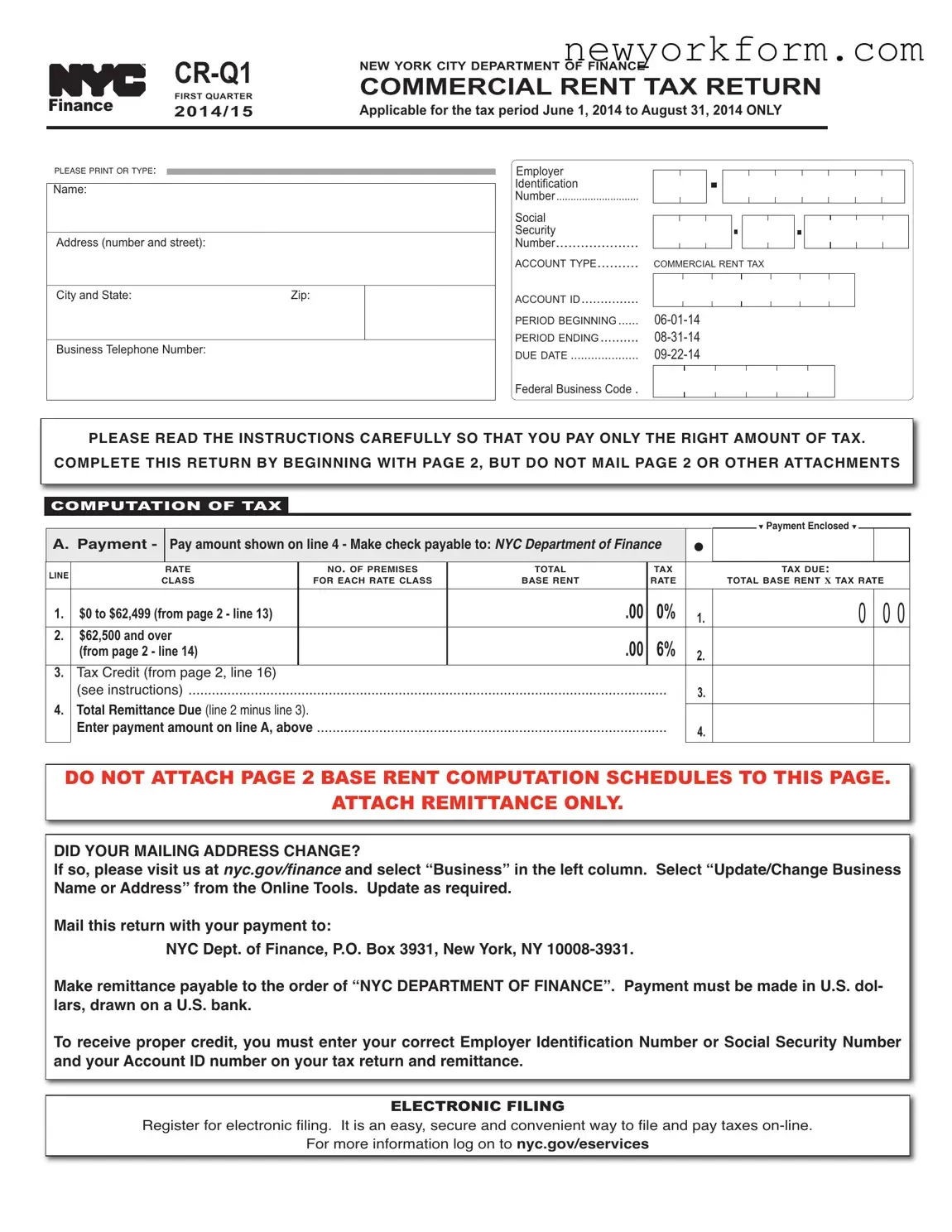

Free Ny Commercial Rent Tax Form in PDF

Navigating through the intricacies of the New York City Department of Finance's Commercial Rent Tax (CRT) can be a daunting task for businesses operating within the bustling metropolis. The CR-Q1 form, specifically designed for the tax period of June 1, 2014, to August 31, 2014, stands as the initial quarter return document that these entities must tackle. It calls for a detailed account of rented premises, alongside the employer or individual identification numbers, to ensure a comprehensive understanding of the tax obligations based on rented spaces. Moreover, the form guides taxpayers through the computation of tax, applying rates and credits where designated, to determine the total tax liability or refund due. Intricate aspects such as deductions for commercial revitalization program participation and other permissible subtractions from the gross rent are highlighted to aid businesses in minimizing their tax expenditure. Furthermore, instructions embedded within the form steer taxpayers towards correct electronic or physical submission protocols and stress the importance of accuracy in reporting, underscored by the potential disqualification of deductions for erroneous information. In essence, the CR-Q1 form encapsulates a critical compliance avenue for businesses within New York City, embedding layers of fiscal responsibilities, calculation methodologies, and payment directives within its structure.

Ny Commercial Rent Tax Sample

|

NEW YORK CITY DEPARTMENT OF FINANCE |

||

|

|

||

FINANCE |

FIRST QUARTER |

COMMERCIAL RENT TAX RETURN |

|

2014/15 |

ApplicableforthetaxperiodJune1,2014toAugust31,2014ONLY |

||

|

|||

|

|

|

PLEASE PRINT OR TYPE:

Name:

_________________________________________________________________________________

Address (number and street):

_________________________________________________________________________________

City and State: |

Zip: |

_________________________________________________________________________________ |

|

Business Telephone Number: |

|

Employer

Identification

Number .............................

Social

Security

Number....................

ACCOUNT TYPE |

COMMERCIAL RENT TAX |

|

|

|

|

|||

ACCOUNT ID |

|

|

|

|

|

|

|

|

PERIOD BEGINNING |

|

|

|

|

|

|

||

PERIOD ENDING |

|

|

|

|

|

|

||

DUE DATE |

|

|

|

|

|

|

||

Federal Business Code .

PLEASE READ THE INSTRUCTIONS CAREFULLY SO THAT YOU PAY ONLY THE RIGHT AMOUNT OF TAX. COMPLETE THIS RETURN BY BEGINNING WITH PAGE 2, BUT DO NOT MAIL PAGE 2 OR OTHER ATTACHMENTS

COMPUTATION OF TAX

|

|

|

|

|

|

|

|

|

|

▼ Payment Enclosed ▼ |

|

|

|

A. Payment - |

Payamountshown online4- Makecheck payableto:NYCDepartmentofFinance |

● |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LINE |

|

RATE |

|

NO. OF PREMISES |

TOTAL |

TAX |

|

|

TAX DUE: |

||

|

CLASS |

|

FOR EACH RATE CLASS |

BASE RENT |

RATE |

|

TOTAL BASE RENT X TAX RATE |

|||||

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

$0 to $62,499 (from page 2 - line 13) |

|

|

.00 |

0% |

1. |

0 |

0 0 |

|||

|

2. |

$62,500 and over |

|

|

.00 |

6% |

|

|

|

|

|

|

|

|

(from page 2 - line 14) |

|

|

2. |

|

|

|

|

|||

|

3. |

Tax Credit (from page 2, line 16) |

|

|

|

|

|

|

|

|

||

|

|

(see instructions) |

|

|

3. |

|

|

|

|

|||

|

4. |

TotalRemittanceDue(line 2 minus line 3). |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||||

|

|

Enter paymentamounton lineA,above |

.......................................................................................... |

|

|

4. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DO NOT ATTACH PAGE 2 BASE RENT COMPUTATION SCHEDULES TO THIS PAGE.

ATTACH REMITTANCE ONLY.

DID YOUR MAILINGADDRESS CHANGE?

If so, please visit us at nyc.gov/financeand select “Business” in the left column. Select “Update/Change Business

Name orAddress” from the Online Tools. Update as required.

Mail this return with your payment to:

NYC Dept. of Finance, P.O. Box 3931, New York, NY

Make remittance payable to the order of “NYC DEPARTMENT OF FINANCE”. Payment must be made in U.S. dol- lars, drawn on a U.S. bank.

To receive proper credit, you must enter your correct Employer Identification Number or Social Security Number and yourAccount ID number on your tax return and remittance.

ELECTRONIC FILING

Register for electronic filing. It is an easy, secure and convenient way to file and pay taxes

For more information log on to nyc.gov/eservices

Form |

Page 2 |

USE THIS

PAGE IF

PAGE IF YOU HAVE

YOU HAVE

THREE

THREE

OR LESS

OR LESS

PREMISES/SUBTENANTS OR, MAKE COPIES OF THIS

PREMISES/SUBTENANTS OR, MAKE COPIES OF THIS

PAGE TO REPORT ADDITIONAL PREMISES/SUBTENANTS. IF YOU REPORT MORE THAN

PAGE TO REPORT ADDITIONAL PREMISES/SUBTENANTS. IF YOU REPORT MORE THAN

THREE

THREE

PREMISES OR SUBTENANTS, AND CHOOSE TO

PREMISES OR SUBTENANTS, AND CHOOSE TO

USE A SPREADSHEET, YOU MUST USE THE

USE A SPREADSHEET, YOU MUST USE THE

CRQ FINANCE

CRQ FINANCE

SUP- PLEMENTAL SPREADSHEET, WHICH YOU CAN DOWNLOAD FROM

SUP- PLEMENTAL SPREADSHEET, WHICH YOU CAN DOWNLOAD FROM

OUR WEBSITE AT WWW.NYC.GOV/CRTINFO.

OUR WEBSITE AT WWW.NYC.GOV/CRTINFO.

EACH LINE MUST BEACCURATELYCOMPLETED. YOUR DEDUCTION WILLBE DISALLOWED IF INACCURATE INFORMATION IS SUBMITTED.

LINE |

DESCRIPTION |

PREMISES 1 |

PREMISES 2 |

PREMISES 3 |

||||

● 1a. |

Street Address ......................................................... 1a. |

|

|

|

|

|

|

|

1b. Zip Code ..................................................................1b. |

________________________________________________________________________________________ |

|||||||

1c. |

Block and 1d. Lot Number...................................1c/1d. ________________________________________________________________________________________ |

|||||||

|

|

|

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

● 2. |

Gross Rent Paid (see instructions) |

2. |

________________________________________________________________________________________ |

3. |

Rent Applied to Residential Use |

3. |

________________________________________________________________________________________ |

|

............................................. |

4a. |

________________________________________________________________________________________ |

●4b. Employer Identification Number (EIN) forKEEP THIS PAGE partnerships or corporations .....................................4b. ● 4b. EIN _____________________ ● 4b. EIN_____________________ ● 4b. EIN ____________________4a. SUBTENANT'S NAME

4c. Social Security Number for individuals |

4c. |

● 4c. SSN_____________________ ● 4c. SSN ____________________ ● 4c. SSN ____________________ |

|

4d. RENT RECEIVED FROM SUBTENANT |

|

|

|

|

(see instructions if more than one subtenant) |

4d. ___________________________________________________________________________________________________ |

|

5b. |

Commercial RevitalizationFORProgram |

YOUR RECORDS. |

|

5a. |

Other Deductions (attach schedule) |

5a. |

________________________________________________________________________________________ |

|

special reduction (see instructions) |

5b. |

________________________________________________________________________________________ |

6. |

Total Deductions (add lines 3, 4d, 5a and 5b) |

6. |

________________________________________________________________________________________ |

7.Base Rent Before Rent Reduction (line 2 minus line 6) ....7DO. ________________________________________________________________________________________NOT FILE

8.35% Rent Reduction (35% X line 7) ...........................8. ________________________________________________________________________________________

9. Base Rent Subject to Tax (line 7 minus line 8) ...........9. ________________________________________________________________________________________

If the line 7 amount represents rent for less than the full 3 month period, proceed to line 10a, or

NOTE If the line 7 amount plus the line 5b amount is $62,499 or less and represents rent for a full 3 month period, transfer line 9 to line 13, or If the line 7 amount plus the line 5b amount is $62,500 or more and represents rent for a full 3 month period, transfer line 9 to line 14

COMPLETE LINES 10 - 12 ONLY IF YOU RENTED PREMISES FOR LESS THAN THE FULL

........10a. Number of Months at Premises during the tax period |

10a. # of months |

10b. From: |

10a. # of months |

10b. From: |

10a. # of months |

10b. From: |

|

|

|

10c. To: |

|

10c. To: |

|

|

10c. To: |

11.Monthly Base Rent before rent reduction

(line 7 plus line 5b divided by line 10a) |

11. ________________________________________________________________________________________ |

12.Quarterly Base Rent before rent reduction

(line 11 X 3 months) |

12. ________________________________________________________________________________________ |

■If the line 12 amount is $62,499 or less, transfer the line 9 amount (NOT THE LINE 12AMOUNT) to line 13

■If the line 12 amount is $62,500 or more, transfer the line 9 amount (NOT THE LINE 12AMOUNT) to line 14

|

RATE CLASS |

TAX RATE |

|

|

|

13. |

($0 - 62,499) |

0% |

13. |

_______________________________________________________________________________________ |

|

14. |

($62,500 or more) |

6% |

14. |

_______________________________________________________________________________________ |

|

15.Tax Due before credit

(line 14 multiplied by 6%) |

15. |

|

16. Tax Credit (see worksheet below) |

16. |

_______________________________________________________________________________________ |

Note: The tax credit only applies if line 7 plus line 5b (or line 12, if applicable) is at least $62,500, but is less than $75,000. All others enter zero.

Tax Credit Computation Worksheet

■If the line 7 amount represents rent for the full 3 month period, your credit is calculated as follows:

Amount on line 15 X ($75,000 minus the sum of lines 7 and 5b) = _____________ = your credit

$12,500

■If the line 7 amount represents rent for less than the full 3 month period, your credit is calculated as follows:

Amount on line 15 X ($75,000$12,500minus line 12) = _____________ = your credit

TRANSFER THE AMOUNTS FROM LINES 13, 14 AND 16 TO THE CORRESPONDING LINES ON PAGE 1

File Overview

| Fact | Detail |

|---|---|

| Form Title | CR-Q1 New York City Department of Finance Finance First Quarter Commercial Rent Tax Return 2014/15 |

| Applicable Period | For the tax period from June 1, 2014, to August 31, 2014, ONLY |

| Submission Detail | Do not mail Page 2 or other attachments; attach remittance only. Instructions for the payment are detailed, including making the check payable to the NYC Department of Finance. |

| Governing Law | New York City Administrative Code governs Commercial Rent Tax (CRT) in New York City. |

| Electronic Filing | Encourages filers to register for electronic filing as an easy, secure, and convenient way to file and pay taxes online. |

Ny Commercial Rent Tax: Usage Guidelines

The New York City Department of Finance requires commercial entities operating within its jurisdiction to file a Commercial Rent Tax (CRT) return on a quarterly basis. This requirement specifically concerns businesses occupying premises where the annual rent exceeds a certain threshold. Keeping accurate records and understanding the detailed instructions for completing the CRT return is paramount to ensuring compliance and avoiding potential penalties. Below are instructions to guide you through filling out the New York Commercial Rent Tax form for the first quarter of the 2014/15 tax year.

- Begin with the top section by entering your business’s name, address (including number and street, city, state, and zip code), business telephone number, employer identification number (EIN), and social security number (if applicable).

- Proceed to fill in the ‘Account Type’, ‘Commercial Rent Tax Account ID’, ‘Period Beginning’, ‘Period Ending’, and ‘Due Date’ fields as already pre-filled for the specific tax period (June 1, 2014, to August 31, 2014).

- Under ‘Computation of Tax’, check the box if payment is enclosed and enter the amount on line A. Make your check payable to: NYC Department of Finance.

- Go to the ‘Computation of Tax’ section to complete information regarding the tax due:

- For line 1, enter the base rent for rate class $0 to $62,499, which is taxed at a 0% rate.

- For line 2, enter the base rent for the rate class over $62,500, which is subjected to a 6% tax rate.

- Enter any applicable tax credit in line 3, and subtract this from line 2 to calculate your total remittance due on line 4.

- Confirm your mailing address. If your mailing address has changed, the form prompts you to update your information online at the NYC Department of Finance website.

- Prepare your payment to be sent along with this form to the mailing address provided on the form. Ensure your EIN or Social Security Number and your Account ID number are included both on your tax return and on your remittance.

- Lastly, for electronic filing, which is encouraged for its convenience and security, the form provides instructions and the web address for registration.

FAQ

What is the New York City Commercial Rent Tax (CRT)?

The New York City Commercial Rent Tax is a tax imposed on the occupant of a property within certain areas of Manhattan for the privilege of occupying commercial premises. It applies to tenants who pay a total annual rent for any premises used for business purposes. This tax is calculated based on the rent paid under specific conditions and thresholds set by the New York City Department of Finance.

Who needs to file a Commercial Rent Tax return?

Any business or individual occupying commercial premises in Manhattan, south of the center line of 96th Street, must file a Commercial Rent Tax return if the annual gross rent paid exceeds a certain threshold. The requirement to file applies regardless of whether the business owns or leases the space.

What is the period covered by the CR-Q1 form?

The CR-Q1 form covers the first quarter of the Commercial Rent Tax year, specifically from June 1 to August 31. It is filed quarterly, and the due date for the first quarter form is on September 22.

How do I determine the tax amount due on the CR-Q1 form?

To determine the tax amount due, start by calculating the total base rent paid for the premises. Apply the tax rate to the base rent amount, which is 0% for rents up to $62,499 and 6% for amounts $62,500 and over. If applicable, subtract any tax credit from the gross tax due to find the total remittance due.

How can I claim a tax credit on the CR-Q1 form?

A tax credit can be claimed if the total base rent, plus any applicable additional amounts, falls within a specific range. The exact calculation depends on whether the rent amount represents the whole three-month period or a portion thereof. The tax credit computation worksheet provided on the form should be used to calculate the correct credit amount.

What should I do if my mailing address has changed?

If your mailing address has changed, it is essential to update your information with the NYC Department of Finance. This can be done by visiting the NYC.gov/finance website, selecting "Business" from the left column, and then choosing "Update/Change Business Name or Address" from the Online Tools section.

Is electronic filing available for the Commercial Rent Tax?

Yes, electronic filing is available and encouraged for filing and paying the Commercial Rent Tax. Registering for electronic filing offers a secure, convenient, and easy way to manage your taxes online. Information on how to register and file electronically can be found on the NYC.gov/eservices website.

What if I rent more than three premises or subtenants?

If you are reporting on more than three premises or subtenants, copies of the page for premises/subtenants can be made, or a supplemental spreadsheet provided by the NYC Department of Finance can be used. It's important to accurately complete each line for every premise or subtenant to ensure correct tax calculation and compliance.

Are there any deductions allowed when calculating the base rent?

Yes, certain deductions are allowed when calculating the base rent for the Commercial Rent Tax. These include rent applied to residential use, amounts received from subtenants, other deductions such as business expenses, and special reductions from programs like the Commercial Revitalization Program. Be sure to attach any schedules or documentation supporting these deductions.

What is the due date for the CR-Q1 Commercial Rent Tax return, and how should payment be made?

The CR-Q1 Commercial Rent Tax return is due on September 22 for the period covering June 1 to August 31. Payment should be made online when filing electronically, or by check payable to the "NYC DEPARTMENT OF FINANCE" when filing by mail. Include the correct Employer Identification Number (EIN) or Social Security Number (SSN), and CR-Q1 form Account ID number to ensure the payment is credited properly.

Common mistakes

When filling out the New York City Commercial Rent Tax (CRT) form, it's imperative to avoid common mistakes to ensure compliance and avoid potential penalties. The CRT, a tax on commercial rents within certain areas of Manhattan, requires careful attention to detail.

Incorrect Employer Identification Number (EIN) or Social Security Number (SSN): Ensuring the accuracy of identification numbers is crucial. The form distinguishes between these numbers for partnerships or corporations (line 4b) and individuals (line 4c). Mistakes here could lead to processing delays or misapplied payments.

Failing to Accurately Report Base Rent: The base rent must be meticulously calculated, considering gross rent paid (line 2) and adjustments for residential use (line 3) and deductions such as subtenant rent received (line 4d). Overlooking these details might result in erroneous tax amounts being due.

Omitting Tax Credits: Neglecting applicable tax credits (line 16) is another common oversight. Businesses that qualify for credits based on their rent and the special reduction for the Commercial Revitalization Program (line 5b) could pay more than necessary if these credits are not properly calculated and reported.

Misclassification of Rent Periods: When the rented premises are not utilized for the full tax period, specific adjustments are required (lines 10a-c). Incorrectly classifying the rental period can lead to a misunderstanding of the tax obligation due to either overstating or understating the rent subject to tax.

Not Updating Mailing Address: The CRT form requests confirmation of the mailing address (bottom of the form) and provides instructions for updates via the website. Failure to maintain current contact information can result in missed communications or notices from the Department of Finance.

Efficiency and precision in completing the CRT form are supported by adhering to these guidelines, thereby safeguarding against the common pitfalls associated with its submission. Information must be reviewed for accuracy, and all applicable sections completed to ensure that the submitted form reflects the true tax liability.

Documents used along the form

When dealing with the New York Commercial Rent Tax (CRT) form, businesses often interact with a variety of other documents. These are essential for ensuring compliance, accuracy, and leveraging potential benefits under the law. Here's a look at some of those commonly used documents and forms.

- Lease Agreement: This document outlines the terms and conditions of the rental agreement between the landlord and the tenant. It's crucial for determining the base rent, which is a key figure on the CRT form.

- Rent Receipts: Rent receipts provide proof of the rent paid, which helps in accurately filling out the CRT form. These are often required for verification purposes.

- Financial Statements: These documents include profit and loss statements and balance sheets. They're used to report and calculate the correct amount of rent tax.

- Federal Business Code Documentation: This helps in classifying the business for tax purposes and is often required when filling out various sections of the CRT form.

- Tax Credit Forms: If eligible for tax credits against the CRT, additional forms must be completed. These credits could be vital for reducing the total taxable amount.

- Commercial Revitalization Program Documentation: For businesses participating in this program, documents proving eligibility and calculations for special deductions are needed.

- Electronic Filing Credentials: Businesses are encouraged to file electronically. Information and credentials related to electronic filing systems are, therefore, important.

- Amended Tax Returns: If errors are found or adjustments are needed after a return is filed, amended returns should be prepared and submitted.

- Notice of Change in Business Information: In case of changes to business address or name, proper documentation must be submitted to update tax records.

Managing the Commercial Rent Tax can be elaborate, requiring various forms and documentation. Businesses should keep good records and understand what documents are required not only for compliance but also to take full advantage of any eligible tax benefits. Paying attention to detail can save time and money, helping to ensure that businesses only pay the amount of tax that is rightfully due.

Similar forms

The New York State Sales Tax Return is significantly similar to the New York City Commercial Rent Tax form, primarily in their function of calculating and remitting tax based on business transactions. Both forms require detailed business information, such as names and addresses, and specific financial transactions over a given period. They break down the tax computation into taxable amounts, applicable rates, and deductions or credits, leading to the total tax due. Both forms also emphasize timely submission and payment to the respective tax authority, underscoring the importance of accuracy and deadlines in tax compliance.

The New York State Corporate Tax Return shares parallels with the NYC Commercial Rent Tax form through its focus on documenting financial activities tied to tax liabilities. This form also collects granular details about the business, including identification numbers and financial figures, to calculate the owed tax. Both documents utilize schedules to assess different income or expenditure categories, apply tax rates accordingly, and allow for various deductions or credits. These documents epitomize the systematic approach to tax assessment based on specific financial metrics of an entity.

The Federal Income Tax Return, while broader in scope, analogously requires detailed financial reporting from businesses, comparable to the requirements of the NYC Commercial Rent Tax form. Both necessitate declaring income or revenue figures, applying relevant deductions or credits, and calculating the net tax payable to the tax authorities. Additionally, the importance of accuracy in reporting and the implications of deadlines are strongly mirrored in the adherence and caution advised through the instructions accompanying both forms.

Payroll Tax Returns, such as the Federal Form 941, align with the NYC Commercial Rent Tax form in the aspect of periodic tax reporting. Both documents serve as a means for businesses to report specific, recurring financial obligations related to their operations—rent in one case and payroll in another. They each require detailed business information, account for exemptions or special conditions, and culminate in a calculation of the tax or payment due for the period in question.

The Property Tax Statement closely resembles the NYC Commercial Rent Tax form by virtue of both being anchored in real estate valuation. However, the Property Tax Statement typically focuses on the assessed value of owned property as the basis for taxation, whereas the NYC Commercial Rent Tax form centers on commercial rental transactions. These documents collectively reflect the local governance’s reliance on real estate for revenue generation, each with its own subset of rules for deductions and tax rate applications.

Utility Tax Filings interact with the realm of public services and their usage by businesses, bearing similarities to the NYC Commercial Rent Tax form in terms of periodicity and specific financial reporting. These filings require businesses to report their consumption of utilities, applying rates to calculate taxes similar to how rent values are used to determine tax liability on the Commercial Rent Tax form. Both sets of documents underscore the businesses' responsibilities in contributing to public coffers based on consumption or usage metrics.

Excise Tax Forms, related to specific products or services, showcase a targeted approach to taxation, recalling the focused nature of the NYC Commercial Rent Tax form, which is dedicated to commercial rent. Although varying in the object of taxation, both documents demand the declaration of relevant financial activities within a given period, the application of specific rates, and the inclusion of potential deductions or credits. These forms embody the principle of taxing particular economic activities or goods, reinforcing sector-specific tax obligations.

Dos and Don'ts

Understanding the correct way to complete the New York Commercial Rent Tax (CRT) form is crucial for business owners in New York City. To ensure compliance with the Department of Finance and to avoid common pitfalls, here’s a concise guide outlining what you should and shouldn't do when filling out the CRT form. Keeping these guidelines in mind will help streamline the process and potentially save you from unnecessary errors and complications.

Things You Should Do

- Read the instructions carefully: Before you begin filling out the form, make sure you thoroughly review the instructions provided by the NYC Department of Finance. This will help ensure you only pay the correct amount of tax and take advantage of any applicable tax credits or deductions.

- Print or type clearly: To avoid any processing delays or errors, ensure all information is legible. If the form is not filled out clearly, it could lead to misunderstandings or incorrect tax calculations.

- Use accurate information: Verify all details, especially the Employer Identification Number (EIN), Social Security Number (SSN), and account ID. Accuracy is critical to ensure your payment is credited to the right account.

- Register for electronic filing: Consider registering for electronic filing through the NYC Department of Finance website. It's a secure, convenient way to file and pay your taxes, helping you avoid lost or delayed mail.

Things You Shouldn't Do

- Ignore mailing address changes: If your mailing address has changed, update your information online with the NYC Department of Finance before submitting your form. Failure to do so may result in important correspondence being sent to the wrong address.

- Omit Page 2: While you should not mail Page 2 and other attachments with the main form, it's crucial to complete and retain these documents for your records. They contain important calculations and information needed for accurate tax reporting.

- Estimate or guess amounts: When reporting gross rent paid, tax credits, or deductions, use actual figures instead of estimates. Guesswork can lead to incorrect tax amounts being reported, which may result in penalties or additional taxes due.

- Delay payment: Ensure your payment is made by the due date indicated on the form. Late payments can accrue penalties and interest, increasing your overall tax liability.

By following these dos and don’ts, you can more confidently navigate the process of completing the New York Commercial Rent Tax form. Remember, when in doubt, consulting with a tax professional or the Department of Finance directly can provide clarity and prevent costly mistakes.

Misconceptions

When dealing with the New York City Commercial Rent Tax (CRT), there are several misconceptions that often lead to confusion. Understanding these can help ensure compliance and potentially save businesses money. Here are nine common misconceptions about the CRT form:

Only tenants are responsible for paying the CRT. In reality, both tenants and subtenants may be required to pay the CRT, depending on their lease agreements and the specific arrangements regarding the payment of taxes.

The CRT applies to all commercial properties across NYC. The CRT specifically applies to commercial tenants in Manhattan south of the northern boundary of 96th Street, with rent thresholds determining tax liability.

All businesses pay the same rate. The CRT rate varies based on the amount of rent paid. For rents over a certain threshold, a higher percentage rate may apply.

There is no way to reduce the amount of CRT owed. In fact, there are deductions and credits available, such as the Commercial Revitalization Program reduction, that can lower the tax burden if eligible.

Calculating the CRT is straightforward and only requires knowing the monthly rent. Calculating the CRT can be complex, involving base rent computations, deductions, and the application of specific tax rates.

The CRT is calculated annually. The CRT is filed and paid quarterly, not annually, with specific deadlines for each tax period.

Filing electronically is optional. While paper filing is allowed, the New York City Department of Finance encourages electronic filing for speed and convenience, and it may become mandatory.

There's no need to keep detailed records once the CRT is filed. Maintaining detailed records of rent paid, deductions, and tax payments is crucial for audits and future filings.

Only one CRT form is used regardless of the number of premises or subtenants. Businesses with three or fewer premises or subtenants use the standard form, but those with more must use supplemental schedules or spreadsheets as instructed by the Department of Finance.

Correcting these misconceptions is key to navigating the complexities of the Commercial Rent Tax and ensuring businesses remain compliant while maximizing their allowable deductions and credits.

Key takeaways

Filing the New York Commercial Rent Tax (CRT) form requires accuracy and attention to specific details. Here are key takeaways to ensure you correctly complete and use the form:

- Know the applicable period: The CRT form is specific to the tax period. The form provided is for the first quarter of the 2014/15 tax year, covering June 1, 2014, to August 31, 2014. Always ensure you're filling out the form for the correct period.

- Understand the tax rates: The form delineates two tax rate classes based on the base rent amount. For rents up to $62,499, the tax rate is 0%. For rents of $62,500 and above, the tax rate increases to 6%.

- Compute base rent carefully: Base rent calculations are critical to determining the tax rate class. Deductions may apply, so review instructions on which amounts can be deducted from gross rent paid.

- Record premises accurately: If renting three or fewer premises or subtenants, use the provided page. For more than three, a supplemental spreadsheet is required. Accurate information about each premise, including street address and EIN/SSN, is crucial.

- Take advantage of deductions: Deductions for residential use, subtenant rents, and other allowances can significantly impact the base rent calculation. Attach schedules for any deductions claimed.

- Apply tax credits correctly: A tax credit is available if the sum of base rent and specific deductions falls within a certain range. Calculate this credit carefully using the worksheet provided.

- Electronic filing is encouraged: Register for electronic filing for a secure and convenient way to file and pay taxes. This method also ensures faster processing and reduces errors associated with manual entry.

- Payment instructions: Payments must be made payable to the NYC Department of Finance, in U.S. dollars, and drawn from a U.S. bank. Include the correct employer identification number or social security number and account ID on both the tax return and payment to ensure proper credit.

Accurately completing and submitting the CRT form is essential for compliance with New York City's tax laws. Follow the guidelines carefully to ensure the proper amount of tax is calculated and paid.

Common PDF Documents

What Is It 201 Tax Form - The precise tracking of casualty and theft losses on line 5 demonstrates the state’s commitment to accommodating unforeseen financial hardships in tax calculations.

Form It 2 - Integrates boxes for indicating participation in retirement plans, third-party sick pay, or statutory employee status.