Free Nyc 399Z Form in PDF

The NYC 399Z form stands as a pivotal instrument for businesses operating within New York City's precincts, adjusting their fiscal responsibilities rooted deeply in the aftermath of the September 10, 2001, events. This nuanced document guides corporations and unincorporated entities through the maze of recalibrating depreciation deductions, especially for "qualified property," which, by standard regulations, would enjoy more generous terminologies under federal law, but are reconstrued through the lens of the city's specific mandates. Beyond its prima facie role, it intricately delineates the treatment of sport utility vehicles under Schedules A2 and B, grappling with both federal and city-dictated depreciation caps. Moreover, the document broadens its scope to encapsulate modifications in gain or loss upon disposals, aligning federal and city viewpoints to determine tax liabilities precisely. It then seamlessly transitions into adjustments in New York City income, as indicated in Schedule C, ensuring a comprehensive reconciliation between federally acknowledged depreciation practices and the city's articulated stance which, since the Economic Stimulus Act of 2008 and subsequent federal enactments, has witnessed a dynamic interplay of amendments crucial for taxpayers to comprehend. Importantly, the form meticulously outlines eligibility criteria, binding certain businesses to its tenets, thus underpinning its relevance in the broader context of tax reporting within the sophisticated tax landscape of New York City.

Nyc 399Z Sample

*00612291*

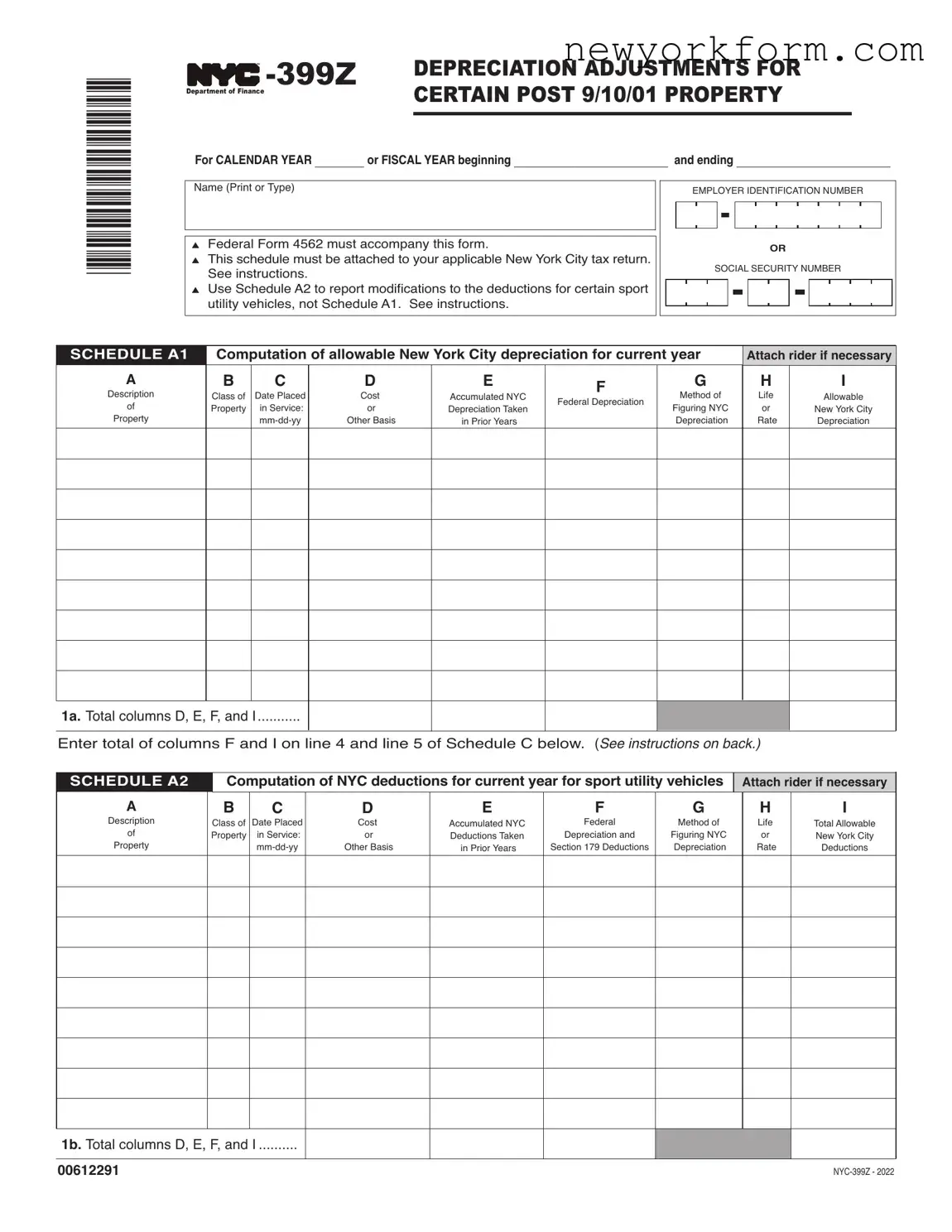

DEPRECIATION ADJUSTMENTS FOR |

|

|

CERTAIN POST 9/10/01 PROPERTY |

|

|

ForCALENDARYEAR________orFISCALYEARbeginning_________________________ andending_________________________

mentore)

▲ ederlormmustmpnthisorm |

|

|

▲ |

hissedulemustettedtourpplileeworit |

txreturn |

|

Seeinstruions |

|

▲ |

seSeduletoreportmodiitionstothededuionsor |

rtinsport |

|

utilitvehiesnotSeduleSeeinstruions |

|

|

|

|

OR

SS

SCHEDULE A1 |

Computation of allowable New York City depreciation for current year |

Attach rider if necessary |

|

|

|

A |

B |

C |

D |

E |

|

F |

G |

|

H |

|

I |

esption |

lsso |

ted |

ost |

multed |

|

thodo |

|

ie |

|

lowle |

|

|

ederlepretion |

|

|

||||||||

o |

pert |

inServi |

or |

epretionn |

|

iurin |

|

or |

|

eworit |

|

|

|

|

|

||||||||

pert |

|

mmd |

thersis |

inorers |

|

|

epretion |

|

te |

|

epretion |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a.otllumnsnd |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

tertotlolumnsndonlinendlineoS |

|

eduleelow |

See instructions on back.) |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE A2 |

Computation of NYC deductions for current year for sport utility vehicles |

Attach rider if necessary |

|||||||||

A |

B |

C |

D |

E |

|

F |

G |

|

H |

|

I |

esption |

lsso |

ted |

ost |

multed |

|

ederl |

thodo |

|

ie |

|

otllowle |

o |

pert |

inServi |

or |

eduionsn |

|

epretionnd |

iurin |

|

or |

|

eworit |

pert |

|

mmd |

thersis |

inorers |

Seioneduions |

epretion |

|

te |

|

eduions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b.otllumnsnd |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00612291 |

|

|

|

|

|

|

|

|

|

|

|

Form |

Page 2 |

|

|

SCHEDULE B

Disposition adjustment

Attach rider if necessary

oreitemopropertlistedelowdeterminethediere |

netweenederlndeworitdeduionsusedint |

hemputtionoederl |

|

ndeworittxleinmeinpriorrs |

|

|

|

▲ |

ederldeduionexedseworitdeduionsutr |

lumnromlumnndenterinlumn |

|

▲ |

eworitdeduionexedsederlsutrlumnro |

mlumnndenterinlumn |

|

A |

B |

C |

D |

E |

F |

G |

|

esption |

lsso |

ted |

otlederl |

otl |

justment |

justment |

|

|

pert |

inServi |

|||||

opert |

epretionn |

epretionn |

minus |

minus) |

|||

S) |

mmd |

||||||

|

|||||||

|

|

|

|

|

2. |

otlexssederldeduionsover deduions |

(see instructions) |

|

|

|

||||

3. |

otl exss deduionsoverederldeduions |

(see instructions) |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

SCHEDULE C |

Computation of adjustments to New York City income |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. ederl |

|

B. eworit |

|

|

|

|

|

|

|

|

|

|

|

4. |

termountromSedulelinelumn |

|

4. |

|

|

|

|

||

5. |

termountromSedulelinelumn |

|

5. |

|

|

|

|

||

6a. termountromSedulelineolumn |

|

6a. |

|

|

|

|

|||

6b.termountromSedulelineolumn |

|

6b. |

|

|

|

|

|||

7a. termountromSeduleline |

|

7a. |

|

|

|

|

|||

7b.termountromSeduleline |

|

7b. |

|

|

|

|

|||

8. |

otls lumnlinesndlumnlines |

nd |

8. |

|

|

|

|

||

terthemountonlinelumnsndditionndt |

hemountonlinelumnsdeduionontheppl |

ileeworitreturneinstr) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*00622291*

00622291

GENERAL INFORMATION

The NewYork CityAdministrative Code, as amended pursuant to the authority granted under Part G of Chapter 93 of the Laws of 2002, limits the depreciation deduction for "qualified prop- erty," other than "qualified Resurgence Zone property," to the deduction that would have been allowed for such property under IRC §167 had the property been acquired by the tax- payer on September 10, 2001, and therefore, not been eligible for the enhanced deductions allowed by the IRC §168(k). "Qualified Resurgence Zone property" is "qualified property" used substantially in the Resurgence Zone in connection with the active conduct of a trade or business where the original use began with the taxpayer in the Resurgence Zone after Sep- tember 10, 2001. The Resurgence Zone (defined in sections

gain or loss included in entire net income or unincorporated business entire net income upon the disposition of any property for which the federal and New York City depreciation deduc- tions differ.

NOTE

Deductions for "qualified Resurgence Zone property," are not affected by the above decoupling provisions other than for cer- tain sport utility vehicles. The additional

NOTE

Any exceptions to the decoupling provisions provided in the Administrative Code for Qualified New York Liberty Zone property or Qualified New York Liberty Zone leasehold im- provements as defined in IRC §1400L have expired.

Form |

Page 3 |

|

|

Economic StimulusAct of 2008 and

Other Federal Legislation Effecting Depre-

ciation.

Section 102 of the Economic Stimulus Act of 2008, Pub.L. No.

In 2015, Section 143 of the Protecting Ameri- cans from Tax Hikes Act of 2015, Pub. L. No.

Most recently, section 13201(b) of theTax Cuts and Jobs Act of 2017 (“TCJA”) extended the bonus depreciation deduction to cover property placedinservicebeforeJanuary1,2027(except for aircraft and

Under the TCJA, the first year depreciation limit increase of $8,000 for passenger automo- biles under §280(F)(a)(1)(A) is extended to in- clude automobiles placed in service on or before December 31, 2026. Prior to that, in order to qualify for the $8,000 increase in bonus depreciation, the passenger automobile would have had to been placed into service on or before December 31, 2019. This extension of the placed in service deadline only applies

to automobiles acquired on or after September 28, 2017. However, if the passenger automo- biles was acquired before September 28, 2018, the first year additional depreciation is phased down to $6,400 in the case of an automobile placed in service during 2018 and to $4,800 in the case of automobile placed in service during 2019.

However, as discussed above the Administra- tive Code limits the depreciation for “qualified property” other than “Qualified Resurgence Zone property” to the deduction that would have been allowed for such property had the property been acquired by the taxpayer on Sep- tember 10, 2001, and therefore, except for Qualified Resurgence Zone property, as de- fined in the Administrative Code, the City has decoupled from the federal bonus depreciation provision. The Administrative Code also re- quires appropriate adjustments to the amount of any gain or loss included in entire net in- come or unincorporated business entire net in- come upon the disposition of any property for which the federal and New York City depreci- ation deductions differ.

Special Provisions for Certain Sport Utility

Vehicles for Tax Periods Beginning on or

AfterJanuary 1, 2004

Under Section 280F of the Internal Revenue Code, the federal depreciation deduction under sections 167 and 168 of the Internal Revenue Code and the expense in lieu of depreciation deduction under section 179 of the Internal Revenue Code for certain passenger automo- biles are generally limited to the amounts pro- vided in section 280F(a)(1) of the Internal Revenue Code. Congress passed legislation that limits the amount deductible for certain sport utility vehicles. That legislation does not affect the modifications required for City tax purposes described below. For tax years begin- ning on or after January 1, 2004, in determining ENI of taxpayers, other than eligible farmers (for purposes of the New York State farmers' school tax credit), the amount allowed as a de- duction for NewYork City purposes (for either depreciation or expense in lieu of depreciation) with respect to a sport utility vehicle (SUV) that is NOT a passenger automobile for pur- poses of section 280F(d)(5) of the Internal Rev- enue Code is limited to the amount that would be allowed under section 280F(a)(1) of the In- ternal Revenue Code if the vehicle were a pas- senger automobile as defined in section 280F(d)(5). For all SUVs subject to these spe- cial provisions, the amount allowed as a de- duction is calculated as of the date the SUV was actually placed in service and not as of September 10, 2001. (The date that is applica- ble to qualified property, other than qualified Resurgence Zone property and New York Lib- erty Zone property, under the general post- 9/11/01 decoupling provisions).

On the disposition of an SUV subject to this limitation, the amount of any gain or loss in- cluded in ENI must be adjusted to reflect the limited deductions allowed for City purposes under this provision. See Finance Memoran- dum

Coordination of Federal depreciation and City decoupling provisions with respect to SUVs

As discussed above, the Economic Stimulus Act of 2008 amended IRC section 168(k) to provide bonus depreciation for certain property acquired in 2008. The Act also amended §168(k)(2)(F)(i) to increase the first year de- preciation allowed under §280F(a)(1)(A) by $8,000 for passenger automobiles to which the

WHO MUSTUSETHIS FORM

A corporation or unincorporated business that files or is included in a

●

●

●

●

Form |

Page 4 |

|

|

must use Form

1)it claims for federal purposes a deprecia- tion deduction for "qualified property" pursuant to the Economic StimulusAct of 2008, or subsequent federal legislation including the 2015 PATH Act or TCJA other than “Qualified Resurgence Zone property.”

2)it is not an eligible farmer (for purposes of the NewYork State farmers' school tax credit) and it claims for federal purposes a depreciation deduction or an expense deduction in lieu of depreciation deduc- tion under section 179 of the Internal Revenue Code for an SUV that is NOT a passenger automobile for purposes of sec- tion 280F(d)(5) of the Internal Revenue Code (regardless of whether the SUV is “qualified property” under IRC §168(k).

NOTE

Corporations and unincorporated businesses meeting the criteria set forth in #1 or #2 above are not permitted to file on Form

SPECIFIC INSTRUCTIONS

SCHEDULE A1

The purpose of this schedule is to compute the allowableNewYorkCitydepreciationdeduction. This form has been designed to be used with the federal depreciation schedule, Form 4562 (Rev. March2002orlater). Acopyofthefederalform must accompany this Form

Column A

Enter a brief description of each item of “qual- ified property,” other than “qualified Resur- gence Zone property,” included in part II or III of federal Form 4562.

Column B

For each item of property listed in column A, indicate the property class type used in com- puting the federal deduction. Use “UPM” for property which is depreciated under the unit of production method provided in IRC §168(f)(1).

ColumnD

The cost or other basis entered in this column must be the same amount used for federal pur- poses prior to any reduction for the special de- preciation allowance for qualified property.

ColumnG |

total amount that may be deducted for New |

||||

Indicate the depreciation method selected for |

York City purposes in the current tax year for |

||||

the computation of the New York City allow- |

an SUV subject to the special provisions. See |

||||

able depreciation deduction.Any method used |

Finance Memorandum |

||||

to compute depreciation that would have been |

IRC §280F Limits to Sport Utility Vehicles”. |

||||

allowed under IRC §167, had the property been |

|

|

|

|

|

acquired on September 10, 2001, will be ac- |

SCHEDULE B |

||||

ceptable. This includes such methods as |

|

|

|

|

|

Column A |

|

||||

depreciation, |

Enter each item of property disposed of during |

||||

or any other consistent method. |

the taxable year separately.Attach a rider if ad- |

||||

|

ditional room is needed. |

||||

Column I |

|

|

|

|

|

Enter depreciation computed by the method in- |

Column D |

|

|||

dicated in column G computed as IRC §167 |

Enter for each item of property the total amount |

||||

would have applied had the property been ac- |

of federal deductions used in the computation |

||||

quired on September 10, 2001. Total of this |

of prior years’ federal taxable income. For an |

||||

column will be the amount allowable as a de- |

SUV subject to the special provisions, the |

||||

duction for New York City. |

amount entered in Column D should include |

||||

any amount deducted under section 179 of the |

|||||

|

|||||

LINE 1a |

Internal Revenue Code. |

||||

|

|

|

|

||

Enter total of columns F and I on lines 4 and 5 |

Column E |

|

|||

of Schedule C, as indicated. |

|

||||

Enter for each item of property the total amount |

|||||

|

|||||

If you have disposed of “qualified property” |

of New York City deductions used in the com- |

||||

other than “qualified Resurgence Zone prop- |

putation of prior years’ New York City entire |

||||

erty,” in any year after the year of acquisition, |

net income. |

|

|||

you must complete Schedule B. |

Column F |

|

|||

|

|

||||

SCHEDULEA2 |

For any item of property, if column D exceeds |

||||

column E, subtract column E from column D |

|||||

|

|||||

ColumnA |

and enter the excess in this column. |

||||

|

|

|

|

||

Enter the year, make and model for each SUV. |

Column G |

|

|||

ColumnB |

For any item of property, if column E exceeds |

||||

column D, subtract column D from column E |

|||||

Indicate the property class type used or that |

|||||

and enter the excess in this column. |

|||||

would be used in computing federal deprecia- |

|

|

|

|

|

tion for each SUV. |

LINE 2 |

|

|

|

|

|

|

|

|

||

ColumnD |

Add the amounts in column F and enter the |

||||

total on line 2 and on Schedule C, line 7a. |

|||||

The amount entered in this column must be |

|||||

|

|

|

|

||

equal to the cost or other basis used for federal |

LINE 3 |

|

|

|

|

purposes prior to any special depreciation al- |

Add the amounts in column G and enter the |

||||

lowances for qualified property and prior to the |

total on line 3 and on Schedule C, line 7b. |

||||

expense in lieu of depreciation deduction al- |

|

|

|

|

|

lowed under section 179 of the Internal Rev- |

SCHEDULE C |

||||

enue Code. |

|

|

|

|

|

|

LINE 8 |

|

|

|

|

ColumnE |

Enter the amount on line 8A as an addition on |

||||

Enter the total New York City depreciation |

the applicable New York City tax return. Use |

||||

taken in prior years including, for years prior |

the following lines. Attach an explanation. |

||||

to 2018, the amount of any deduction taken |

|

|

|

|

|

under section 179 of the Internal Revenue |

|||||

Code for New York City purposes. |

Schedule B, line 6c |

||||

|

|||||

ColumnF |

- |

Schedule B, line 4 |

|||

For each SUV, enter the sum of the amount of |

- |

Schedule B, line 10c |

|||

the federal depreciation deduction taken and |

|||||

amount of any federal expense in lieu of de- |

|||||

preciation deduction taken under section 179 |

- |

Schedule B, line 14c |

|||

of the Internal Revenue Code for the current |

- |

Schedule B, line 8 |

|||

tax period. |

- |

Schedule B, line 11 |

|||

|

|||||

ColumnI |

|||||

The amount entered in column I should be the |

- |

Schedule B, Line 6 |

|||

Form |

Page 5 |

|

|

Enter the amount on line 8B as a deduction on the applicable New York City tax return. Use the following lines. Attach an explanation.

*If this form is for the reporting corporation, enter amounts on the appropriate lines in Col- umnA. For any other member of the combined group, enter amounts on the appropriate lines on Form

**If this form is for the designated agent, enter amounts in the appropriate column. For any other member of the combined group, enter amounts on the appropriate lines on Form

File Overview

| Fact Number | Description |

|---|---|

| 1 | The form NYC-399Z is designed to adjust depreciation for certain properties post 9/10/01 in New York City. |

| 2 | It includes sections for calculating allowable NYC depreciation, deductions for sports utility vehicles, and disposition adjustments. |

| 3 | Governing laws include the New York City Administrative Code and amendments from Part G of Chapter 93 of the Laws of 2002. |

| 4 | Qualified Resurgence Zone property refers to property used in specific areas of Manhattan, encouraging business activity there. |

| 5 | Adjustments on gain or loss from property disposition where federal and NYC deductions differ are required under the Administrative Code. |

| 6 | Depreciation adjustments do not affect deductions for qualified Resurgence Zone property other than for certain sports utility vehicles. |

| 7 | Economic Stimulus Act of 2008 and subsequent legislation affecting depreciation are taken into account but with NYC-specific modifications. |

| 8 | For tax periods beginning on or after January 1, 2004, special provisions apply to depreciation deductions for certain sports utility vehicles. |

| 9 | Form NYC-399Z must be used by corporations or unincorporated businesses filing specific NYC tax forms if claiming depreciation for qualified property or certain SUVs. |

Nyc 399Z: Usage Guidelines

The form NYC-399Z plays a crucial role for corporations and unincorporated businesses within New York City, especially in light of specific property depreciation adjustments following September 10, 2001. It is designed to make necessary adjustments to the depreciation deductions for "qualified property" as well as for certain Sport Utility Vehicles (SUVs), ensuring compliance with both New York City and federal tax requirements. Preparing this form requires attention to detail and an understanding of the assets involved. To help make this process as straightforward as possible, the following steps are compiled to aid in accurately completing the form.

- Identify Fiscal Year: Start by filling in the calendar year or the fiscal year beginning and ending dates at the top of the form.

- SCHEDULE A1 - Computation of Allowable New York City Depreciation:

- Provide a brief description of each piece of “qualified property” in Column A.

- In Column B, indicate the property class type used for federal depreciation purposes.

- Fill in the cost or other basis for the property in Column D, as utilized for federal purposes.

- Select the depreciation method for New York City purposes in Column G. This is based on what would have been allowed under IRC §167 as if the property had been acquired on September 10, 2001.

- In Column I, enter the New York City allowable depreciation for the current year, calculated as per the method indicated in Column G.

- SCHEDULE A2 - Computation of NYC Deductions for Sport Utility Vehicles:

- Enter the year, make, and model of each SUV in Column A.

- Indicate the federal property class in Column B.

- For Column D, fill in the cost or other basis used for federal tax purposes.

- In Column E, list the total New York City depreciation taken in all prior years.

- Column F should include the total of the federal depreciation and any expense deduction taken under section 179 of the Internal Revenue Code for the SUV for the current year.

- SCHEDULE B - Disposition Adjustment: If disposing of qualified property or an SUV, provide details of the property and the difference between federal and New York City depreciation used in prior years in Columns A through G.

- SCHEDULE C - Computation of Adjustments to New York City Income: Summarize the total adjustments to New York City income from SCHEDULES A1, A2, and B in SCHEDULE C to reflect the necessary additions or deductions on your New York City tax return.

After completing these steps, review the form thoroughly to ensure accuracy and completeness. All relevant riders and supporting documents, such as the federal depreciation schedule Form 4562, should be attached as necessary. Submit the completed form alongside your New York City tax return, making sure to include any adjustments in the specified lines of the return as instructed in SCHEDULE C. Understanding the nuances of this process helps in aligning depreciation methods between federal and city requirements, ultimately aiding in precise tax reporting and compliance.

FAQ

What is Form NYC-399Z used for?

Form NYC-399Z is required for businesses to adjust depreciation deductions for certain properties acquired post-September 10, 2001. It specifically calculates allowable New York City (NYC) depreciation for such properties, ensuring compliance with changes in the tax code that limit depreciation deductions to those that would have applied if the property had been acquired on September 10, 2001.

Who must file Form NYC-399Z?

Any corporation or unincorporated business filing NYC-3A, NYC-3L, NYC-4S, NYC-202, NYC-202EIN, NYC-204, NYC-1, NYC-2, NYC-2A, or NYC-2S, must use Form NYC-399Z under two conditions:

- If it claims a federal depreciation deduction for "qualified property" as per Economic Stimulus Act of 2008 or subsequent legislation, excluding "Qualified Resurgence Zone property."

- If it claims federal depreciation or a section 179 expense deduction for a Sport Utility Vehicle (SUV) not considered a passenger automobile under section 280F(d)(5) of the Internal Revenue Code, irrespective of the SUV being “qualified property” under IRC §168(k).

Are there any exceptions to filing Form NYC-399Z?

Certain sport utility vehicles (SUVs) and properties qualify for exceptions based on their use or designation, such as Qualified Resurgence Zone property, which are influenced by specific federal tax provisions and their application to the NYC Administrative Code. Also, exceptions apply to Qualified New York Liberty Zone property or leaseholds as outlined in IRC §1400L, which have expired.

What schedules are included in Form NYC-399Z?

Form NYC-399Z includes several schedules for different adjustments:

- Schedule A1 for computing allowable NYC depreciation,

- Schedule A2 for computing NYC deductions for certain SUVs,

- Schedule B for adjustment upon property disposition,

- Schedule C for adjustments to NYC income.

How does the Economic Stimulus Act of 2008 affect Form NYC-399Z?

The Act, along with subsequent federal legislation, amended IRC section 168(k), influencing bonus depreciation rates and applicable property acquisition dates. However, NYC has decoupled from the federal bonus depreciation for "qualified property" other than Qualified Resurgence Zone property for purposes of NYC taxation, requiring adjustments to be made using Form NYC-399Z.

What adjustments are required for sport utility vehicles?

For tax periods beginning on or after January 1, 2004, the depreciation deduction for SUVs not classified as passenger automobiles is limited. This limitation aligns the deduction amount with that of section 280F(a)(1) of the Internal Revenue Code, as if the SUV was a passenger automobile. Disposition of such SUVs requires adjustments to the amount of gain or loss included in entire net income or unincorporated business entire net income.

How do federal depreciation and City decoupling provisions coordinate for SUVs?

While federal legislation may extend or increase first-year depreciation benefits for SUVs, NYC specifically limits depreciation deductions for these vehicles unless they qualify as "Qualified Resurgence Zone property." This ensures a standard deduction rate is applied across both federal and city tax filings in specific cases.

What are the specific instructions for completing Schedule A1 and A2?

Schedule A1 focuses on calculating the allowable depreciation for NYC, requiring detailed input matching federal Form 4562. Schedule A2, for SUVs, requires details such as year, make, model, cost basis, and depreciation taken. Both schedules are critical for correctly adjusting depreciation deductions for NYC tax purposes.

What happens upon the disposition of property?

Schedule B addresses adjustments needed when "qualified property" is disposed of. If there’s a difference between federal and NYC depreciation deductions previously taken, adjustments on gain or loss included in income must reflect these differences, ensuring accurate taxable income reporting for NYC tax purposes.

Common mistakes

Filling out the NYC-399Z form, "Depreciation Adjustments for Certain Post 9/10/01 Property," is vital for certain businesses in New York City, but it can also be tricky. Mistakes on this form can lead to erroneous tax calculations and potential issues with the New York City Department of Finance. Here are five common mistakes to watch out for:

- Not attaching required riders: The form often necessitates additional documentation, particularly when the details of calculations can't fit within the provided spaces or when specific situations require further explanation. A common mistake is not attaching riders when necessary, causing incomplete submissions. Ensure all needed details and explanations are fully provided, using riders as instructed.

- Incorrectly calculating depreciation: The NYC-399Z requires adjustments to depreciation to align with specific New York City limitations, diverging from federal depreciation methods for certain properties. Incorrect calculation of these adjustments is a frequent error. Careful adherence to the instructions for Schedules A1 and A2, ensuring that the depreciation method aligns with the city's requirements, is crucial.

- Failure to adjust for SUV limitations: Specific rules apply to the depreciation and deduction for certain Sport Utility Vehicles (SUVs), which must be accounted for in Schedule A2. A common oversight is the failure to limit deductions for SUVs as required, leading to inaccurately high deduction claims. Understand the special provisions for SUVs to ensure compliance.

- Misunderstanding disposition adjustments: Schedule B requires adjustments for any disposed-of property where federal and New York City depreciation deductions previously differed. Errors often occur here, either through overlooking previous discrepancies or miscalculating the adjustment. Careful review of past deductions and precise calculations are needed to accurately reflect those adjustments.

- Inaccurate reporting of past deductions: When completing Schedules A2 and B, inaccuracies in reporting past deductions taken for New York City and federal purposes can lead to incorrect current year adjustments. This often stems from a misunderstanding or overlooking of past depreciation deductions or special deductions, such as those under section 179 of the Internal Revenue Code.

To avoid these issues, it's advisable to review the general and specific instructions provided with the form carefully. Consulting the instructions can clarify requirements for attachments, permissible depreciation methods, special provisions for certain types of property, and the accurate computation and reporting of past deductions. Proper attention to these instructions and thorough review of previously claimed deductions are essential steps toward accurate completion of the NYC-399Z form.

Lastly, consider seeking professional advice if uncertain. Tax laws and regulations can be complex, and professional guidance can help navigate these complexities, ensuring compliance and accurate tax reporting.

Documents used along the form

The Form NYC-399Z is a crucial document for businesses operating within New Beach City, especially in the wake of post 9/10/01 regulatory adjustments. This form, supporting the accurate computation and reporting of depreciation adjustments for eligible property, necessitates the accompaniment of several other forms and documents to ensure comprehensive compliance and optimal tax benefits. Understanding these complementary documents will empower businesses to navigate the complexities of tax filings effectively.

- Form 4562: Federal Depreciation and Amortization. This form details the depreciation and amortization expenses claimed for federal tax purposes. It is essential for computing allowable New York City depreciation, as adjustments on Form NYC-399Z are often based on the federal values reported.

- Schedule B: Disposition Adjustment. A supplemental schedule for Form NYC-399Z, this document records the adjustments required when there is a disposition of property, ensuring the difference between federal and New York City depreciation deductions is accurately reflected.

- Schedule C: Adjustments to New York City Income. Works alongside Form NYC-399Z to report necessary adjustments to income, stemming from the different treatment of depreciation between federal and city tax codes.

- Form NYC-3A, NYC-3L, or NYC-4S: For General Business Corporations. These forms are for corporate taxpayers and must be used in conjunction with Form NYC-399Z if modifications to depreciation are claimed at a federal level or to report the depreciation of certain sport utility vehicles.

- Form NYC-202, NYC-202EIN, or NYC-204: For Unincorporated Businesses. Similar to the corporate forms, these documents are necessary for unincorporated businesses that claim federal depreciation differences or need to report on SUV depreciations and must accompany the NYC-399Z.

- Form NYC-1: For Banking Corporations. Banking institutions filing NYC-399Z must use Form NYC-1 to report their business income and calculate tax due, integrating any depreciation adjustments made.

- Finance Memorandum 21-1: Application of IRC §280F Limits to Sport Utility Vehicles. This memorandum provides guidelines on how to apply limits to the depreciation and expensing of SUVs for city tax purposes, crucial for businesses using SUVs significantly in their operations.

Complementary to Form NYC-399Z, these documents ensure businesses accurately report and adjust their tax obligations in light of New York City’s specific requirements. Adequate preparation and understanding of each form’s role in the reporting process can significantly streamline the compliance efforts of businesses in New York City. With diligence and attention to detail, businesses can leverage these forms to achieve both compliance and optimization of their tax positions.

Similar forms

The NYC-399Z form, outlining depreciation adjustments for specific property post-September 10, 2001, shares similarities with several other tax documents focused on asset depreciation and adjustments for tax purposes. One such document is the IRS Form 4562, "Depreciation and Amortization." This form is used to claim depreciation on properties, including vehicles, equipment, and buildings for federal taxes. Both forms require detailed calculations of property costs, useful life, and methods of depreciation, making them essential for businesses to accurately report asset depreciation and, in the case of the NYC-399Z, make necessary adjustments for New York City tax purposes.

Another related document is the IRS Schedule C, "Profit or Loss from Business (Sole Proprietorship)." Specifically, when a sole proprietor reports business income and expenses, they must account for the depreciation of assets used in the business. The NYC-399Z form and Schedule C intersect where individuals declare deductions for business use of property, requiring adjustments due to specific post-9/11 legislation affecting properties in New York City.

The IRS Form 4797, "Sales of Business Property," also parallels the NYC-399Z form in its function. Form 4797 is used to report the sale or exchange of property used in a trade or business, which may include properties that have been depreciated. Similarly, NYC-399Z includes schedules for reporting the disposition of property and adjustments based on the difference between federal and New York City depreciation deductions, reflecting their shared objective of adjusting gains or losses for tax purposes.

The IRS Form 8824, "Like-Kind Exchanges," involves reporting deferral of taxes due on the exchange of certain types of properties. When businesses execute a like-kind exchange involving qualified property affected by post-9/11 depreciation rules in NYC, adjustments on the NYC-399Z form might be necessary. This similarity arises from the need to reconcile the tax implications of property exchanges with special depreciation rules, illustrating how both forms play crucial roles in tax planning and compliance for businesses.

The Form NYC-3A, used by corporations for General Corporation Tax in New York City, is similar to the NYC-399Z in that businesses operating in NYC must report and adjust their income and deductions, including depreciation, to comply with local tax regulations. Both forms cater to entities navigating the complexities of tax liabilities in the context of NYC's unique legislative environment following 9/11.

Similarly, the Form NYC-202, for Unincorporated Business Tax, echoes the necessity found in the NYC-399Z of modifying federal taxable income and deductions to meet specific NYC regulatory requirements. Unincorporated businesses, like their incorporated counterparts, must make depreciation adjustments reflective of NYC's guidelines, underscoring the cohesion between these forms in maintaining tax compliance within the city.

The Economic Stimulus Act of 2008, while not a tax form, introduced tax provisions that affect the depreciation of properties, offering enhanced first-year depreciation deductions for certain properties. The rules and modifications resulting from this act have direct implications on the reporting and calculations done on the NYC-399Z form, where specific post-9/11 NYC adjustments override federal bonuses, making an understanding of both essential for accurate tax reporting.

Lastly, the Special Provisions for Certain Sport Utility Vehicles under Section 280F of the Internal Revenue Code, which limits depreciation deductions for certain vehicles, resembles the adjustments required for sport utility vehicles on the NYC-399Z form. Both set of rules demand specific calculations to account for the depreciation of vehicles used in business, ensuring that tax liabilities reflect the intended legislative benefits and limitations. These provisions underscore the interplay between federal tax legislation and local NYC tax rules affecting business property.

Dos and Don'ts

When it comes to handling the NYC-399Z form, which is crucial for computing depreciation adjustments for certain post-9/10/01 property, precision and attentiveness are key. To assist you in this process, below is a comprehensive list of dos and don'ts:

Things You Should Do

-

Read the instructions thoroughly: Before filling out the form, ensure you understand each section by reading through the instructions provided. This will help avoid common mistakes.

-

Use the federal depreciation schedule: This form must be used alongside the federal depreciation schedule, Form 4562. Ensure a copy of the federal form accompanies this form.

-

Check property classification: Make sure to accurately classify each property type as indicated in the form, especially for Schedule A1 and A2, as this affects depreciation calculations.

-

Accurately report the cost or other basis: Enter the correct amounts in column D for Schedule A1 and A2, reflecting the cost used for federal purposes before any special depreciation allowance or section 179 deductions.

-

Review prior deductions: For the disposition adjustment in Schedule B, properly calculate and enter the total amount of federal and New York City deductions used in previous years.

-

Sign and date the form: After completing the form, don’t forget to sign and date it, as failing to do so may result in processing delays.

Things You Shouldn't Do

-

Don’t guess on numbers: Ensure all figures entered, especially in columns related to cost basis and previous deductions, are accurate and verifiable.

-

Avoid incomplete entries: Do not leave any required fields blank. Incomplete entries could result in the form being rejected or returned.

-

Don’t use incorrect property classifications: Misclassifying property can lead to incorrect depreciation calculations and potentially undervalued deductions.

-

Don’t overlook the addition of a rider: If more space is needed, especially for Schedule B, attach a rider instead of trying to cram information into a limited space.

-

Avoid late filing: Make sure to submit the form within the specified deadlines to avoid penalties or interest on late filings.

-

Don’t ignore the specific instructions for SUVs: For any sport utility vehicles, carefully follow the guidelines as outlined in Schedule A2 and the special provisions section.

Misconceptions

- Misconception 1: The form is only for large corporations – Incorrect. The NYC 399Z form must be used by any corporation or unincorporated business that claims depreciation for "qualified property," not just large corporations. This includes entities filing NYC-3A, NYC-3L, NYC-4S, NYC-202, NYC-204, and others under specific criteria.

- Misconception 2: "Qualified Resurgence Zone property" does not need to be reported – This is false. While special rules apply, adjustments for such property still need to be reported on the NYC 399Z form to ensure that New York City tax liabilities are accurately calculated, especially for property used substantially within the Resurgence Zone.

- Misconception 3: The form is only applicable to property acquired after 9/11 – The form applies to "qualified property," including property acquired before and after September 10, 2001, but with adjustments based on whether it would have qualified for depreciation as if acquired on September 10, 2001.

- Misconception 4: Only physical property depreciation is covered – Incorrect. The form also requires adjustments for any gain or loss on the disposition of property for which federal and New York City depreciation deductions differ, including intangible properties.

- Misconception 5: Federal bonus depreciation automatically applies to NYC taxes – False. New York City enacted decoupling provisions, meaning the city does not automatically follow federal bonus depreciation rules, especially for properties acquired after specific dates outlined in federal statutes like the Economic Stimulus Act of 2008 and TCJA.

- Misconception 6: The form is straightforward and doesn't require detailed records – On the contrary, detailed calculation and extensive record-keeping are necessary to accurately complete the form, including federal Form 4562 documentation for comparison.

- Misconception 7: Special SUV provisions apply only to certain businesses – In reality, special provisions for the depreciation of certain sport utility vehicles apply broadly, affecting how depreciation deductions for SUVs are calculated for almost all businesses, not just specific industries or sectors.

- Misconception 8: The NYC-399Z form is an annual requirement for all businesses – This is inaccurate. Only those businesses that meet specific criteria regarding property depreciation, acquisition dates, and the type of tax form filed must submit this form alongside their regular tax filings.

- Misconception 9: Filing the NYC-399Z form is optional if your accountant advises against it – This is misguided advice. Compliance with filing the NYC-399Z is mandatory for eligible entities to accurately compute and report New York City taxes. Relying solely on an accountant's opinion without understanding the form's requirements could lead to errors in tax reporting and potential penalties.

There are several misconceptions regarding the NYC 399Z form, which merit clarification to ensure accurate and compliant submission:

Key takeaways

Understanding the intricacies of the NYC-399Z form is paramount for businesses operating in the wake of post-9/10/01 adjustments and federal legislations affecting depreciation. Here are four key takeaways vital for anyone navigating the fiscal landscape of New York City:

- Eligibility and Purpose: This form is tailored for corporations or unincorporated businesses that have availed themselves of federal depreciation deductions for "qualified property" under recent economic stimulus acts or the Tax Cuts and Jobs Act, excluding "Qualified Resurgence Zone property." Its primary function is to align New York City depreciation deductions with federal deductions while accounting for any adjustments due to legislation changes post-September 10, 2001.

- Special Considerations for SUVs: The form has provisions that specifically address depreciation and deductions for certain sport utility vehicles (SUVs), distinct from other qualified properties. For tax years beginning on or after January 1, 2004, the New York City deduction for an SUV is capped at the limit that would be applied if the SUV were categorized as a passenger automobile under section 280F(d)(5) of the IRC.

- Reconciliation of Discrepancies: A critical aspect of this form is its role in reconciling discrepancies between federal and New York City depreciation deductions, including adjustments for any gain or loss on property disposition. This involves detailed computations in Schedules B and C, ensuring that businesses correctly reflect these differences in their NYC tax returns.

- Integration with Federal Depreciation Practices: The NYC-399Z requires information from the federal depreciation schedule, Form 4562, to be used in the calculation of allowable NYC depreciation. This linkage underscores the necessity of harmonizing federal and city tax filings, reminding taxpayers of the importance of consistent documentation across both levels.

In conclusion, navigating the NYC-399Z demands a nuanced understanding of both federal and city tax laws regarding depreciation, especially in the context of post-9/11 legislation, the Economic Stimulus Act of 2008, and the Tax Cuts and Jobs Act adjustments. Businesses must carefully evaluate their eligibility, especially in relation to SUVs, and meticulously compute their deductions to ensure compliance and optimize their tax positions in New York City.

Common PDF Documents

Notice of Appearance New York Supreme Court - Helpful tips for navigating the New York appellate system as a poor person seeking to challenge a Family Court decision, with steps to follow and common pitfalls to avoid.

Construction Rules and Regulations - A obligatory document for construction projects aiming to operate within the permissible noise levels set by NYC.