Free Nyc 245 Form in PDF

The NYC 245 form plays a crucial role for corporations operating within New York City by providing a means for them to report activities and assert their exemption from the General Corporation Tax or Business Corporation Tax. This form is applicable specifically to entities claiming not to be subject to these taxes, including both Business and General Corporations. Focused on a wide array of business activities ranging from the location of offices and places of business within the city, to the number of employees, transactions, and types of assets located or utilized in the city, the form demands detailed disclosures. Further elaborating on its importance, the instructions address various scenarios under which corporations might be liable or exempt from taxes, highlighting conditions for exemption and the repercussions of misfiling. Additionally, it delineates deadlines for submission based on the corporation's fiscal calendar, offering clarity on compliance schedules. Notably, the form serves not just as a procedural compliance tool but as a safeguard against potential tax liabilities, making accurate and timely filing imperative for corporations. With stipulations on who must file, including distinctions between S corporations and C corporations alongside specific requirements for non-profit organizations, the form encompasses a broad spectrum of corporate entities. Providing a clear path for corporations to either certify their tax-exempt status or identify their tax obligations, the NYC 245 form exemplifies the complex interplay between corporate activities and municipal tax regulations in New York City.

Nyc 245 Sample

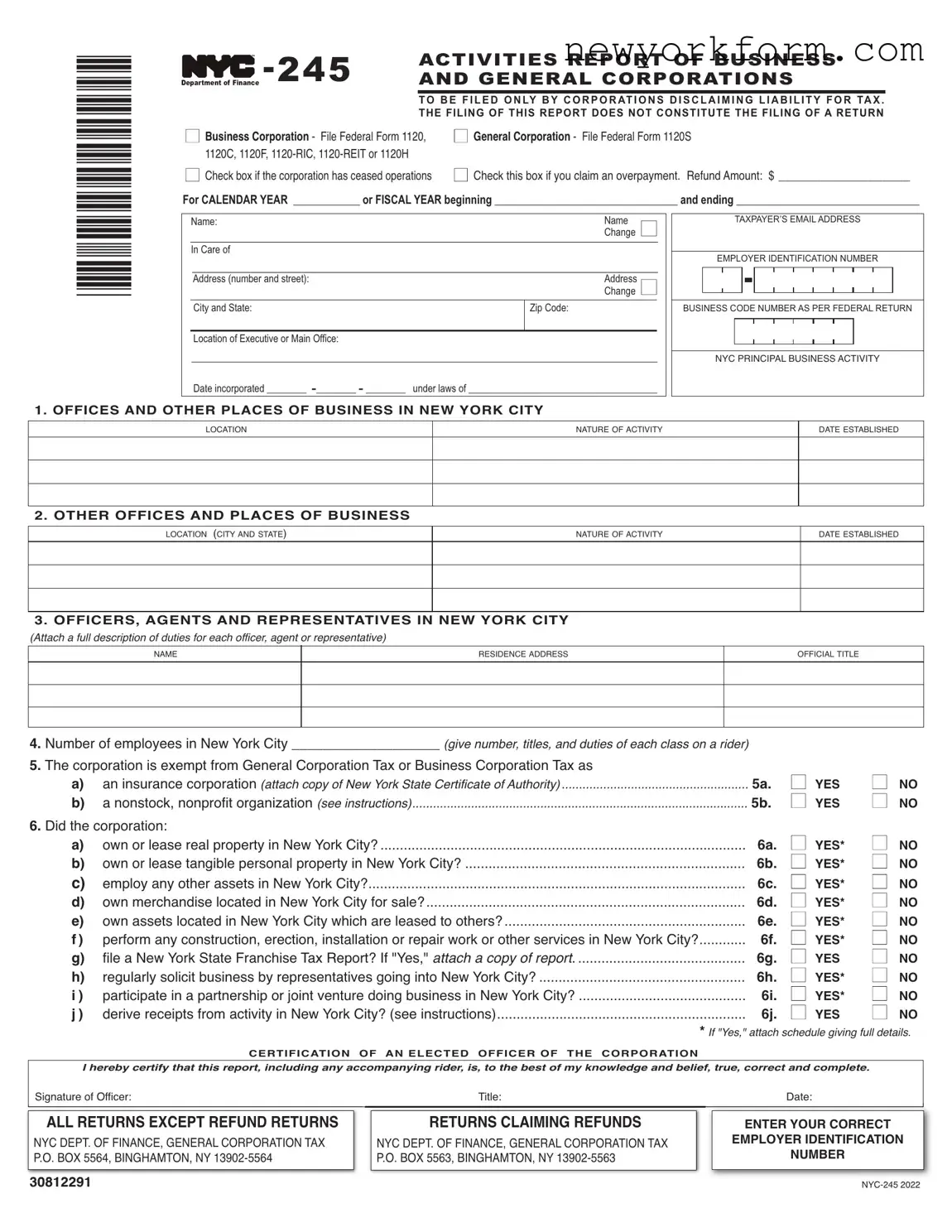

*30812291*

ACTIVITIES REPORT OF BUSINESS |

|

|

AND GENERAL CORPORATIONS |

|

TO B E F I L E D O N LY B Y C O R P O R AT I O N S D I S C L A I M I N G L I A B I L I T Y F O R TA X . |

|

THE FILING OF THIS REPORT DOES NOT CONSTITUTE THE FILING OF A RETURN |

■ BusinessCorporation- File Federal Form 1120, |

■ GeneralCorporation- File Federal Form 1120S |

1120C, 1120F, |

|

■ Check box if the corporation has ceased operations |

■ Check this box if you claim an overpayment. RefundAmount: $ ___________________ |

For CALENDAR YEAR ____________ or FISCAL YEAR beginning _________________________________ and ending _________________________________

Name: |

|

Name |

■ |

|

|

|

|

Change |

|

|

|

|

|

|

In Care of |

|

|

|

|

|

|

|

|

|

|

Address (number and street): |

|

Address |

■ |

|

|

|

Change |

|

|

|

|

|

|

|

City and State: |

|

Zip Code: |

|

|

|

|

|

|

|

Location of Executive or Main Office: |

|

|

|

|

|

|

|

|

|

Date incorporated ________ |

under laws of ______________________________________ |

||

TAXPAYER’S EMAIL ADDRESS

EMPLOYER IDENTIFICATION NUMBER

BUSINESS CODE NUMBER AS PER FEDERAL RETURN

NYC PRINCIPAL BUSINESS ACTIVITY

1. OFFICES AND OTHER PLACES OF BUSINESS IN NEW YORK CITY

|

LOCATION |

|

NATURE OF ACTIVITY |

|

DATE ESTABLISHED |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

OTHER OFFICES AND PLACES OF BUSINESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

LOCATION (CITY AND STATE) |

|

NATURE OF ACTIVITY |

|

DATE ESTABLISHED |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

OFFICERS, AGENTS AND REPRESENTATIVES IN NEW YORK CITY |

|

|

|||

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

|

NAME |

|

|

RESIDENCE ADDRESS |

OFFICIAL TITLE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. Number of employees in New York City ___________________ (

5.The corporation is exempt from General Corporation Tax or Business Corporation Tax as

a) an insurance corporation (w |

5a. |

■ YES |

■ |

NO |

b) a nonstock, nonprofit organization ( |

5b. |

■ YES |

■ |

NO |

6.Did the corporation:

a) |

own or lease real property in New York City? |

6a. |

■ YES* |

■ NO |

b) |

own or lease tangible personal property in New York City? |

6b. |

■ YES* |

■ NO |

c) |

employ any other assets in New York City? |

6c. |

■ YES* |

■ NO |

d) |

own merchandise located in New York City for sale? |

6d. |

■ YES* |

■ NO |

e) |

own assets located in New York City which are leased to others? |

6e. |

■ YES* |

■ NO |

f) |

perform any construction, erection, installation or repair work or other services in New York City? |

6f. |

■ YES* |

■ NO |

g) |

file a New York State Franchise Tax Report? If "Yes," |

6g. |

■ YES |

■ NO |

h) |

regularly solicit business by representatives going into New York City? |

6h. |

■ YES* |

■ NO |

i) |

participate in a partnership or joint venture doing business in New York City? |

6i. |

■ YES* |

■ NO |

j) |

derive receipts from activity in New York City? (see instructions) |

6j. |

■ YES |

■ NO |

|

|

* |

|

|

CERTIFICATION OF AN ELECTED OFFICER OF THE CORPORATION

I hereby certify that this report, including any accompanying rider, is, to the best of my knowledge and belief, true, correct and complete.

Signature of Officer:

ALLRETURNSEXCEPTREFUND RETURNS

NYC DEPT. OF FINANCE, GENERALCORPORATION TAX P.O. BOX 5564, BINGHAMTON, NY

30812291

Title:

RETURNSCLAIMINGREFUNDS

NYC DEPT. OF FINANCE, GENERALCORPORATION TAX P.O. BOX 5563, BINGHAMTON, NY

Date:

ENTER YOUR CORRECT

EMPLOYER IDENTIFICATION

NUMBER

Instructionsfor Form |

Page 2 |

|

|

This report must be filed by any corporation that has an officer, employee, agent, or repre- sentative in the City and claims not to be sub- ject to the NewYork City General Corporation Tax or Business Corporation Tax. For taxable years beginning in 1996 and thereafter, entities taxable as corporations for federal income tax purposesunderIRC§7701(a)(3)and§7704are considered corporations for purposes of the General Corporation Tax. Acorporationsub-

jecttoGeneralCorporationTaxorBusiness Corporation Tax cannot use this form; it must file a General Corporation Tax return, Form

A corporation is not required to file this report if it falls under one of the following:

1)thecorporationisexemptfromtheGeneral CorporationTaxunder

2)the corporation has received a letter from the Department of Finance exempting it from tax as a nonstock, nonprofit corpora- tion (see instructions for line 5b below), provided there has been no change in its character, activities or federal tax status since the date of that letter;

3)the corporation’s only tie with New York Cityisthatoneormoreofthecorporation’s officers, employees, agents or representa- tives reside in the City or come into the City infrequently in connection with iso- lated transactions of the corporation;

4)the corporation is a Real Estate Mortgage Investment Conduit (REMIC); or

5)the corporation is exempt from Federal in- come tax under IRC section 501(c)(2) or (25).

WHENTOFILE

Any S corporation required to file this report mustdosoannually,onorbeforeMarch15thif itreportsonacalendaryearbasisforfederalin- cometaxpurposes,oronorbeforethe15thday of the 3rd month following the close of its fis- cal year if it reports on a fiscal year basis.

Any C corporation required to file this report must do so annually, on or beforeApril 15th if itreportsonacalendaryearbasisforfederalin- cometaxpurposes,oronorbeforethe15thday of the 4th month following the close of its fis- cal year if it reports on a fiscal year basis.

LINE5b

Every corporation claiming exemption from General Corporation Tax or Business Corpora- tion Tax as a nonstock, nonprofit corporation (except for corporations exempt from federal income tax under IRC Section 501(c)(2) and

(25)mustapplyforan exemption fromthe De- partment of Finance by submitting an applica- tion for exemption containing an affidavit setting forth the following information about the corporation:

1)the type of organization;

2)the purposes for which it is organized;

3)a description of its actual activities;

4)the source and disposition of its income;

5)whetheranyofitsincomeiscreditedtosur- plusormayinuretoanyprivatestockholder or individual; and

6)such other facts that may affect its right to exemption.

The affidavit must be supplemented by: a copy of the articles of incorporation or articles of association, a copy of the bylaws, copies of statementsshowingthecorporation'sassetsand liabilities and receipts and disbursements for themostrecentyear,aphotostaticcopyofalet- terfromtheUnitedStatesTreasuryDepartment granting the corporation an exemption from federalincometaxationandphotocopiesoffed- eral, state and local tax returns filed by the or- ganization for the three most recent preceding years.

All of the above information should be sent to:

NYCDepartmentofFinance ExemptionProcessingUnit 59MaidenLane,20thFloor NewYork,NY 10038

There is no prescribed application form and no application fee.

LINE6

If you answer "yes" to any question, the corpo- ration may be subject to General Corporation Tax or Business CorporationTax. See "Corpo- rations Subject to Tax" for more information. Corporations subject to tax cannot use this form.

LINE6g

If the answer to question 6g is “yes,” state on a rider what activities take place elsewhere in New York State that do not also take place in New York City, or other reasons for filing a State Franchise Tax Report.

LINE6h

If the answer is "yes," see section

LINE6j

This question is only applicable to C corpora- tions. The term “deriving receipts from activ- ity” in New York City is defined in

CORPORATIONSSUBJECTTOTAX

A corporation subject to General Corpora- tion Tax or Business Corporation Tax can- not use this form; it must file either Form

1)doing business in New York City;

2)employing capital in New York City;

3)owning or leasing property in New York City, in a corporate or organized capacity;

4)maintaining an office in NewYork City; or

5)in the case of a C corporation, deriving re- ceipts from activity in New York City.

The term “doing business” is used in a com- prehensive sense and includesall activities that occupy the time or labor of people for profit. Regardless of the nature of its activities, every corporation organized for profit and carrying

Instructionsfor Form |

Page 3 |

|

|

out any of the purposes of its organization is deemed to be “doing business” for the purpose of the tax. In determining whether a corpora- tion is doing business, it is immaterial whether its activities actually result in a profit or a loss.

UndertheBusinessCorporationTaxapplicable to federal C Corporations for tax years begin- ning on or after January 1, 2015, a corporation is doing business in the city if:

(1)it has issued credit cards to onethousandor more customers who have a mailing ad- dress within the city as of the last day of its taxable year;

(2)it has merchant customer contracts with merchantsandthetotalnumberoflocations coveredbythosecontractsequalsonethou- sand or more locations in the city to whom thecorporationremittedpaymentsforcredit cardtransactionsduringthetaxableyear;or

(3)the sum of the number of customers de- scribed in item #1 plus the number of lo- cations covered by its contracts described in item #2 equals one thousand or more.

Additionally,fortaxyearsbeginningonorafter January 1, 2022, a corporation which does not meet the requirements of either (1), (2), or (3) above will be considered to be doing business inthecity,ifthecorporationhasatleasttencus- tomers,orlocations,orcustomersandlocations, as described above in (1), (2) and (3), the cor- poration is part of a unitary group AND if the number of customers, locations, or customers andlocations,withinthecityofthemembersof the unitary group that have at least ten cus- tomers,orlocations,orcustomersandlocations withinthecityintheaggregatemeetseither(1), (2), or (3) above.

For purposes of these provisions, the term “credit card” includes bank, credit, travel and entertainment cards. See Administrative Code Section

For tax years beginning on or after January 1, 2022, a C corporation will be subject to the Business Corporation Tax if it derives receipts from activity in the city and meets any one of the following:

(1)thereceiptswithinthecityare$1millionor more in a taxable year; or

(2)the corporation’s receipts from activity in thecityarelessthanonemilliondollarsbut at least ten thousand dollars in a taxable year and the corporation is part of a unitary group where the members that have at least

$10,000 of receipts within the city have, in the aggregate, receipts within the city of $1 million or more in a taxable year. SeeAd- ministrative Code Section

Theterm“employingcapital”includesanyofa large variety of uses, which may overlap other categories and give rise to taxable status. In general,theuseof assetsinstrumentalinmain- tainingoraiding thecorporateenterpriseorac- tivity in the City will create liability. Employing capital includes activities such as:

a)maintaining stockpiles of raw materials or inventories; and

b)maintaining securities in the City for trad- ing purposes.

Under Sections

a)the maintenance of cash balances with banks or trust companies or brokers in the City;

b)the ownership of shares of stock or securi- tieskeptintheCity,ifkeptinasafedeposit box, safe, vault or other receptacle rented for the purpose, or if pledged as collateral security, or if deposited with one or more banks or trust companies, or brokers who are members of a recognized security ex- change, in safekeeping or custody ac- counts;

c)the taking of any action by any such bank or trust company or broker which is inci- dental to the rendering of safekeeping or custodial service to the corporation;

d)the maintenance of an office in the City by oneormoreofficersordirectorsofthecor- poration who are not employees of the cor- poration as long as the corporation is not otherwise doing business or employing capital in the City and does not own or lease property in the City;

e)the keeping of books or records of a corpo- rationintheCityifthebooksorrecordsare not kept by employees of the corporation and the corporation is not otherwise doing business or employing capital in the City and does not own or lease property in the City; or

f)anycombinationoftheforegoingactivities.

In addition, a corporation will not be subject to the General Corporation Tax or Business Cor- poration Tax if its sole connection with New York City is:

(i)the maintenance of a statutory office at the address of its registered agent or the main- tenance of a mailing address; or

(ii)the mere ownership of shares of stock of corporations doing business in the City.

Under Administrative Code Section

For purposes of the Business Corporation Tax, an alien corporation that under any provision of the Internal Revenue Code is not treated as a “domesticcorporation”asdefinedinIRC§7701 and has no effectively connected income for the taxable year pursuant to clause (iii) of the open- ing paragraph of Administrative Code §11- 652(8)isnotsubjecttotheBusinessCorporation Tax for that taxable year. For purposes of the Business Corporation Tax, an alien corporation is defined as a corporation organized under the laws of a country, or any political subdivision thereof, other than the United States, or organ- ized under the laws of a possession, territory or commonwealth of the United States. See Ad- ministrative Code Section

NOTE: For additional guidance concerning what activities constitute "doing business," "employing capital," "owning or leasing prop- erty," and "maintaining an office" in NewYork City, see Sections

REFUNDS: If a corporation has previously paidtaxormadeestimatedtaxpaymentsforthe taxable year and is filing this form disclaiming liability for those taxes, the corporation should file a refund claim and attach this form to that claim.

File Overview

| Fact | Details |

|---|---|

| Purpose | Used by corporations disclaiming liability for New York City General Corporation Tax or Business Corporation Tax. |

| Applicable Entities | Any corporation with an officer, employee, agent, or representative in New York City claiming not to be subject to the taxes mentioned. |

| Non-Eligibility | Corporations subject to General Corporation Tax or Business Corporation Tax cannot use this form. |

| Non-Filing Situations | Corporations exempt under specific NYC Administrative Code sections or with limited NYC activities as outlined are not required to file. |

| Filing Deadline for S Corporations | Annually, by March 15 for calendar year reporters, or the 15th day of the 3rd month following the close of fiscal year. |

| Filing Deadline for C Corporations | Annually, by April 15 for calendar year reporters, or the 15th day of the 4th month following the close of fiscal year. |

| Exemption Application | Nonstock, nonprofit corporations claiming exemption must apply to the Department of Finance with detailed documentation. |

| Governing Law | New York City Administrative Code Sections applicable to tax liabilities and exemptions of corporations. |

| Limited Activities Exemption | Activities such as maintenance of cash balances or bookkeeping in NYC do not alone constitute doing business under the law. |

| Refund Claims | Corporations that have paid taxes or made estimated payments and disclaiming liability through this form must file a refund claim. |

Nyc 245: Usage Guidelines

Preparing the NYC-245 form is an important process for businesses that believe they are not subject to New York City's General Corporation Tax or Business Corporation Tax. This step-by-step guide will help you navigate through filling out this document. Before we dive into the steps, remember that this form serves as a report rather than a tax return, and its correct completion is crucial for your corporation's tax records. Make sure to have all necessary information at hand, including your business code number, employer identification number, and detailed information about your business activities in New York City.

- Start by entering the year you're reporting for, specifying whether it's for a calendar or fiscal year. Indicate the beginning and end dates for fiscal years.

- Fill out your corporation's name. If there has been a change in name since last filing, check the "Change" box.

- Provide the care of address, including number, street, city, state, and zip code. If there's been an address change, mark the "Change" box.

- Enter the location of your executive or main office.

- Specify the date your corporation was incorporated and under which laws.

- Include your taxpayer's email address and your employer identification number (EIN) for contact and identification purposes.

- Enter the business code number as per your federal return to classify your business activity appropriately.

- Detail the offices and other places of business your corporation has in New York City under Item 1.

- Under Item 2, list other offices and places of business outside of New York City.

- For Item 3, provide information on officers, agents, and representatives located within New York City.

- Indicate the number of employees in the city, if any.

- Answer whether your corporation leases or owns tangible property in the city, employs any assets in the city, or maintains an inventory for sale within city limits, among other specified activities from Items 6a through 6j.

- If you answered "Yes" to any activities not confined exclusively to New York City (Item 6g), attach a rider detailing these activities.

- For certification, an elected officer of the corporation must sign and date the form, attesting to the accuracy and completeness of the information provided.

After carefully filling out the NYC-245 form, review all the information for accuracy before submission. This form does not initiate the tax limitations period, meaning it doesn't replace the need for submitting a standard tax return for that purpose. Additionally, if during the year your corporation ceased doing business in the city, you are required to file a final return or request an extension. The aim of completing and filing this form rightly is to maintain compliance with city tax laws while correctly reporting your corporation's activity status. Always consult with a tax professional if you're unsure about any steps in this process to ensure compliance and accuracy in your filing.

FAQ

What is the NYC-245 form used for?

The NYC-245 form is specifically designed for corporations that have an officer, employee, agent, or representative in New York City and claim not to be subject to New York City General Corporation Tax or Business Corporation Tax. It is a report that must be filed annually by corporations disclaiming liability for these taxes.

Who needs to file the NYC-245 form?

Any corporation that operates within New York City but believes it is not subject to the city's General Corporation Tax or Business Corporation Tax due to its activities or status should file this form. However, if a corporation is actually subject to these taxes, it cannot use this form and must file the appropriate tax return.

When is the NYC-245 form due?

The due date for filing the NYC-245 form varies based on the corporation's tax reporting schedule. S corporations must file by March 15th if on a calendar year basis, or the 15th day of the 3rd month following the close of the fiscal year. C corporations have until April 15th for calendar year filings or the 15th day of the 4th month after their fiscal year ends.

Are there penalties for not filing the NYC-245 form?

While the document does not explicitly mention penalties specific to not filing the NYC-245 form, failing to comply with city tax reporting requirements generally results in penalties and interest on any taxes found to be due.

What information is required on the NYC-245 form?

Corporations must provide detailed information about their activities in New York City, including the locations of business, officers, agents, employees in the city, and various categories of tangible and intangible property or assets they have in the city. They must also certify their business activities and provide their Employer Identification Number (EIN) and business codes as per the federal return.

Can I file the NYC-245 form electronically?

The instructions do not specify the availability of electronic filing for the NYC-245 form. Typically, tax forms filed with the New York City Department of Finance can be submitted online, but it is advisable to consult the Department's website or contact them directly for the most current filing options.

What happens if I mistakenly file an NYC-245 form when my corporation is actually subject to tax?

If a corporation that is subject to the General Corporation Tax or Business Corporation Tax mistakenly files an NYC-245 form, it may need to correct its filing status by submitting the appropriate tax return form and could be liable for any unpaid taxes plus interest and penalties.

Is there a filing fee for the NYC-245 form?

There is no mention of a filing fee for the NYC-245 form in the instructions. Typically, reports such as this do not require a filing fee, but it's important to verify any updates or changes to filing requirements directly with the New York City Department of Finance.

If my corporation doesn't physically operate in New York City but has employees working remotely from the city, do we need to file an NYC-245 form?

Yes, if your corporation has employees, agents, or representatives working in New York City, even remotely, and you claim not to be subject to city taxes, you should file the NYC-245 form to report these activities.

How can I obtain an NYC-245 form?

The NYC-245 form can be obtained from the New York City Department of Finance's website. You can download the form directly from their site to ensure you have the most current version.

Common mistakes

Filling out forms for tax purposes is a common responsibility for corporations operating within various jurisdictions, including New York City. The NYC-245 form, also known as the Activities Report of Business and General Corporations, is a crucial document for corporations disclaiming liability for tax within the city. While the process might seem straightforward, errors can happen. Here are five common mistakes corporations make when completing this form:

- Incorrectly identifying the corporation type: The form differentiates between business corporations and general corporations. Confusion or misidentification at this early stage can lead to incorrect processing of the form, potentially affecting the corporation's tax liabilities.

- Failure to report all offices and places of business: The NYC-245 form requires corporations to list their offices and other places of business both within New York City and elsewhere. Overlooking or omitting some locations can give an inaccurate picture of the corporation's presence and activities, which is essential information for tax assessment purposes.

- Not updating officer, agent, and representative information: Section 3 of the form asks for details on officers, agents, and representatives in the city. Outdated or incomplete information can complicate compliance checks and correspondence related to the form.

- Omitting the certification signature: The form requires certification by an elected officer of the corporation, attesting to the correctness and completeness of the information provided. Missing signatures can result in the form being considered incomplete, delaying processing and potentially impacting the corporation's tax standing.

- Misunderstanding the eligibility to file Form NYC-245: Certain corporations may assume they are eligible to file this form, not realizing that their city activities actually subject them to General Corporation Tax or Business Corporation Tax. Misfiling can lead to penalties and the need to submit additional paperwork, including possibly the correct tax forms for those subjects to tax.

Corporations must give careful attention to the detailed instructions provided with the form to avoid these and other potential errors. By ensuring that all sections are accurately and fully completed, corporations can avoid the pitfalls of misreporting their activities, which could lead to fines, penalties, or complications with New York City tax authorities. It's always advisable to consult with a tax professional or legal advisor when preparing complex forms like the NYC-247 to ensure compliance with all city tax regulations.

Documents used along the form

When businesses in New York City claim they are not subject to the New York City General Corporation Tax or Business Corporation Tax, they must file the NYC 245 form. This form acts as a critical piece in ensuring compliance with city tax regulations, but often, additional documents are needed to support the information provided. Understanding these additional forms and documents can help businesses navigate the legal and administrative landscape more effectively.

- Form NYC-4S: This form is used by corporations subject to the General Corporation Tax. It is for S Corporations filing within New York City and helps detail income, deductions, and tax credits specific to the city’s taxation requirements.

- Form NYC-2 or NYC-2S: Targeted to C Corporations, these forms are essential for business corporation tax filings. They collect comprehensive financial information, which assists in calculating the tax liability based on business activities within New York City.

- Form NYC-EXT: This application allows businesses an extension of time to file their tax returns, including the General Corporation Tax or Business Corporation Tax returns. It is especially useful for corporations that cannot meet the filing deadline.

- Letter of Exemption: A document from the Department of Finance stating exemption from city taxes. This is crucial for non-profit organizations or businesses that have been deemed exempt from specific taxes by the city. To obtain this, companies must provide detailed information proving their eligibility for such an exemption.

- Form NYC-3L: Primarily for larger corporations, this form details the business activities and financial dealings relevant to taxation under the General Corporation Tax. It's designed to capture the broader scope of operations characteristic of larger entities.

Together, these forms and documents play a vital role in the tax filing process for corporations operating within New York City. They ensure businesses can accurately report their activities and financial status, claim potential exemptions, and ultimately comply with the city's taxation laws. It's important for corporations, whether they are small or large, to accurately understand and utilize these documents in conjunction with the NYC 245 form to maintain good standing and avoid potential legal complications.

Similar forms

The NYC 245 Activities Report form is closely related to the Federal Form 1120 (U.S. Corporation Income Tax Return) due to its role in business taxation processes. Similar to the NYC 245 form, which corporations utilize to report activities for tax purposes without actually filing a tax return in New York City, Form 1120 serves as the federal tax return for corporations in the United States. Both are mandatory filings for corporations operating within their respective jurisdictions, designed to report income, profits, and losses. However, while the NYC 245 specifically disclaims liability for certain city taxes, Form 1120 calculates federal income tax liability.

Form NYC-4S, for General Corporation Tax Return, shares a common goal with the NYC 245 form, as both involve the reporting of business activities within New York City. Corporations that are fully operational in NYC use Form NYC-4S to calculate and report the general corporation tax due to the city. In contrast, the NYC 245 is for those claiming exemption from these taxes, still requiring those corporations to report their presence and activities. Both forms help the city track corporate activities and ensure appropriate taxation.

Form NYC-2, the Business Corporation Tax Return, is another document with a similar purpose to the NYC 245 form. It is designed for corporations to report their earnings and calculate the business corporation tax owed to New York City. While the NYC 245 form is used by corporations to report activities without claiming tax liability, both forms play crucial roles in the city’s corporate taxation framework, ensuring businesses contribute their fair share to municipal finances.

The Form 990 (Return of Organization Exempt From Income Tax) parallels the NYC 245 form in its focus on tax exemption. Non-profit organizations use Form 990 to provide the IRS with financial information, proving their exemption from federal income taxes. Similarly, corporations use the NYC 245 to assert activities in NYC that, they claim, do not subject them to certain city taxes. Both forms are critical for entities to maintain their tax-exempt status, albeit in different tax jurisdictions.

Schedule C (Profit or Loss from Business), part of the personal income tax return, although different in its targeted filer, resembles the NYC 245 form in intent. Schedule C allows individuals to report profits and losses from their sole proprietorship businesses, similar to how the NYC 245 form lets corporations report their business activities in NYC. Both documents are vital for tax reporting purposes, allowing accurate assessment of tax liabilities or exemption claims.

Form W-9 (Request for Taxpayer Identification Number and Certification) is utilized in the tax reporting process, much like the NYC 245 form. The Form W-9 is often required by financial institutions and other entities to accurately report income paid to individuals or corporations, which relates to how the NYC 245 form is used by corporations to report activities that establish their tax responsibilities or exemptions in New York City.

Form NYC-EXT, used for requesting an extension of time to file a NYC tax return, operates in the same regulatory space as the NYC 245 form. Both forms interact with New York City’s Department of Finance, allowing businesses more flexibility in their reporting requirements. While the NYC-EXT grants additional time for filing detailed returns, the NYC 245 offers a way for corporations to report their presence and business activities without filing a complete tax return.

Form SS-4 (Application for Employer Identification Number) and the NYC 245 form are linked through their role in business identification and tax reporting. While Form SS-4 is used to apply for a unique identifier for federal tax purposes, the NYC 245 form requires this identifier as part of its reporting process. This connection underscores the importance of accurate identification in managing tax obligations and exemptions.

The Statement of Information (varies by state but generally referred to as Form SI in many states) mirrors the NYC 245 form in its functionality of reporting business activities and details. Required annually or biennially, depending on the state, these forms update the state on the corporation's information, similar to how the NYC 245 informs New York City of a corporation's activities and claims of tax exemption.

The Application for Tax Exemption, while not a single standardized form due to variations across different jurisdictions and tax statuses, resembles the NYC 245 in its essence. Both types of documents are pivotal for entities seeking to establish or maintain exemption from certain tax obligations, whether at the federal, state, or city level. Specifically, the NYC 245 form is used by corporations claiming an exemption from New York City’s business and general corporation taxes, a process paralleled by various exemption applications in other tax contexts.

Dos and Don'ts

When you're filling out the NYC 245 form, there are several do's and don'ts to keep in mind to ensure the process goes smoothly and your report is filed correctly.

- Do read the instructions thoroughly before you start filling out the form to ensure you understand what information is required and how to provide it.

- Do make sure you have all the necessary information on hand, including your Employer Identification Number (EIN), business code number as per your federal return, and any specific details about your corporation’s activities and locations in New York City.

- Do answer all the questions on the form accurately to the best of your knowledge, especially those concerning business activities in New York City, as this can affect your tax liability.

- Don’t leave any sections incomplete unless they truly do not apply to your corporation. Incomplete forms can lead to processing delays or requests for additional information.

- Don’t guess or approximate answers, especially when it comes to numbers like the Employee Identification Number (EIN) or the number of offices or employees in the city. Inaccuracies can raise questions about your filing and potentially trigger an audit.

- Don’t file the NYC 245 form if your corporation doesn’t meet the specific criteria for disclaiming tax liability, such as not doing business, employing capital, owning or leasing property, or maintaining an office in New York City. Ensure you check the eligibility requirements before submitting.

Staying organized, providing complete and accurate information, and understanding the form's requirements can make filing your NYC 245 form a straightforward task. Remember to double-check your responses and supporting documents before submitting to ensure everything is in order.

Misconceptions

Understanding the NYC-245 form is essential for corporations operating within New York City, especially those claiming not to be subject to the New York City General Corporation Tax or Business Corporation Tax. However, misconceptions about the form and its requirements can lead to confusion and, possibly, non-compliance. Below are eight common misconceptions dispelled to aid in a clearer understanding of the NYC-245 form and its purpose.

Any corporation can file the NYC-245 form: This form is specifically for corporations that have a presence in New York City but claim they are not subject to New York City General Corporation Tax or Business Corporation Tax. Corporations subject to these taxes must file a different form.

Filing the NYC-245 form is equivalent to filing a tax return: Filing this form does not constitute the filing of a tax return. To start the limitations period for tax assessments, a corporation must file the appropriate General Corporation Tax return or Business Corporation Tax return.

There is no deadline for filing the NYC-245 form: S corporations must file by March 15 if reporting on a calendar year basis or by the 15th day of the 3rd month following the close of their fiscal year. C corporations have their respective deadlines on April 15 and the 15th day of the 4th month following their fiscal year’s end.

All corporations doing business in New York City are required to file this form: Only corporations that claim they are not subject to the specified city taxes need to file this report. Certain exemptions apply, such as for corporations exempt under specific sections of the Administrative Code or for those whose activities in the city are minimal and meet certain criteria.

Submitting the NYC-245 form exempts a corporation from all NYC taxes: The form is a declaration of no liability for specific taxes, not an exemption from all city taxes. Corporations might still be liable for other taxes or fees.

There is no need to provide detailed activity information in the form: Detailed information about the corporation’s activities, like the number of employees in the city, leases, and representation in the city, is required to assess the corporation's tax liability accurately.

Corporations can file the form even after ceasing operations in NYC within the tax year: Corporations that have ceased doing business in the city during the taxable year cannot use this form and must file a final return or request an extension to file such a return.

The form only pertains to corporate income tax: While focused on General Corporation Tax and Business Corporation Tax, the form also deals with property, presence, and sales activities which might affect other tax liabilities.

Correct understanding and handling of the NYC-245 form ensure compliance with tax regulations, avoiding potential fines and penalties. It's crucial to consult with a tax professional or the Department of Finance for specific queries or clarifications regarding your corporation's obligations.

Key takeaways

- The NYC-245 form is specifically designed for corporations that operate within New York City but claim they are not subject to the New York City General Corporation Tax or Business Corporation Tax.

- This form must be filed by corporations that have an officer, employee, agent, or representative within the city, yet assert that they do not owe the specific taxes.

- Certain entities, such as those considered corporations for federal income tax purposes under IRC §7701(a)(3) and §7704, are also required to file this form if claiming exemption from the specified NYC taxes.

- Corporations that are actually subject to the General Corporation Tax or Business Corporation Tax cannot use this form and must file appropriate tax returns instead.

- Filing the NYC-245 form does not start the limitations period for tax assessments, which is only triggered by filing a proper tax return.

- Corporations that cease doing business in NYC during the taxable year cannot use this form and must file a final return or request an extension for a final return.

- Exemptions from filing are available for certain types of corporations, such as those exempt under specific sections of the Administrative Code, nonstock nonprofit corporations meeting certain conditions, and entities with minimal connections to NYC like having officers or employees residing in the city without further business activities.

- The form's filing deadlines vary by corporation type: S corporations must file by March 15th or the 15th day of the 3rd month following a fiscal year's close, while C corporations file by April 15th or the 15th day of the 4th month after a fiscal year ends.

- Answers on the form that indicate possible tax obligations, such as owning, leasing, or employing assets in the city, require careful consideration as they may subject the corporation to the General Corporation Tax or Business Corporation Tax.

Common PDF Documents

Nyc Pba 14 - An exclusive dental claim form for NYPD members, necessitating explicit details on dental treatments, patient relationships, and dentist certifications.

Nyc-1127 - Specific guidelines for those with extensions on federal or state tax returns.