Free Ny It 370 Form in PDF

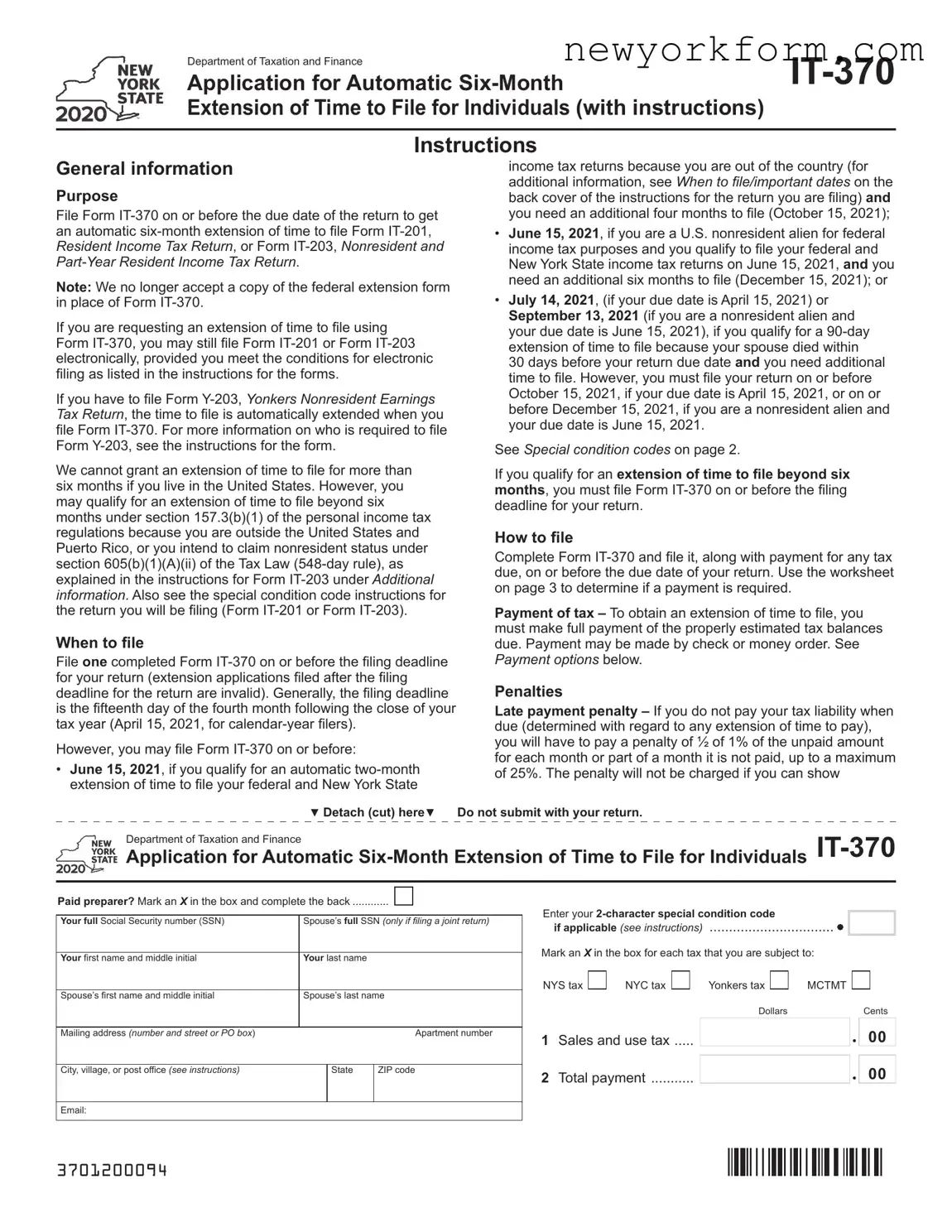

Filing taxes can often feel like a race against the clock, especially when life's hurdles get in the way. Recognizing this, the Department of Taxation and Finance provides New Yorkers a lifesaver in the form of the IT-370 form. This document is an Application for Automatic Six-Month Extension of Time to File for Individuals, offering a much-needed reprieve for those who can't meet the original filing deadline. It grants an automatic six-month extension to file either Form IT-201, the Resident Income Tax Return, or Form IT-203, the Nonresident and Part-Year Resident Income Tax Return. It's important to note the shift away from accepting federal extension forms in lieu of the IT-370, emphasizing its significance. For those facing extraordinary circumstances, such as living outside the United States or dealing with a spouse's recent death, there are provisions in place for an even longer extension under specific conditions. The form also adapts to modern conveniences, allowing for electronic filing under certain conditions, thus streamlining the process for busy taxpayers. Additionally, the form includes space for those who must also file a Yonkers Nonresident Earnings Tax Return, simplifying the process by connecting the extension to this requirement. Submitting the IT-370 by the due date with any tax due using the provided worksheet ensures taxpayers avoid late penalties and interest, a crucial step in maintaining financial integrity while navigating tax responsibilities.

Ny It 370 Sample

Department of Taxation and Finance |

|

||

Application for Automatic |

|||

Extension of Time to File for Individuals (with instructions) |

|

||

|

|

||

Instructions |

|

||

General information |

income tax returns because you are out of the country (for |

||

Purpose |

additional information, see When to file/important dates on the |

||

back cover of the instructions for the return you are filing) and |

|||

File Form |

you need an additional four months to file (October 15, 2021); |

||

an automatic |

• June 15, 2021, if you are a U.S. nonresident alien for federal |

||

Resident Income Tax Return, or Form |

income tax purposes and you qualify to file your federal and |

||

New York State income tax returns on June 15, 2021, and you |

|||

Note: We no longer accept a copy of the federal extension form |

need an additional six months to file (December 15, 2021); or |

||

• July 14, 2021, (if your due date is April 15, 2021) or |

|||

in place of Form |

|||

If you are requesting an extension of time to file using |

September 13, 2021 (if you are a nonresident alien and |

||

your due date is June 15, 2021), if you qualify for a |

|||

Form |

extension of time to file because your spouse died within |

||

electronically, provided you meet the conditions for electronic |

30 days before your return due date and you need additional |

||

filing as listed in the instructions for the forms. |

time to file. However, you must file your return on or before |

||

If you have to file Form |

October 15, 2021, if your due date is April 15, 2021, or on or |

||

before December 15, 2021, if you are a nonresident alien and |

|||

Tax Return, the time to file is automatically extended when you |

|||

your due date is June 15, 2021. |

|

||

file Form |

|

||

Form |

See Special condition codes on page 2. |

|

|

We cannot grant an extension of time to file for more than |

If you qualify for an extension of time to file beyond six |

||

six months if you live in the United States. However, you |

months, you must file Form |

||

may qualify for an extension of time to file beyond six |

deadline for your return. |

|

|

months under section 157.3(b)(1) of the personal income tax |

How to file |

|

|

regulations because you are outside the United States and |

|

||

Puerto Rico, or you intend to claim nonresident status under |

Complete Form |

||

section 605(b)(1)(A)(ii) of the Tax Law |

|||

due, on or before the due date of your return. Use the worksheet |

|||

explained in the instructions for Form |

|||

on page 3 to determine if a payment is required. |

|||

information. Also see the special condition code instructions for |

|||

|

|

||

the return you will be filing (Form |

Payment of tax – To obtain an extension of time to file, you |

||

When to file |

must make full payment of the properly estimated tax balances |

||

due. Payment may be made by check or money order. See |

|||

File one completed Form |

Payment options below. |

|

|

for your return (extension applications filed after the filing |

Penalties |

|

|

deadline for the return are invalid). Generally, the filing deadline |

|

||

is the fifteenth day of the fourth month following the close of your |

Late payment penalty – If you do not pay your tax liability when |

||

tax year (April 15, 2021, for |

due (determined with regard to any extension of time to pay), |

||

However, you may file Form |

you will have to pay a penalty of ½ of 1% of the unpaid amount |

||

for each month or part of a month it is not paid, up to a maximum |

|||

• June 15, 2021, if you qualify for an automatic |

|||

of 25%. The penalty will not be charged if you can show |

|||

extension of time to file your federal and New York State |

|

|

|

▼ Detach (cut) here▼ |

Do not submit with your return. |

|

|

Department of Taxation and Finance |

|

Application for Automatic |

Paid preparer? Mark an X in the box and complete the back.............

Your full Social Security number (SSN) |

Spouse’s full SSN (only if filing a joint return) |

||

|

|

|

|

Your first name and middle initial |

Your last name |

|

|

|

|

|

|

Spouse’s first name and middle initial |

Spouse’s last name |

||

|

|

|

|

Mailing address (number and street or PO box) |

|

|

Apartment number |

|

|

|

|

City, village, or post office (see instructions) |

|

State |

ZIP code |

|

|

|

|

Email: |

|

|

|

|

|

|

|

Enter your 2‑character special condition code

if applicable (see instructions) .................................

Mark an X in the box for each tax that you are subject to:

NYS tax |

NYC tax |

Yonkers tax |

MCTMT |

|

|

|

|

Dollars |

|

1 |

.....Sales and use tax |

|

|

|

2 |

Total payment |

|

|

|

|

|

|||

Cents

00

00

3701200094

Page 2 of 3

reasonable cause for paying late. This penalty is in addition to the interest charged for late payments.

Reasonable cause will be presumed with respect to the addition to tax for late payment of tax if the requirements relating to extensions of time to file have been complied with, the balance due shown on the income tax return, reduced by any sales or use tax that is owed, is no greater than 10% of the total New York State, New York City, and Yonkers tax, and metropolitan commuter transportation mobility tax (MCTMT) shown on the income tax return, and the balance due shown on the income tax return is paid with the return.

Late filing penalty – If you do not file your Form

Interest

Interest will be charged on income tax, MCTMT, or sales or use tax that is not paid on or before the due date of your return, even if you received an extension of time to file your return. Interest is a charge for the use of money and in most cases may not be waived. Interest is compounded daily and the rate is adjusted quarterly.

Fee for payments returned by banks

The law allows the Tax Department to charge a $50 fee when a check, money order, or electronic payment is returned by a bank for nonpayment. However, if an electronic payment is returned as a result of an error by the bank or the department, the department won’t charge the fee. If your payment is returned, we will send a separate bill for $50 for each return or other tax document associated with the returned payment.

Specific instructions

Married taxpayers who:

•file separate returns must complete separate Forms

Form

•file a joint Form

•file a Form

Spouse’s Certification, do not list the spouse with no New York source income on Form

Name and address box – Enter your name (both names if filing a joint application), address, and entire Social Security number(s). Failure to provide the entire Social Security number may invalidate this extension or result in monies not being properly credited to your account. If you do not have a Social Security number, enter do not have one. If you do not have a Social Security number, but have applied for one, enter applied for.

Foreign addresses – Enter the information in the following order: city, province or state, and then country (all in the City, village, or post office box). Follow the country’s practice for entering the postal code. Do not abbreviate the country name.

Special condition codes – If you are out of the country and need an additional four months to file (October 15, 2021), enter special condition code E3. If you are a nonresident alien and your filing due date is June 15, 2021, and you need an additional six months to file (December 15, 2021), enter special condition code E4. If you qualified for a

a nonresident alien, on or before December 15, 2021), enter special condition code D9. Also enter the applicable special condition code, E3, E4, or D9 on Form

Privacy notification

See our website or Publication 54, Privacy Notification.

▼Detach (cut) here▼ Do not submit with your return.

When completing this section, enter your New York tax preparer registration |

|

Payment options – Full payment must be made by check or money order of |

identification number (NYTPRIN) if you are required to have one. If you are |

any balance due with this automatic extension of time to file. Make the check |

not required to have a NYTPRIN, enter in the NYTPRIN excl. code box one |

or money order payable in U.S. funds to New York State Income Tax and |

of the specified |

write the last four digits of your Social Security number and 2020 Income Tax |

from the registration requirement. You must enter a NYTPRIN or an exclusion |

on it. For online payment options, see our website (at www.tax.ny.gov). |

code. Also, you must enter your federal preparer tax identification number |

|

(PTIN) if you have one; if not, you must enter your Social Security number. |

Paid preparers – Under the law, all paid preparers must sign and complete |

|

|

|

|

|

||||||

the paid preparer section of the form. Paid preparers may be subject to civil |

|

Code |

Exemption type |

Code |

Exemption type |

||||||

and/or criminal sanctions if they fail to complete this section in full. |

|

01 |

Attorney |

02 |

Employee of attorney |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

03 |

CPA |

04 |

Employee of CPA |

|

▼ Paid preparer must complete (see instructions) ▼ |

Date: |

||||||||||

|

|

|

|

|

|||||||

|

05 |

PA (Public Accountant) |

06 |

Employee of PA |

|||||||

Preparer’s signature |

▼ Preparer’s NYTPRIN |

|

|||||||||

▼ |

|

|

|

|

|

|

07 |

Enrolled agent |

08 |

Employee of enrolled |

|

|

|

|

|

|

|

|

|||||

Firm’s name (or yours, if |

▼ Preparer’s PTIN or SSN |

|

|

|

|

|

agent |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

09 |

Volunteer tax preparer |

10 |

Employee of business |

|

Address |

Employer identification number |

|

|

|

|

preparing that |

|||||

|

|

|

|

|

|

|

|

|

|

business’ return |

|

|

|

NYTPRIN |

|

See our website for more information about the tax preparer |

|||||||

|

|

excl. code |

|

|

|

|

|||||

|

|

|

|

|

registration requirements. |

|

|

||||

Email: |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||

3702200094

Worksheet instructions

Complete the following worksheet to determine if you must make a payment with Form

If you enter an amount on lines 1, 2, 3, or 4 of this worksheet, mark an X in the appropriate box on the front of this form.

Line 1 – Enter the amount of your New York State income tax liability for 2020 that you expect to enter on Form

Line 2 – Enter the amount of your New York City income tax liability for 2020 that you expect to enter on Form

Line 3 – Enter the amount of your Yonkers income tax liability for 2020 that you expect to enter on Form IT‑201, lines 55, 56, and 57; or Form IT‑203, lines 53 and 54.

Line 4 – Enter the amount of your MCTMT liability for 2020 that you expect to enter on Form

Line 5 – Enter the amount of sales and use tax, if any, that you will be required to report when you file your 2020 return. See the instructions for your NYS income tax return for information on how to compute your sales and use tax. Also enter this amount on line 1 on the front of this form.

Line 7 – Enter the amount of 2020 tax already paid that you expect to enter on Form

|

|

Worksheet |

|

|

|

|

1 |

|

|

1. |

|

|

|

New York State income tax liability for 2020 . |

|

|

||||

2 |

....New York City income tax liability for 2020 |

|

|

|||

3 |

...........Yonkers income tax liability for 2020 |

|

|

|||

4 |

MCTMT liability for 2020 |

4. |

|

|

||

5Sales and use tax due for 2020 (enter this

|

amount here and on line 1 on the front) |

5. |

|

|

6 |

Total taxes (add lines 1 through 5) |

6. |

||

7 |

Total 2020 tax already paid |

7. |

||

8 |

Total payment (subtract line 7 from line 6 and enter this |

|||

|

amount here and on line 2 on the front). If line 7 is more |

|||

|

than line 6, enter 0 |

8. |

||

Note: You may be subject to penalties if you underestimate the balance due.

How to claim credit for payment made with this form

Include the amount paid with Form

For more information, see the line instructions for the return you file.

Where to file

If you are enclosing a payment with Form

EXTENSION REQUEST

PO BOX 4125

BINGHAMTON NY

If you are not enclosing a payment with Form

EXTENSION

PO BOX 4126

BINGHAMTON NY

Private delivery services

If you choose, you may use a private delivery service, instead of the U.S. Postal Service, to mail in your form and tax payment. However, if, at a later date, you need to establish the date you filed or paid your tax, you cannot use the date recorded by a private delivery service unless you used a delivery service that has been designated by the U.S. Secretary of the Treasury

or the Commissioner of Taxation and Finance. (Currently designated delivery services are listed in Publication 55, Designated Private Delivery Services. See Need help? below for information on obtaining forms and publications.) If you have used a designated private delivery service and need to establish the date you filed your form, contact that private delivery service for instructions on how to obtain written proof of the date your form was given to the delivery service for delivery. See Publication 55 for where to send the form covered by these instructions.

Need help?

Visit our website at www.tax.ny.gov

• get information and manage your taxes online

• check for new online services and features

Telephone assistance |

|

Automated income tax refund status: |

|

Personal Income Tax Information Center: |

|

To order forms and publications: |

|

Text Telephone (TTY) or TDD |

Dial |

equipment users |

New York Relay Service |

|

|

3703200094

File Overview

| Fact Name | Description |

|---|---|

| Purpose and Usage | The NY IT-370 form is used to request an automatic six-month extension of time to file the NY State income tax returns (IT-201 or IT-203) for individuals. |

| Filing Deadline | Must be filed on or before the due date of the original tax return. For calendar year filers, this is typically April 15. |

| Payment with Submission | When filing Form IT-370, any estimated tax due must be paid to obtain the extension, using the included worksheet to calculate the payment. |

| Governing Laws | The form and its requirements are governed by New York State Tax Law and the instructions provided by the Department of Taxation and Finance. |

Ny It 370: Usage Guidelines

Filing the New York IT-370 form is essential for individuals who need more time to compile their New York State income tax return documents. This form grants an automatic six-month extension to file, ensuring no penalties for late submission as long as the form and any owed payments are submitted by the original due date. The steps below will guide you through filling out this form accurately. Following these details carefully is pivotal to ensuring that the process goes smoothly and effectively.

- Fill in your full Social Security number and, if filing jointly, your spouse’s full Social Security number.

- Enter your first name, middle initial, and last name. If filing jointly, also provide your spouse’s name and middle initial.

- Enter your mailing address, including the number and street or P.O. box, apartment number, city, village, or post office, state, and ZIP code.

- Indicate your email address if you have one.

- If applicable, enter your 2-character special condition code.

- Mark an X in the box for each applicable tax: NYS tax, NYC tax, Yonkers tax, and MCTMT (metropolitan commuter transportation mobility tax).

- Determine the total payment due, if any, and fill in lines for sales and use tax and the total payment in dollars and cents.

- For those required, enter the New York tax preparer registration identification number or PTIN if a paid preparer is completing the form.

- Complete the worksheet on page 3 of the form to determine if a payment is required with your extension request, and calculate the total payment amount needed.

- Sign and date the form. If a paid preparer filled out the form, ensure they complete the paid preparer section.

- Review the form for accuracy and completeness.

- Mail the completed IT-370 form by the due date for your return:

- If including a payment, send to: EXTENSION REQUEST PO BOX 4125, BINGHAMTON NY 13902-4125

- Without a payment, send to: EXTENSION REQUEST–NR, PO BOX 4126, BINGHAMTON NY 13902-4126

Remember, it is critical to submit Form IT-370 by your original filing deadline to avoid potential penalties for late submission of your income tax return. Making any required payment alongside this form by the due date will also help in avoiding late payment penalties and interest charges. Taking these steps ensures you remain compliant with New York State tax obligations while giving you more time to file your complete and accurate income tax return.

FAQ

What is Form IT-370 and why would I need to file it?

Form IT-370, the Application for Automatic Six-Month Extension of Time to File for Individuals, is utilized when more time is needed to file the New York State income tax returns, specifically Form IT-201, Resident Income Tax Return, or Form IT-203, Nonresident and Part-Year Resident Income Tax Return. This request grants an automatic six-month extension to submit the necessary returns, providing additional time without the need for a federal extension form.

When is the deadline to file Form IT-370?

The form must be filed on or before the original due date of your return. Generally, this is April 15th for calendar-year filers. If special circumstances apply, such as being out of the country or a U.S. nonresident alien, the deadlines adjust accordingly to June 15th or other specified dates. Filing beyond your return's due date invalidates the extension application.

Can I file Form IT-370 electronically?

Yes, you may file Form IT-370 electronically if you meet the conditions for electronic filing as detailed in the instructions for forms IT-201 and IT-203. This option allows for a more convenient submission process.

What payment is required with Form IT-370?

To obtain the extension, full payment of the estimated tax due is necessary. Payment can be made by check or money order, with guidance on the calculation provided in the form's worksheet. This includes any New York State, New York City, and Yonkers tax, as well as metropolitan commuter transportation mobility tax (MCTMT) and sales or use tax.

What penalties might I face if I don't comply with payment or filing requirements?

If tax is not paid by the due date, a late payment penalty of ½ of 1% of the unpaid amount per month, up to 25%, may apply. Additionally, failing to file the return or Form IT-370 by the due date invites a late filing penalty of 5% of the tax due per month, up to 25%. However, these penalties may be waived if reasonable cause is demonstrated.

If I am married, how should my spouse and I file Form IT-370?

Married taxpayers have options based on their filing status. If filing separate returns, each spouse must submit a separate Form IT-370. For a joint extension, the form is filed collectively, with any payment equally divided between each spouse's accounts. However, if a Form IT-203-C is also filed due to one spouse having no New York source income, do not list them on the Form IT-370 to ensure proper account allocation.

What if I am a nonresident or have special filing circumstances?

If you are a nonresident alien, outside the United States and Puerto Rico, or claiming nonresident status under specific tax law provisions, you may qualify for extensions beyond six months. Special condition codes (e.g., E3, E4, D9) must be entered on Form IT-370 and the respective income tax return to denote these statuses.

Common mistakes

Filling out tax forms can be a daunting task, and the New York IT-370 form is no exception. This form, used to apply for an automatic six-month extension of time to file certain New York State income tax returns, often trips up filers. Let's explore seven common mistakes made when completing this form:

- Missing the filing deadline - Submission of Form IT-370 is required on or before the original due date of your return to secure an extension. Missing this deadline could lead to penalties for failing to file on time.

- Incorrect payment estimate - The form necessitates an accurate estimate of any tax due. Underestimating the amount owed could result in penalties and interest charges on the unpaid balance.

- Not including payment for estimated tax due - If you owe taxes, payment should accompany your extension request. Failure to include the estimated tax payment can also lead to penalties and interest.

- Providing incomplete or incorrect information - It's crucial to fill in every required field accurately, especially your Social Security number(s) and address. Mistakes here can invalidate your extension or delay processing.

- Overlooking special condition codes - If you qualify for additional extensions due to specific circumstances (like being out of the country), failing to include the correct special condition code may cost you the extra time.

- Not signing the form - An unsigned form is like an unsubmitted form in the eyes of taxation authorities. Ensure you (and your spouse, if filing jointly) sign the form before submission.

- Failing to file electronically where applicable - Although the IT-370 allows for electronic filing, some filers still submit paper forms when they could benefit from the convenience and reduced processing time of e-filing.

Errors on the IT-370 can lead to a variety of complications, from simple delays to financial penalties. It's important to pay careful attention to each part of the form, to ensure that all the information is complete and correct. Furthermore, understanding the specific instructions and requirements can help avoid these mistakes. For instance, when making a payment, checks or money orders should be payable in U.S. funds to the New York State Income Tax and should include the last four digits of your Social Security number to prevent misapplication of funds.

Avoiding these common pitfalls can help ensure that your extension is processed smoothly, giving you the extra time you need without unnecessary stress or cost. Remember, the extension only applies to the filing of the return, not to any tax payment due, so it's wise to estimate and submit any owed taxes with your Form IT-370 to avoid interest and penalties. Careful reading of the instructions provided with the form can guide you in completing it correctly. If in doubt, consulting with a tax professional or the Department of Taxation and Finance directly can provide clarity and peace of mind.

Documents used along the form

Filing tax forms and related documents is a multifaceted process, especially for individuals residing or earning income in the state of New York. When submitting the New York Form IT-370 for an automatic six-month extension of time to file personal income tax returns, there are additional forms and documents that taxpayers often need to consider. Below is a breakdown of some of these forms and documents, aiming to provide clarity on their purpose and necessity.

- Form IT-201: Resident Income Tax Return. This form is used by residents of New York State to file their annual income tax returns. It's essential for those who have their primary home in New York for more than half the year.

- Form IT-203: Nonresident and Part-Year Resident Income Tax Return. For individuals who lived in New York for only part of the year or earned income in the state without residing there, this form ensures their income is correctly taxed by New York State.

- Form IT-203-B: Nonresident and Part-Year Resident Income Allocation and College Tuition Itemized Deduction Worksheet. This helps nonresidents and part-year residents calculate how much of their income is subject to New York State taxes.

- Form Y-203: Yonkers Nonresident Earnings Tax Return. Individuals working in Yonkers but not residing there use this form to declare income earned within this jurisdiction, fulfilling local tax obligations.

- Form IT-201-ATT: Other Tax Credits and Taxes. This attachment is used alongside Form IT-201 for detailing applicable tax credits and additional taxes owed by the taxpayer.

- Form IT-2: Summary of W-2 Statements. Taxpayers must complete this form if they receive a W-2 form from their employer, summarizing their annual wages and tax withholdings.

- Form IT-1099-R: Summary of Federal Form 1099-R Statements. This form is necessary for individuals who have received distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, or insurance contracts, summarizing the information for state tax purposes.

- Form IT-214: Claim for Real Property Tax Credit for Homeowners and Renters. Eligible New York residents can claim a tax credit for real property taxes or rent paid during the tax year using this form.

Understanding these forms and when they are required is crucial for a smooth and accurate tax filing process. By familiarizing themselves with the specific documents related to their residency status and income sources, taxpayers can ensure compliance with New York State's taxation regulations and avoid common pitfalls during the tax season.

Similar forms

The IRS Form 4868, "Application for Automatic Extension of Time To File U.S. Individual Income Tax Return," bears resemblance to the NY IT-370 form, as both serve the purpose of requesting an additional six-month period to file their respective tax returns. While Form 4868 pertains to federal income tax returns, the NY IT-370 is specific to New York State taxpayers. Both forms must be filed by the original due date of the return to be valid and require an estimation of the tax due, if any, along with payment of any estimated amount owed to avoid penalties and interest.

Form 7004, "Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns," is akin to the IT-370 in its function of requesting extra time for tax filing. However, Form 7004 is targeted at businesses needing more time to file their federal tax returns, including partnerships, corporations, and certain trusts. Similar to the IT-370, Form 7004 requires submission by the tax return's original due date, but it covers a variety of business entities rather than individuals.

The California Form 3519, "Payment for Automatic Extension for Individuals," functions similarly to the NY IT-370, providing individuals an extension to file their state income tax return. Like the IT-370, this form is designed for taxpayers who cannot file their return by the original deadline and need additional time. Both forms entail estimating the amount of tax owed and making a payment by the original due date to avoid penalties.

The "Application for Extension of Time to File Michigan Tax Returns" (Form 4) offers Michigan taxpayers a parallel service to what the NY IT-370 provides for New Yorkers. It grants an automatic extension of time to file the state's income tax return. Although specific to Michigan residents, it similarly requires that the application be filed by the original due date of the return, mirroring the IT-370’s stipulations for extensions and payment of estimated tax due.

Form 8809, "Application for Extension of Time to File Information Returns," while serving a different target audience—businesses and other entities required to file information returns—shares the fundamental concept of requesting additional time for filing with the IT-370. This form is useful for entities that need more time to gather necessary information to accurately complete returns such as Forms W-2 or 1099. The parallel lies in the mechanism of providing relief through extended deadlines, albeit for different categories of filers.

Form IT-303, the "Application for Extension of Time to File Georgia Income Tax Return," parallels the NY IT-370 for Georgia residents. It allows individuals extra time to file their Georgia state income tax returns, requiring it to be filed by the return's original due date. Both forms facilitate an extension process specific to their respective state tax obligations, emphasizing the need for timely application and payment of estimated taxes due to avoid penalties.

New Jersey's Form NJ-630, "Application for Extension of Time to File New Jersey Gross Income Tax Return," serves a similar purpose for New Jersey residents as the NY IT-370 does for New York taxpayers. It allows individuals to request more time to file their state tax returns, conditional on filing by the original due date. Each form caters to the specific procedural and regulatory framework of its state, offering a structured process for securing an extension.

Form CT-1040 EXT, "Application for Extension of Time to File Connecticut Income Tax Return for Individuals," offers Connecticut taxpayers a mechanism like the NY IT-370, granting an extension for filing their state income tax returns. To avoid penalties, filers must estimate and pay any tax due by the original filing deadline. Both forms represent state-specific adaptations of the federal extension request process, tailored to the administrative requirements of individual states.

Form RPD-41096, "Application for Extension of Time to File New Mexico Personal Income Tax Return," is another state-specific document providing an extension service similar to that of the NY IT-370, but for New Mexico residents. It allows taxpayers additional time to file their personal income tax returns, emphasizing the need for submission by the statutory due date and payment of any estimated taxes to avoid interest and penalties.

Dos and Don'ts

When completing the NY IT-370 form, there are essential practices to follow and avoid ensuring a smooth process. Adhering to these guidelines can make the difference between a successfully filed request for an extension and unnecessary complications.

Do:- File on time: Submit Form IT-370 on or before your return's due date to receive an automatic six-month extension.

- Include payment for any tax due: Alongside Form IT-370, provide full payment of the estimated tax balance due to avoid penalties and interest charges.

- Review specific instructions: Carefully read through the specific instructions for married taxpayers, payment options, and other relevant sections to ensure accurate completion.

- Ensure correct mailing: Depending on whether you are including a payment, mail your Form IT-370 to the correct address to prevent delays or misplacement.

- Overlook the deadline: Failing to file by the due date can invalidate your extension request and lead to penalties.

- Miscalculate your estimated tax due: Incorrectly estimating the amount of tax owed can result in penalties, so use the worksheet provided carefully.

- Ignore special condition codes: If applicable, use the correct special condition code related to your filing circumstances for accurate processing.

- Forget to sign: A common oversight is failing to sign the form. Ensure that both you and, if applicable, your paid preparer sign the form before submission.

Misconceptions

One common misconception is that the NY IT-370 form can be substituted with a copy of the federal extension form. This is not the case; the State of New York explicitly requires Form IT-370 for an extension and does not accept a federal extension form as a replacement.

Many people mistakenly believe that filing Form IT-370 grants an extension on paying taxes due. However, it only extends the time to file the income tax return. Taxes owed are still due by the original deadline, and failure to pay on time can result in penalties and interest.

Another misconception is that the extension provided by Form IT-370 is beyond six months. In truth, Form IT-370 only grants an automatic six-month extension, with specific conditions under which further extension might be possible for those living outside the United States or for nonresident status claims.

Some individuals think that if they file for an extension, they do not have to estimate and pay any tax due with the form. Actually, to avoid penalties, an estimated tax payment should accompany the extension form if you believe you owe taxes.

There's also a wrong notion that Form IT-370 extends the time to pay any sales or use tax due. This extension form is specifically for income tax returns, and any sales or use tax due must be handled separately according to its own deadlines and requirements.

Many assume that an extension to file using Form IT-370 also extends the deadline for filing Form Y-203, Yonkers Nonresident Earnings Tax Return. While the extension for filing the state return does automatically extend the time for filing Form Y-203, it's important to understand the particular requirements and deadlines for this form.

Lastly, a significant misconception is that extensions are automatically granted without the need to file Form IT-370. In fact, to receive the six-month extension, a completed IT-370 form must be submitted by the original due date of the return.

Key takeaways

When dealing with the New York State IT-370 form, an Application for Automatic Six-Month Extension of Time to File for Individuals, there are several key points to remember:

- Filing the IT-370 form by the due date of your return grants an automatic six-month extension to file Form IT-201 (Resident Income Tax Return) or Form IT-203 (Nonresident and Part-Year Resident Income Tax Return).

- Replacing Form IT-370 with a federal extension form is no longer accepted by the New York State Department of Taxation and Finance.

- Form IT-370 must be filed on or before the original due date of your return to be valid.

- A payment for the estimated tax due should accompany your IT-370 form to avoid late payment penalties. Use the worksheet provided in the form instructions to calculate the payment if necessary.

- If filing electronically, conditions for electronic submission must be met as outlined in the instructions for Forms IT-201 and IT-203.

- Filing Form IT-370 automatically extends the time to file Form Y-203 (Yonkers Nonresident Earnings Tax Return).

- The extension of time to file beyond six months is not typically granted to residents within the United States, except under specific circumstances such as living outside the United States and Puerto Rico.

- Married taxpayers must each file separate IT-370 forms if they file separate income tax returns. Joint filers will have any payments divided equally and credited to both accounts.

- Late payment penalties and interest will apply to unpaid or underpaid tax amounts by the due date, even with an extension.

- Nonpayment by banks for reasons such as insufficient funds will incur a $50 fee, separate from other penalties and interest for late payment.

Ensuring the correct and timely filing of Form IT-370, along with the full payment of estimated taxes due, is crucial to avoid unnecessary penalties and interest. It's also important to understand the specific conditions under which one can qualify for an extension, and what the extension covers in terms of tax obligations with the state of New York.

Common PDF Documents

Ga-4 Form - By including both payroll and loss cost data, the GA-4 form allows for a comprehensive calculation of the total assessment due.

Irc 125 on W2 - Guides corporations on how to appoint their tax payment—either as a refund or credit towards the next year's estimated tax.

New York Prs 2 - A prerequisite for teachers to verify and officially claim prior service credit within their retirement system benefits.