Name(If combined filer, give name of reporting corporation) See Instructions |

Taxpayer’s EmailAddress |

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In Care of |

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BUSINESS CODE NUMBER AS PER FEDERAL RETURN |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business telephone number |

|

Person to contact |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

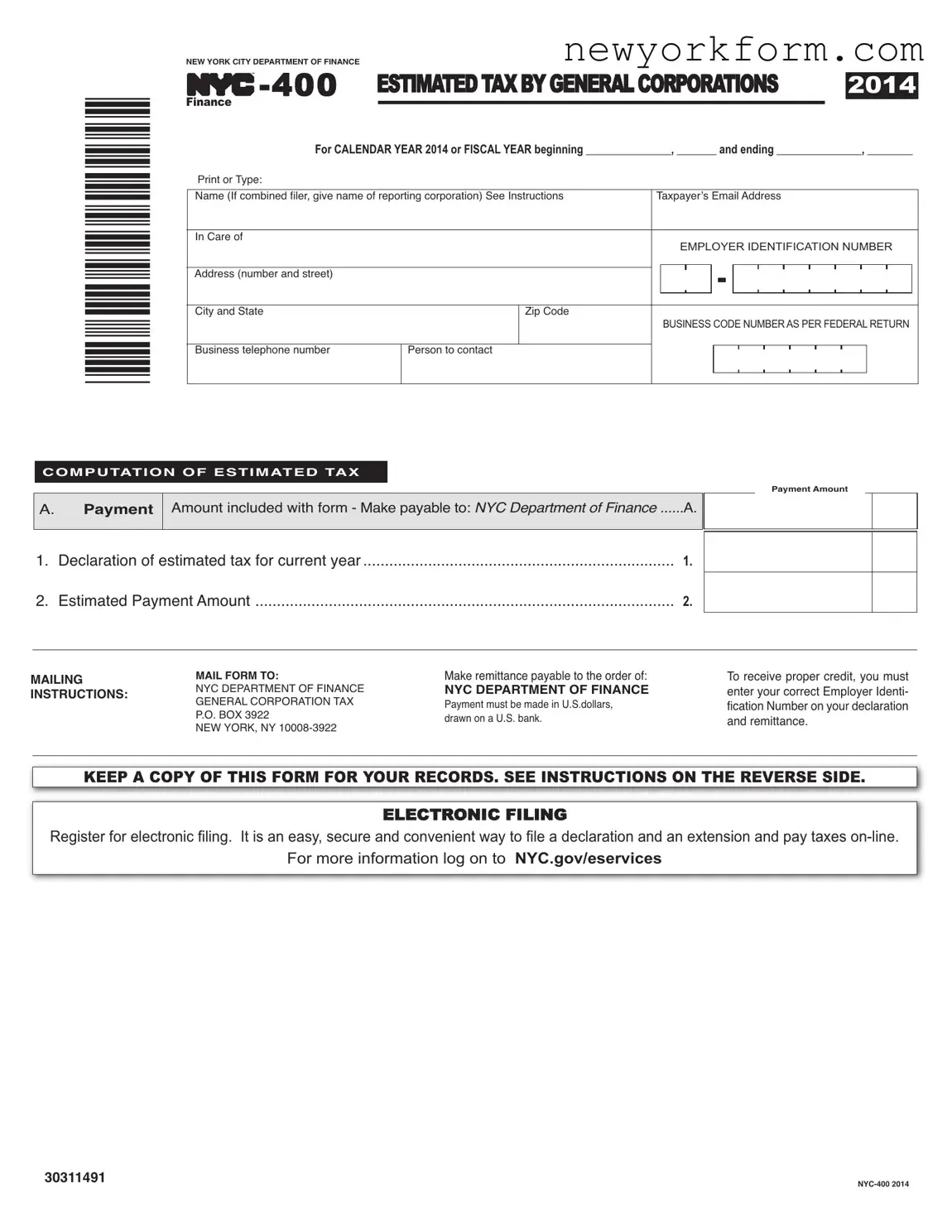

COMPUTATION OF ESTIMATED TAX

Payment Amount

A.Payment

Amount included with form - Make payable to: NYC Department of Finance |

......A. |

|

|

|

|

|

|

|

|

|

|

1. |

Declaration of estimated tax for current year |

1. |

2. |

Estimated PaymentAmount |

2. |

MAILING INSTRUCTIONS:

MAILFORM TO:

NYC DEPARTMENT OF FINANCE GENERAL CORPORATION TAX P.O. BOX 3922

NEW YORK, NY

Make remittance payable to the order of:

NYC DEPARTMENT OF FINANCE

Payment must be made in U.S.dollars, drawn on a U.S. bank.

To receive proper credit, you must enter your correct Employer Identi- ficationNumberonyourdeclaration and remittance.

KEEP A COPY OF THIS FORM FOR YOUR RECORDS. SEE INSTRUCTIONS ON THE REVERSE SIDE.

ELECTRONIC FILING

Registerforelectronicfiling.

For more information log on to NYC.GOV/ESERVICES

30311491

Form |

Page 2 |

|

|

WHOMUSTFILE

Every corporation subject to the NewYork City General CorporationTax (Title 11, Chapter 6, Subchapter 2 of theAdministrative Code) must file a declaration

NOTE:Ifthecurrentyear’staxisreasonablyestimatedtoexceed$1,000,anestimatedpaymentisrequiredevenifthisisthefirstyearofbusi- nessinNewYorkCityforthetaxpayerorthetaxpayerpaidonlytheminimumtaxfortheprecedingyear.Failuretopayorunderpayment ofestimatedtaxinthesecircumstanceswillresultinpenalties.

LINE1 - DECLARATIONOFESTIMATEDTAXFORCURRENTYEAR

Corporationswhosetaxliabilityfortheprecedingyearexceeds$1,000arerequiredtopay,withthetaxreportfortheprecedingyearorwith theapplicationforextensionoftimeforthefilingofsuchreport,25%ofthetaxliabilityfortheprecedingyearasafirstinstallmentofes- timatedtaxforthecurrentyear. Aftertakingcreditforthat25%paymentandfortheamountofanyoverpaymentshownonlastyear’sre- turnwhichthetaxpayerelectedtohaveappliedasacreditagainstthecurrentyear’stax,taxpayersfilingestimatedtaxarerequiredtopay the balance of estimated tax in fractional installments.

ESTIMATEDTAXDUEDATES

Iftherequirementsforfilingestimatedpayments |

Filetheformonorbeforethe: |

Thebalanceofestimatedtaxisdueasfollows: |

arefirstmetduringthetaxableyear: |

|

|

|

|

|

Before the first day of the 6th month |

15th day of the 6th month |

l 1/3 by the 15th day of the 6th month |

|

|

l 1/3 by the 15th day of the 9th month |

|

|

l 1/3 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 6th month and before the |

15th day of the 9th month |

l 1/2 by the 15th day of the 9th month |

first day of the 9th month |

|

l 1/2 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 9th month and before the |

15th day of the 12th month. In lieu of this form, |

Pay in full |

first day of the 12th month |

a completed tax report, with payment of any unpaid |

|

|

balance of tax, may be filed on or before the 15th day |

|

|

of the 2nd month of the following year. |

|

|

|

|

If any of the above dates fall on a Saturday, Sunday or legal holiday, the due date is the next business day.

AMENDMENTS

LATEFILING

PENALTY

The law imposes penalties for failure to pay or underpayment of estimated tax. (Refer to Section

istrative Code.)

ELECTRONICFILING

Note: Register for electronic filing. It is an easy, secure and convenient way to file and pay an extension

For more information log on to NYC.gov/eservices

File Overview

| Fact | Detail |

|---|---|

| Form Purpose | Estimated Tax by General Corporations for NYC |

| Year | 2014 |

| Governing Law(s) | New York City General Corporation Tax (Title 11, Chapter 6, Subchapter 2 of the Administrative Code) |

| Eligibility for Filing | Corporations with estimated tax over $1,000 |

| Payment Method | U.S. dollars, drawn on a U.S. bank to the NYC Department of Finance |

| Mailing Address | NYC Department of Finance General Corporation Tax P.O. Box 3922 New York, NY 10008-3922 |

| Electronic Filing | Available and encouraged for convenience and security |

| Penalties | For late filing or underpayment of estimated tax |

Nyc 400: Usage Guidelines

After completing the NYC-400 form, it's crucial to understand what comes next in the filing process. This form is designed for general corporations to declare and pay their estimated tax for the new fiscal year. Given its importance, filling it out correctly ensures compliance with the New York City Department of Finance's requirements. Once the form is correctly filled out and submitted by the due date, along with any payment due, businesses may focus on their planning and operations for the upcoming fiscal year, knowing their preliminary tax responsibilities have been addressed.

- Start by entering the calendar year or fiscal year for which the estimated taxes are being declared at the top of the form.

- In the "Print or Type" section, enter the name of the corporation. If filing as a combined group, provide the name of the reporting corporation.

- Input the taxpayer’s email address in the designated space to ensure communication accessibility.

- For corporations filing on behalf of the group, the "In Care of" space should be filled out with the appropriate contact information.

- Provide the Employer Identification Number (EIN) to identify the business correctly.

- Enter the complete address of the business, including number, street, city, state, and zip code, ensuring the Department of Finance can correspond as necessary.

- Fill in the Business Code Number as per the business's federal return. This code helps categorize the type of business operations.

- Provide a business telephone number and the name of a person to contact for any queries regarding the form.

- In the "COMPUTATION OF ESTIMATED TAX" section, calculate and enter the estimated tax payment amount in the space provided (A).

- Ensure the Payment Amount entered matches the check or electronic payment amount sent to the NYC Department of Finance.

- Review the mailing instructions carefully and mail the completed form to the NYC Department of Finance at the address given. Make sure the remittance is payable to the NYC Department of Finance, drawn on a U.S. bank, and in U.S. dollars.

- For convenience and to save time, consider registering for electronic filing as indicated on the form. This method facilitates easy, secure, and convenient declaration, extension filing, and tax payments online.

- Keep a copy of the completed form for your records, ensuring you have proof of compliance and can refer back to the information if needed.

Once the form and any required payment are submitted, it's critical to track due dates for any remaining estimated tax payments, as outlined in the provisions for the current fiscal year. Timely compliance with these deadlines helps avoid penalties and ensures smooth financial operations throughout the year.

FAQ

-

Who is required to file the NYC-400 form?

Every corporation operating under the New York City General Corporation Tax must file an NYC-400 form if its estimated tax for the current year is over $1,000. This requirement applies regardless of whether it's the corporation's first year of business in New York City or if the corporation only paid the minimum tax in the previous year. For combined returns, the member responsible for filing the return and paying the tax should submit this form.

-

What are the due dates for estimated tax payments?

Estimated tax payments are due in fractional installments throughout the fiscal year. The specifics depend on when in the tax year the filing requirements are met. For filings required before the 6th month, payments are due on the 15th day of the 6th, 9th, and 12th months. If the requirement is first met between the 6th and 9th months, half the payment is due by the 15th day of the 9th month, with the remainder by the 15th day of the 12th month. For requirements met after the 9th month, the full payment is due by the first day of the 12th month. Should these dates fall on a weekend or legal holiday, the due date moves to the next business day.

-

What happens if amendments are needed after the 9th month?

If there's a need to amend the estimated tax or related payments after the 15th day of the 9th month, an amended form must be filed using the NYC-400 or the Notice of Estimated Tax Payment. Along with the amendment, any increase in the estimated tax must be paid. This ensures that corporations can adjust their contributions accurately and in a timely manner to reflect their tax obligations better.

-

Are there penalties for late filing or underpayment?

Yes, penalties are imposed for both late filing of the NYC-400 form and underpayment of estimated taxes. These penalties are detailed in Section 11-676, Subdivisions 3 and 4 of the Administrative Code. Businesses are encouraged to file and make estimated tax payments promptly to avoid these penalties. It's worth noting the option for electronic filing, which offers an easy, secure, and convenient way to file an extension online and could help avoid late submissions.

Common mistakes

Filling out the NYC-400 form, a requirement for corporations in New York City estimating taxes over $1,000, is critical for compliance and avoiding penalties. Common mistakes can lead to unnecessary complications. Here are eight errors often made:

- Incorrect Employer Identification Number (EIN): The EIN must match the corporation's official records. An incorrect EIN may cause delays or misapplication of your payment.

- Not Using the Correct Business Address: The address provided should be current and match the official address on file with the IRS. Changes in address that are not updated can result in missed communications.

- Omitting the Business Code Number: The form requires your federal return business code number. This number helps categorize your business type and is crucial for accurate processing.

- Failure to Declare the Correct Estimated Tax: On Line 1, corporations are to declare their estimated tax for the current year, taking into account credits and previous payments. Misestimating can lead to underpayment penalties.

- Incorrect Payment Amount Included: Payment amount errors are common. Ensure the amount matches the expected tax liability, and double-check all calculations.

- Not Following the Specified Payment Schedule: Depending on when you first meet the filing requirements during the tax year, payment schedules vary. Failure to adhere to the specific due dates results in penalties.

- Misunderstanding Electronic Filing Options: While electronic filing is encouraged for its convenience, some filers overlook this option due to misunderstanding its availability or benefits, potentially slowing down the process.

- Not Keeping a Copy of the Form: For record-keeping and future reference, it's important to retain a copy of the filled-out NYC-400 form, which many forget to do.

Mistakes on the NYC-400 form can lead to delayed processing, incorrect estimations of tax due, and penalties. It's important for corporations to review their form thoroughly before submission, ensure all information is accurate and current, and adhere to the specified timelines. For corporations filing combined returns, the group member responsible for filing and paying must pay special attention to these details to prevent issues for the group.

Understanding the nuances of the NYC-400 form and avoiding these common errors can help ensure compliance with New York City's tax obligations, contributing to a smoother financial operation for your corporation.

Documents used along the form

When it comes to managing your business's obligations to the New York City Department of Finance, learning which forms and documents are often used in tandem with the NYC-400 form can streamline the process and ensure compliance. The NYC-400 form is a crucial document for estimating tax by general corporations, but it doesn't stand alone. Various other forms complement the NYC-400, each serving a specific purpose in the broader context of corporate tax responsibilities.

- Form NYC-300 - This form is used for the Declaration of Estimated Tax by S Corporations. It's similar to the NYC-400 but specifically tailored for S Corp tax considerations, taking into account the different tax treatment of S Corporations.

- Form NYC-1 - Annual Return for Business Corporation Tax. This comprehensive return is filed annually by corporations, detailing their income, deductions, and tax owed to NYC.

- Form NYC-EXT - Application for Automatic Extension of Time to File Business Income Tax Returns. Corporations needing more time to file their comprehensive tax returns can use this form to request an extension.

- Form IT-2658 - Report of Estimated Personal Income Tax for Nonresident Individuals; applicable when nonresident shareholders owe tax on earnings from the corporation.

- - Businesses must issue this query,"form to contractors or cursrent, ,"formers who they've been treating as subjectctly were canadian equivalents receiving paymentsmos totwrights $ "temporary residing overseas totalto work from requests starting a page back of earnings.

- Form NYC-114.10 - Certificate of Payment of Estimated Tax. This document serves as proof that the corporation has made payments towards its estimated tax liability.

- Form NYC-9.5 - Claim for Reassessment Exclusion for General Corporation Tax. Corporations can file this form to exclude certain reassessed values from their taxable income.

- Form W-9 - Request for Taxpayer Identification Number and Certification. It's often used when setting up vendor accounts or for other situations where the business's tax ID needs to be formally communicated.

- Form CT-400 - Estimated Tax for Corporations. For corporations that also owe taxes at the state level, this New York State form helps estimate those tax obligations.

Understanding these additional forms and documents can make managing your corporation's tax affairs much smoother. While the NYC-400 plays a pivotal role in the estimated tax process, these supplemental forms ensure that all tax bases are covered, from annual returns to specific exemptions and extensions. By familiarizing yourself with these documents, you can help ensure that your corporation remains in good standing with both the city and state tax departments.

Similar forms

The NYC-400 form, tailored for estimating tax payments by general corporations in New York City, shares similarities with the IRS Form 1120-W, which is the Estimated Tax for Corporations form used at the federal level. Both forms are designed for corporations to calculate and remit their estimated taxes for the year, ensuring compliance with tax laws and avoiding penalties for underpayment or late payment. While the NYC-400 is specific to the tax obligations within New York City, the 1120-W form encompasses estimated tax payments at the federal level, reflecting the broader scope of tax liability for corporations operating across the United States.

Similar to the NYC-400 form, the IRS Form 1040-ES is used for estimating taxes, but it is aimed at individuals, sole proprietors, partners, and S corporation shareholders. It serves a similar purpose in helping taxpayers calculate and pay estimated taxes quarterly to avoid penalties. The 1040-ES form ensures that these taxpayers, much like corporations filling out the NYC-400, comply with the pay-as-you-go tax system of the United States, although the target audience and specific tax details may differ between the two forms.

The UBT-ES form, or Unincorporated Business Tax Estimated Tax Payments form, is another document with parallels to the NYC-400. This form is used by unincorporated businesses operating within New York City to estimate and make payments for their business taxes throughout the year. Both the UBT-ES and NYC-400 forms cater to different types of business structures but share the goal of facilitating estimated tax payments within the specified jurisdiction, highlighting the city's approach to capturing tax revenues from a diverse range of business operations.

The NYC-300 form, which is used for the General Corporation Tax Return in New York City, operates within the same tax ecosystem as the NYC-400. While the NYC-400 deals with estimated payments, the NYC-300 is geared towards the annual reporting and finalization of a corporation's tax obligations. These documents are interconnected, with the estimated payments made via the NYC-400 potentially impacting the final tax liability reported on the NYC-300, underscoring the cyclical nature of tax preparation and filing for corporations in the city.

Another document sharing similarities with the NYC-400 is the IRS Form 990-W, which is an Estimated Tax on Unrelated Business Taxable Income for Tax-Exempt Organizations. Although primarily for tax-exempt entities engaging in revenue-generating activities unrelated to their exempt purposes, the form's essence in calculating and paying estimated taxes aligns with the NYC-400's objective. Both forms ensure organizations, whether for-profit or tax-exempt, meet their tax obligations proactively throughout the fiscal year.

The IRS Form 941, Employer's Quarterly Federal Tax Return, parallels the NYC-400 in its periodic approach to tax payments, specifically for payroll taxes. While the NYC-400 is concerned with a corporation's overall estimated tax liability, the 941 form focuses on the reporting and paying of payroll taxes on a quarterly basis. This similarity underscores the importance of regular tax payments to different taxing authorities, ensuring entities fulfill their ongoing tax responsibilities throughout the year.

Lastly, the Payment Voucher (often accompanying specific tax forms such as Form 1120 or state-specific tax returns) shares a straightforward functional resemblance with the NYC-400. These vouchers are used by taxpayers to accompany checks or money orders when making tax payments, facilitating the correct application of payments to taxpayer accounts. Both the NYC-400 and payment vouchers are instrumental in ensuring payments are accurately and effectively processed by the respective tax departments, highlighting their role in efficient tax administration.

Dos and Don'ts

When approaching the task of filling out the Form NYC-400, which pertains to the estimated tax for general corporations, individuals are encouraged to proceed with meticulous care to ensure compliance and accuracy. The following guidelines aim to assist in this process, delineating both recommended practices and pitfalls to avoid.

Do:

- Ensure that all the information is current and accurate. Double-check the Employer Identification Number (EIN), business address, and the taxpayer’s email address to make sure they are up to date. This information is crucial for the New York City Department of Finance to process your form properly.

- Calculate your estimated tax payments correctly. It is imperative that the amount of tax estimated to be imposed by section 11-603 of the Administrative Code, minus the sum of the credits estimated to be allowable against the tax, is calculated with precision to avoid underpayment penalties.

- Adhere to filing and payment deadlines. To avoid late filing fees and other penalties, make sure to file the form and make any necessary payments according to the due dates specified in the instructions section of the form.

- Keep a copy of the form for your records. After filing, retain a copy of the NYC-400 form. This practice is helpful for future reference and is beneficial in the case of any inquiries from the Department of Finance.

Don't:

- Delay registration for electronic filing. The Department of Finance encourages filing and paying online due to its convenience, security, and speed. Late registration can complicate or delay the filing process.

- Make payments in foreign currency or through non-U.S. banks. All payments must be made in U.S. dollars and drawn on a U.S. bank. Failure to comply with this requirement can result in payment rejection.

- Ignore the importance of amending your form if necessary. If, after filing, you discover that your tax estimate needs correction, file an amended form promptly to adjust the tax estimates and related payments.

- Forget to apply for extensions if unable to meet the original due dates. If it becomes apparent that you will not be able to file on time, apply for an extension to avoid penalties related to late filing and payment.

Misconceptions

Understanding the Form NYC-400, or the Estimated Tax by General Corporations, involves navigating through a myriad of details specific to businesses operating within New York City. However, misconceptions about this form can lead to mistakes or oversights that have significant consequences for a corporation. Let's clear up some of the most common misunderstandings:

- Misconception #1: Only corporations paying above a certain threshold need to file. One common mistake is thinking that if your corporation's tax liability is minor, you're exempt from filing the NYC-400 form. The truth is, any corporation subject to the New York City General Corporation Tax and expects its estimated tax for the year to exceed $1,000 must file. This requirement applies regardless of the corporation's size or income, aiming to ensure every corporation contributes its fair share to the city's finances.

- Misconception #2: Electronic filing is optional. In today's digital age, the move towards electronic filings is not just for convenience but also a requirement in many jurisdictions, including New York City. The NYC-400 form notes that registering for electronic filing is encouraged; however, many perceive it as merely a suggestion. It's crucial for corporations to understand that electronic filing is highly recommended, offering a secure, fast, and more efficient process for managing tax obligations.

- Misconception #3: The form applies only to the calendar year. The flexibility of the NYC-400 allows corporations to file based on either the calendar year or a fiscal year. This misinterpretation often leads to incorrectly filed forms and miscalculated taxes. Understanding that the form accommodates different fiscal schedules can help corporations plan their tax payments more accurately and avoid penalties for late or incorrect filings.

- Misconception #4: Estimated tax payments are calculated once and remain static. Many corporations mistakenly believe that once they calculate their estimated taxes for the year, these figures are set in stone. However, the NYC-400 form anticipates changes in a corporation's financial condition or tax laws by allowing for amendments to the estimated tax. This flexibility is crucial for corporations to maintain compliance and adjust their tax obligations in response to changes throughout the tax year.

- Misconception #5: Late filing automatically results in penalties. While it's true that failing to file or pay the estimated tax on time can lead to penalties, the NYC-400 form provides a grace period for corporations that miss the deadline due to reasonable causes. Understanding that penalties are not immediately imposed for late filings can alleviate some stress; however, it's still in a corporation's best interest to file on time to avoid potential fines and complications.

By addressing these misconceptions, corporations can better navigate their tax responsibilities, ensuring compliance with New York City's financial regulations. Understanding the specifics of the NYC-400 form is vital for any corporation to manage its tax obligations accurately and efficiently.

Key takeaways

Filling out and utilizing the NYC-400 form, intended for the estimated tax by general corporations, requires careful attention to several critical points to ensure compliance and accuracy. Here are nine key takeaways from the document:

- The NYC-400 form is essential for any corporation subject to New York City's General Corporation Tax if its estimated tax for the current year exceeds $1,000.

- Corporations must provide detailed information, including the Employer Identification Number (EIN), business code as per the federal return, and contact information, ensuring the Department of Finance can reach them if needed.

- Payment of the estimated tax is made to the NYC Department of Finance, and it's crucial to use U.S. dollars drawn from a U.S. bank. Accurate details, especially the EIN, are vital for proper payment processing and crediting.

- Electronic filing is encouraged as it offers a secure, convenient, and efficient method of submitting the declaration and payment. This can be done through the NYC.gov/eservices portal.

- Declaration of Estimated Tax for the Current Year: This segment obligates those with a tax liability exceeding $1,000 from the preceding year to pay a portion of their estimated tax upfront.

- Amendments to the tax estimate can be made using the NYC-400 form or Notice of Estimated Tax Payment due for changes in the tax estimate or payment corrections.

- Estimated Tax Due Dates outline when payments should be made during the fiscal year, segmenting payments into fractional installments based on when the filing requirements are met during the taxable year.

- Late Filing consequences involve the immediate payment of all due installments and adherence to the original payment schedule as if the filing were timely, emphasizing the importance of meeting filing deadlines.

- Penalties are enforced for non-compliance, including failure to file, late filing, or underpayment of estimated taxes, underscoring the need for accuracy and punctuality in tax-related matters.

Properly understanding and adhering to these guidelines when completing the NYC-400 form is crucial for corporations to comply with local tax laws, avoid penalties, and contribute to the economic structure of New York City.

Common PDF Documents

How to Fill Out Anti Arson Application - Serves as a legal requirement, reinforcing the seriousness of providing accurate and complete information when applying for insurance.

Dissolution of Llc - Includes a section for the filer’s name and address, ensuring accountability and correspondence regarding the dissolution.

Msc 150 - The form distinguishes between types of carrier operations, including interstate and intrastate classifications.