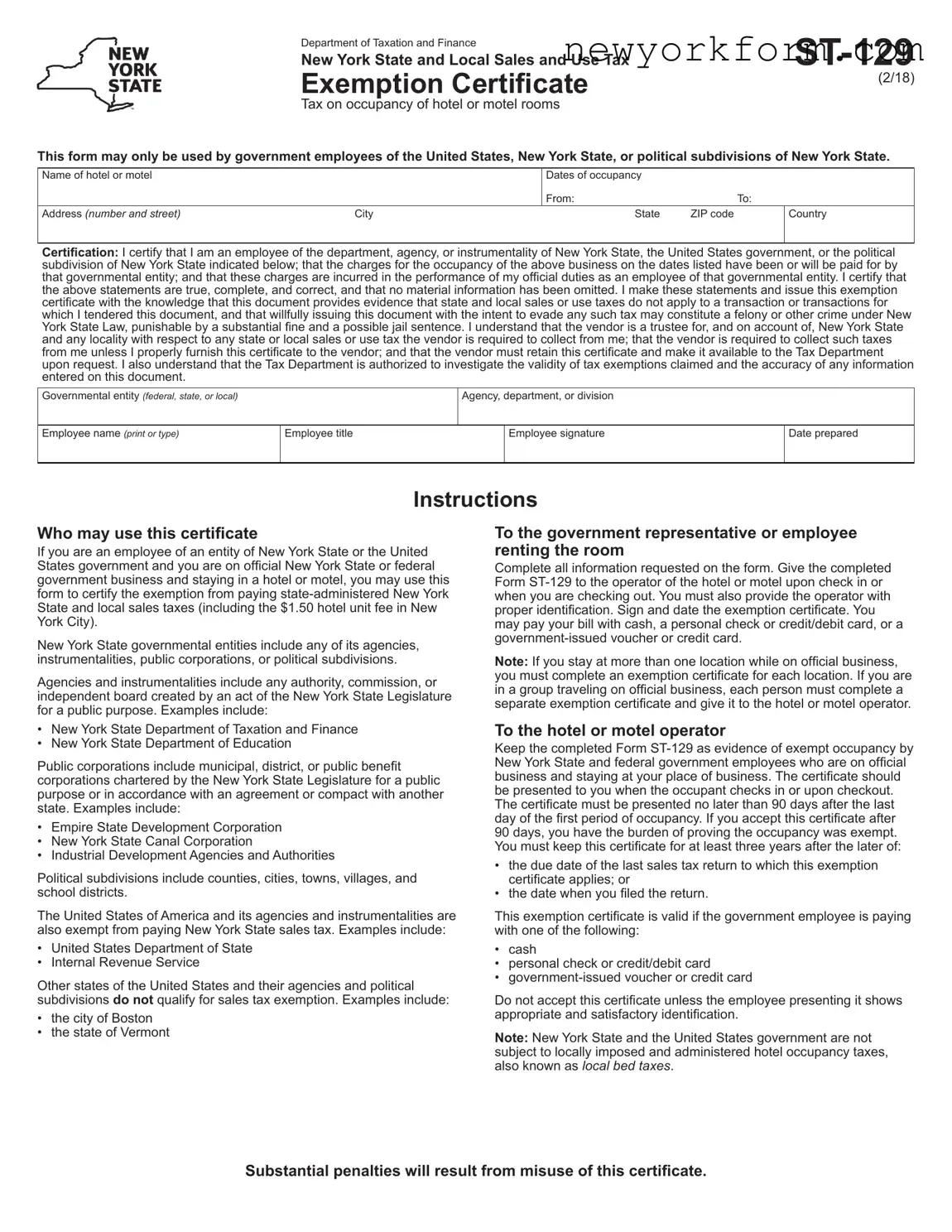

Free New York Hotel Tax Exempt Form in PDF

At the heart of the bustling hospitality sector in New York, the New York Hotel Tax Exempt form, identified formally as ST-129, serves as a crucial document for government personnel seeking exemption from state and local taxes during their hotel stays. Crafted by the Department of Taxation and Finance, this exemption specifically caters to employees of the United States government, the State of New York, and its political subdivisions, ensuring that their official duties are not financially impeded by additional lodging costs. Detailed information such as the name and address of the hotel, occupancy dates, and official identification of the employee are essential components of this certificate. It mandates an affirmation from the government employee that the expenses incurred are in the execution of official duties and funded by the respective governmental entity. Furthermore, it strictly prohibits the misuse of this document, warning of substantial penalties, including potential felony charges. This form not only outlines procedural instructions for both the governmental representative and the hotel operator but also delineates the categories of governmental bodies eligible for such exemptions, thereby playing a pivotal role in the financial interactions between governmental entities and the hospitality industry in New York.

New York Hotel Tax Exempt Sample

Department of Taxation and Finance |

|

New York State and Local Sales and Use Tax |

|

Exemption Certificate |

(2/18) |

|

Tax on occupancy of hotel or motel rooms

This form may only be used by government employees of the United States, New York State, or political subdivisions of New York State.

Name of hotel or motel |

|

Dates of occupancy |

|

|

|

|

|

|

|

|

From: |

|

|

|

To: |

|

|

Address (number and street) |

City |

|

State |

ZIP code |

|

|

Country |

|

|

|

|

|

|

|

|

|

|

Certification: I certify that I am an employee of the department, agency, or instrumentality of New York State, the United States government, or the political subdivision of New York State indicated below; that the charges for the occupancy of the above business on the dates listed have been or will be paid for by that governmental entity; and that these charges are incurred in the performance of my official duties as an employee of that governmental entity. I certify that the above statements are true, complete, and correct, and that no material information has been omitted. I make these statements and issue this exemption certificate with the knowledge that this document provides evidence that state and local sales or use taxes do not apply to a transaction or transactions for which I tendered this document, and that willfully issuing this document with the intent to evade any such tax may constitute a felony or other crime under New York State Law, punishable by a substantial fine and a possible jail sentence. I understand that the vendor is a trustee for, and on account of, New York State and any locality with respect to any state or local sales or use tax the vendor is required to collect from me; that the vendor is required to collect such taxes from me unless I properly furnish this certificate to the vendor; and that the vendor must retain this certificate and make it available to the Tax Department upon request. I also understand that the Tax Department is authorized to investigate the validity of tax exemptions claimed and the accuracy of any information entered on this document.

Governmental entity (federal, state, or local)

Agency, department, or division

Employee name (print or type)

Employee title

Employee signature

Date prepared

Instructions

Who may use this certificate

If you are an employee of an entity of New York State or the United States government and you are on official New York State or federal government business and staying in a hotel or motel, you may use this form to certify the exemption from paying

New York State governmental entities include any of its agencies, instrumentalities, public corporations, or political subdivisions.

Agencies and instrumentalities include any authority, commission, or independent board created by an act of the New York State Legislature for a public purpose. Examples include:

•New York State Department of Taxation and Finance

•New York State Department of Education

Public corporations include municipal, district, or public benefit corporations chartered by the New York State Legislature for a public purpose or in accordance with an agreement or compact with another state. Examples include:

•Empire State Development Corporation

•New York State Canal Corporation

•Industrial Development Agencies and Authorities

Political subdivisions include counties, cities, towns, villages, and school districts.

The United States of America and its agencies and instrumentalities are also exempt from paying New York State sales tax. Examples include:

•United States Department of State

•Internal Revenue Service

Other states of the United States and their agencies and political subdivisions do not qualify for sales tax exemption. Examples include:

•the city of Boston

•the state of Vermont

To the government representative or employee renting the room

Complete all information requested on the form. Give the completed Form

Note: If you stay at more than one location while on official business, you must complete an exemption certificate for each location. If you are in a group traveling on official business, each person must complete a separate exemption certificate and give it to the hotel or motel operator.

To the hotel or motel operator

Keep the completed Form

90 days, you have the burden of proving the occupancy was exempt. You must keep this certificate for at least three years after the later of:

•the due date of the last sales tax return to which this exemption certificate applies; or

•the date when you filed the return.

This exemption certificate is valid if the government employee is paying with one of the following:

•cash

•personal check or credit/debit card

•

Do not accept this certificate unless the employee presenting it shows appropriate and satisfactory identification.

Note: New York State and the United States government are not subject to locally imposed and administered hotel occupancy taxes, also known as local bed taxes.

Substantial penalties will result from misuse of this certificate.

File Overview

| Fact Name | Detail |

|---|---|

| Eligibility for Use | This form is exclusively for government employees of the United States, New York State, or political subdivisions of New York State who are on official business. |

| Exemption Scope | It certifies exemption from state-administered New York State and local sales taxes on hotel or motel room occupancy, including the $1.50 hotel unit fee in New York City. |

| Valid Payment Methods | The exemption is valid if the government employee pays with cash, a personal check or credit/debit card, or a government-issued voucher or credit card. |

| Retention and Presentation | The hotel or motel operator must retain the completed form for at least three years and it must be presented within 90 days from the last day of the first occupancy period. |

New York Hotel Tax Exempt: Usage Guidelines

Filling out the New York Hotel Tax Exempt form is a straightforward process that requires attention to detail. This form is an essential document for government employees who are seeking an exemption from state and local sales taxes on hotel or motel room occupancy. By completing this form correctly, eligible government employees can ensure their stays are tax-exempt, providing they are on official business. Below are the steps to accurately fill out the form.

- Enter the Name of hotel or motel where you will be staying.

- Fill in the Dates of occupancy, including both the 'From:' and 'To:' dates.

- Provide the Address of the hotel or motel, including the number and street, City, State, ZIP code, and Country.

- In the Certification section, confirm your status as a government employee by including the name of the governmental entity (federal, state, or local) you are employed by.

- Include your Agency, department, or division within the governmental entity.

- Print or type your Employee name clearly.

- Enter your Employee title.

- Sign your name in the space provided for the Employee signature.

- Correctly fill in the Date prepared with the current date.

Once the form is completed, remember to present it to the hotel or motel operator at the time of check-in or upon checking out. You must also show proper identification to validate your tax-exempt status. If payment is made with cash, a personal check, credit/debit card, or a government-issued voucher or credit card, ensure this information is known to the operator. For government employees traveling in a group, each individual must complete and submit a separate exemption certificate. Keeping a copy for your records is advisable, as the hotel or motel operator is required to retain the original for a specified period.

FAQ

Welcome to the FAQ section about the New York Hotel Tax Exempt form. This section seeks to answer some of the most common questions regarding the use and application of the ST-129 form, utilized by government employees for tax exemption on hotel or motel room occupancy in New York.

Who is eligible to use the New York Hotel Tax Exempt form (ST-129)?

This form is exclusively available for use by employees of the United States government, New York State, or its political subdivisions when these employees are on official business and need accommodation in hotels or motels. This includes employees from agencies, instrumentalities, public corporations, and political subdivisions of New York State, as well as the federal government.

What are the steps to properly fill out and submit the ST-129 form?

Government representatives or employees should complete every section of the form, providing details about the hotel or motel, dates of occupancy, and their government entity. Upon check-in or checkout at the hotel or motel, the completed form should be presented alongside proper identification. Payment for the stay can be made using cash, personal checks, credit/debit cards, or government-issued vouchers or credit cards. For group travel on official business, each member should fill out separate exemption certificates.

Can the ST-129 form be used for stays in more than one hotel?

No, if you are staying in multiple locations while on official business, a separate exemption certificate must be completed for each location. This ensures that the tax exemption is properly documented and applied at each distinct place of stay.

Is the ST-129 form applicable to employees of other states?

Employees of other states or their political subdivisions do not qualify for this specific tax exemption in New York. The ST-129 form is designed solely for federal employees or employees of New York State and its political subdivisions on official business.

What are the consequences of misuse or fraudulent use of the ST-129 form?

The form clearly states that willfully issuing this certificate to evade tax constitutes a felony or other crime under New York State Law, which is punishable by significant fines and possibly imprisonment. Moreover, substantial penalties can result from the misuse of this certificate.

What responsibilities do hotels and motels have regarding the ST-129 form?

Operators are required to retain the completed ST-129 form as evidence of exempt occupancy. The certificate, which must be presented no later than 90 days after the last day of occupancy, should be kept for at least three years after the relevant sales tax return is due or filed. Operators must ensure that the form is properly filled and presented with appropriate identification before accepting it.

Are there any tax exemptions from local hotel occupancy taxes using the ST-129 form?

Yes, New York State and United States government employees, while staying on official business, are exempt not only from state-administered New York State and local sales taxes but also from locally imposed hotel occupancy taxes, commonly known as local bed taxes. It’s crucial to note, however, that proper procedures must be followed, and the ST-129 form must be accurately completed and submitted.

This FAQ aims to provide clear guidance on the application and usage of the ST-129 New York Hotel Tax Exempt form. For further assistance, governmental entities and hotel operators are advised to directly consult with the New York State Department of Taxation and Finance.

Common mistakes

Filling out the New York Hotel Tax Exempt form accurately is crucial for eligible government employees to ensure tax exemption on hotel stays while on official business. However, individuals often make mistakes that can lead to the rejection of their tax exemption claim. Understanding these common errors can save time and prevent unnecessary problems.

Here are eight common mistakes to avoid:

- Not fully completing the form - Sometimes, sections of the form are left blank. It's important to fill out every required field to provide the hotel or motel with all necessary information for processing the exemption.

- Incorrect dates of occupancy - Entering the wrong dates for the stay or forgetting to include them altogether can lead to confusion and potential denial of the exemption.

- Failure to provide adequate identification - Proper identification must be shown when submitting the form to verify government employment. Neglecting to provide this can result in the form not being accepted.

- Inaccurate entity information - The form requires specific information about the governmental entity paying for the stay. Mistakes in this section can cast doubt on the eligibility for tax exemption.

- Not signing the form - The employee must sign the form to certify that the information provided is accurate and the stay is for official business. An unsigned form is incomplete and will not be accepted.

- Forgetting to date the form - Along with a signature, the form must be dated to confirm when the exemption certificate was completed. This ensures the form is submitted within the acceptable timeframe.

- Using the form for ineligible stays - The exemption only applies to official business stays. Using the form for personal stays, even partially, is incorrect and could lead to penalties.

- Late submission - The form must be presented at check-in or checkout and within 90 days of the stay. Late submissions shift the burden of proof of exemption to the hotel operator and may not be accepted.

Besides these specific errors, it's also essential to remember that this tax exemption cannot be used by government employees of other states or for non-official stays. Misuse of the New York Hotel Tax Exempt form not only leads to complications in processing exemptions but may also result in legal penalties for the individual involved.

To ensure a smooth process, it's recommended that all information be reviewed for accuracy and completeness before submitting the form to the hotel or motel operator. Adequate preparation and attention to detail can prevent these common mistakes and ensure that the tax exemption is correctly applied.

Documents used along the form

In the process of handling hotel tax-exempt accommodations, especially for government employees, beyond the New York Hotel Tax Exempt form (ST-129), several other documents and forms are commonly utilized to ensure compliance, accuracy, and authorization of tax exemption claims. These documents support the exemption process by providing necessary details related to the stay, the government entity involved, and the employee's status. Understanding each document’s purpose can streamline the exemption process, guaranteeing that all requirements are meticulously met while reducing the likelihood of errors or delays.

- Government-Issued Identification (ID): Essential for verifying the identity of the government employee claiming exemption. This could include a federal or state ID card that clearly shows the employee’s name, photo, and the employing agency.

- Official Travel Orders: These documents authorize the travel and stay of government employees, detailing the necessity of the trip as related to governmental duties, thereby supporting the tax-exempt status of the lodging expenses.

- Direct Billing Authorization: A letter or form used by government entities to arrange direct billing to the department or agency. It helps bypass the need for employees to pay out of pocket, further substantiating the official nature of the stay.

- Purchase Orders: Often used for government travel, these authorize payment for lodging directly from the government agency to the hotel, specifying terms and limits of the authorized expenses.

- Exemption Certificate for Other States: For employees of out-of-state government entities traveling to New York, similar exemption certificates might be required to prove eligibility for tax exemption under their state’s laws.

- Credit Card Authorization Form: Utilized when the hotel charges are to be paid for with a government-issued credit card, this form authorizes the hotel to charge the provided card, often including billing instructions specific to government payments.

- Proof of Payment: While not required upfront, retaining detailed receipts and proof of payment is critical for both the government employee and the agency for auditing purposes and to verify that the stay was indeed paid for by the government entity.

- Letter of Justification for Stay: Sometimes required by finance departments inside government agencies, this letter explains the necessity of the stay in detail, offering further documentation that the travel is for official government business and thus eligible for tax-exempt status.

Combining the New York Hotel Tax Exempt form with these supporting documents creates a robust framework that ensures all parties involved—government employees, their employing agencies, and the lodging facilities—are well-informed and compliant with applicable tax laws. This meticulous documentation not only facilitates the tax exemption process but also upholds accountability and transparency, ensuring that government travel remains within the bounds of authorized and necessary expenditures.

Similar forms

The New York Sales Tax Exemption Certificate for Purchases related to Government Functions, often utilized by various government agencies for tax-exempt purchases, shares a core similarity with the New York Hotel Tax Exempt form. Both documents serve the primary function of certifying tax-exempt transactions for government-related activities. Each form carefully outlines the conditions under which exemptions apply, specifically for purchases or services used in the execution of official government duties, thereby preventing misuse and ensuring compliance with New York State tax laws.

The Certificate of Exemption for Interstate Commerce, another document used in tax law, parallels the New York Hotel Tax Exempt form in its delineation of exemptions under specific circumstances – in this case, for transactions that cross state lines. This similarity lies in their shared objective of defining a narrow set of conditions that qualify for tax exemptions, emphasizing the need for detailed documentation and proper certification to legitimize the tax-exempt status.

The Employee Business Expense Reimbursement Exemption Certificate echoes the New York Hotel Tax Exempt form by offering a framework through which employees can make exempt purchases. However, this is limited to situations where expenses are directly related to job functions. Both forms necessitate the employee's certification that the expenses incurred are for official business purposes, underscoring the importance of accountability and proper use of exemption privileges.

The Educational Institution Exemption Certificate focuses on tax exemptions specifically for educational institutions, which mirrors the purposeful specificity found in the New York Hotel Tax Exempt form. Like the hotel exemption, the education exemption certificate is designed with a clear beneficiary in mind and sets forth conditions for tax exemption tailored to the organization’s functions, highlighting both forms’ roles in facilitating specific tax policy objectives.

The Non-profit Organization Tax Exempt Certificate shares a core premise with the New York Hotel Tax Exempt form, as both are used to certify tax exemptions under defined circumstances. For non-profits, the form asserts purchases made for the organization's exempt activities are not taxable. The similarity lies in their structural role in the tax system—both serve as essential tools for entities to claim exemptions, based on their respective activities and statuses under state law.

Resale Exemption Certificates are crucial for businesses purchasing goods intended for resale. This certificate's similarity to the New York Hotel Tax Exempt form is found in their mutual requirement for the purchaser to certify the purpose behind the tax-exempt status. Both forms play pivotal roles in delineating the flow of tax responsibilities, ensuring tax is applied only at the final point of sale to the consumer.

The Agricultural Exemption Certificate, used by farmers and agricultural producers, closely aligns with the New York Hotel Tax Exempt form through its focus on specific conditions under which tax exemptions apply. Each certificate is tailored to its audience, providing clear guidelines for when and how exemptions can be claimed, reflecting the nuanced application of tax laws to different sectors of the economy.

The Utility Exemption Certificate, applicable for utility purchases made by qualifying entities, shares a similar goal with the New York Hotel Tax Exempt form: facilitating tax exemptions under carefully defined circumstances. Both stress the importance of certifying that the purchases or use cases meet specific criteria, underlining the tight regulatory framework governing tax exemptions.

The Streamlined Sales and Use Tax Agreement Certificate of Exemption offers a multijurisdictional approach to claiming sales tax exemptions, akin to the New York Hotel Tax Exempt form's more localized focus. Both facilitate tax exemption processes within their scopes, emphasizing the necessity for eligible entities or individuals to provide accurate information and certifications to qualify for exemptions.

Finally, the Direct Pay Permit mirrors the New York Hotel Tax Exempt form in providing a pathway through which entities can directly manage tax payment obligations, circumventing the usual collection process at point of sale. Unique in approach, both documents require stringent qualifications and offer an alternative framework for handling tax liabilities, underscoring their roles in customized tax compliance strategies within New York State's tax law environment.

Dos and Don'ts

When filling out the New York Hotel Tax Exempt form, accuracy and attention to detail are crucial for ensuring that government employees can rightfully claim exemption from state and local sales taxes during their hotel or motel stay. Following guidelines and common mistakes to avoid will help streamline this process.

Do:- Verify your eligibility before attempting to use the form. Ensure you are a government employee of the United States, New York State, or a political subdivision of New York State on official business.

- Complete all requested information on the form thoroughly and accurately to avoid any delay in the processing of your tax exemption.

- Provide proper identification along with the form to the hotel or motel operator, as this is required to validate your exemption claim.

- Pay for your stay using an acceptable method of payment as stated in the instructions, including cash, a personal check, a credit/debit card, or a government-issued voucher or credit card.

- Sign and date the exemption certificate yourself to certify that the information provided is true and correct, and that the stay is for official government business.

- Submit a separate exemption certificate for each location if staying at more than one hotel or motel on official business, or if traveling as part of a group.

- Provide the completed form to the hotel or motel operator upon checking in or checking out, as per the instructions provided.

- Assume eligibility without confirming that your stay is for official government duties. Personal stays do not qualify for tax exemption.

- Leave sections of the form blank, as incomplete forms may not be accepted, resulting in an inability to claim the tax exemption.

- Forget to present valid identification along with your form, as failure to do so can lead to the rejection of your exemption claim.

- Delay the submission of your exemption certificate beyond your checkout time, as this can complicate the exemption process.

- Use the exemption for non-qualifying stays, such as leisure travel or stays funded by non-governmental sources, which are not exempt under this certificate.

- Ignore the requirement for separate certificates for each location or individual in a group, as each is needed for proper processing.

- Fail to follow up if your exemption is questioned or if additional information is required to verify the exemption's validity.

Misconceptions

Misconceptions about the New York Hotel Tax Exempt form can lead to confusion for both government employees and hoteliers. Here are nine common ones explained:

- Only federal employees are eligible. Actually, the form can be used by employees of the United States, New York State, or political subdivisions of New York State, not solely federal employees.

- The form covers all taxes. This is not entirely true; while it exempts eligible government employees from state-administered sales taxes, it doesn't apply to other states or local bed taxes that may be imposed and administered locally.

- It applies to personal stays. The exemption is strictly for official government business. It cannot be used for personal stays under any circumstances.

- Any government employee can use it, regardless of state. No, it is specifically for government employees of the United States, New York State, or its political subdivisions. Employees of other states or their subdivisions do not qualify.

- All forms of payment qualify. The form validly exempts an employee only when paying with cash, a personal check or credit/debit card, or a government-issued voucher or credit card.

- It's unnecessary to present ID. On the contrary, employees must also provide appropriate and satisfactory identification when presenting this exemption certificate to the hotel or motel operator.

- A single form is enough for group travels. Each government employee traveling on official business must fill out and present a separate exemption certificate, even when traveling as part of a group.

- The form has unlimited duration. The certificate must be presented no later than 90 days after the last day of the first period of occupancy. Timeliness is crucial for its acceptance.

- Hotel operators need not retain the form. Operators are required to keep the completed Form ST-129 for at least three years after the later of the due date of the last sales tax return to which it applies, or the date when you filed the return. This is to provide evidence of exempt occupancy.

Understanding these points ensures that the process runs smoothly for both government personnel on official duties and the accommodating hotels, ensuring compliance with New York’s taxation laws.

Key takeaways

Filling out and using the New York Hotel Tax Exempt form requires attention to detail and knowledge of the eligibility criteria. This document grants a sales tax exemption on hotel or motel rooms to qualified individuals on official business for New York State, the United States government, or political subdivisions of New York State. Here are key takeaways about this important exemption certificate:

- The form ST-129 is exclusively for government employees of the United States, New York State, or political subdivisions of New York State, ensuring they are not charged state and local sales and use tax on hotel or motel room occupancy.

- To qualify, an individual must certify that their hotel charges are paid for by a governmental entity and that the stay is directly connected to the performance of their official duties.

- It is imperative that the form is filled out completely and accurately, as providing false or incomplete information could lead to legal consequences, including a possible felony charge.

- The form serves as proof that state and local sales or use taxes do not apply to the transaction, placing the burden on the vendor to collect taxes unless this certificate is properly furnished.

- Operators of hotels and motels are required to retain the completed exemption certificate and make it available to the New York State Tax Department upon request, keeping it for at least three years after the relevant sales tax return's due date or the date it was filed, whichever is later.

- When checking into or out of a hotel or motel, the government employee must present the completed form along with appropriate and satisfactory identification to the operator.

- Payments for room charges can be made using cash, a personal or government-issued check, credit/debit card, or a government-issued voucher or credit card.

- New York State and the United States government, including their agencies and instrumentalities, are exempt from locally imposed and administered hotel occupancy taxes or local bed taxes.

By adhering to these guidelines, government employees can ensure compliance with New York State's tax exemption requirements, potentially avoiding penalties for misuse of the form. It's a responsibility of both the government employee and the hotel or motel operator to understand and respect the conditions under which this tax exemption applies.

Common PDF Documents

Nyc Lease Renewal Form Pdf - It includes spaces for the mailing addresses of both the tenant and the owner/managing agent to facilitate comprehensive documentation.

Poa Affidavit - A critical step in the process for attorneys-in-fact to continue managing pensions without interruptions.