Free New York Et 95 Form in PDF

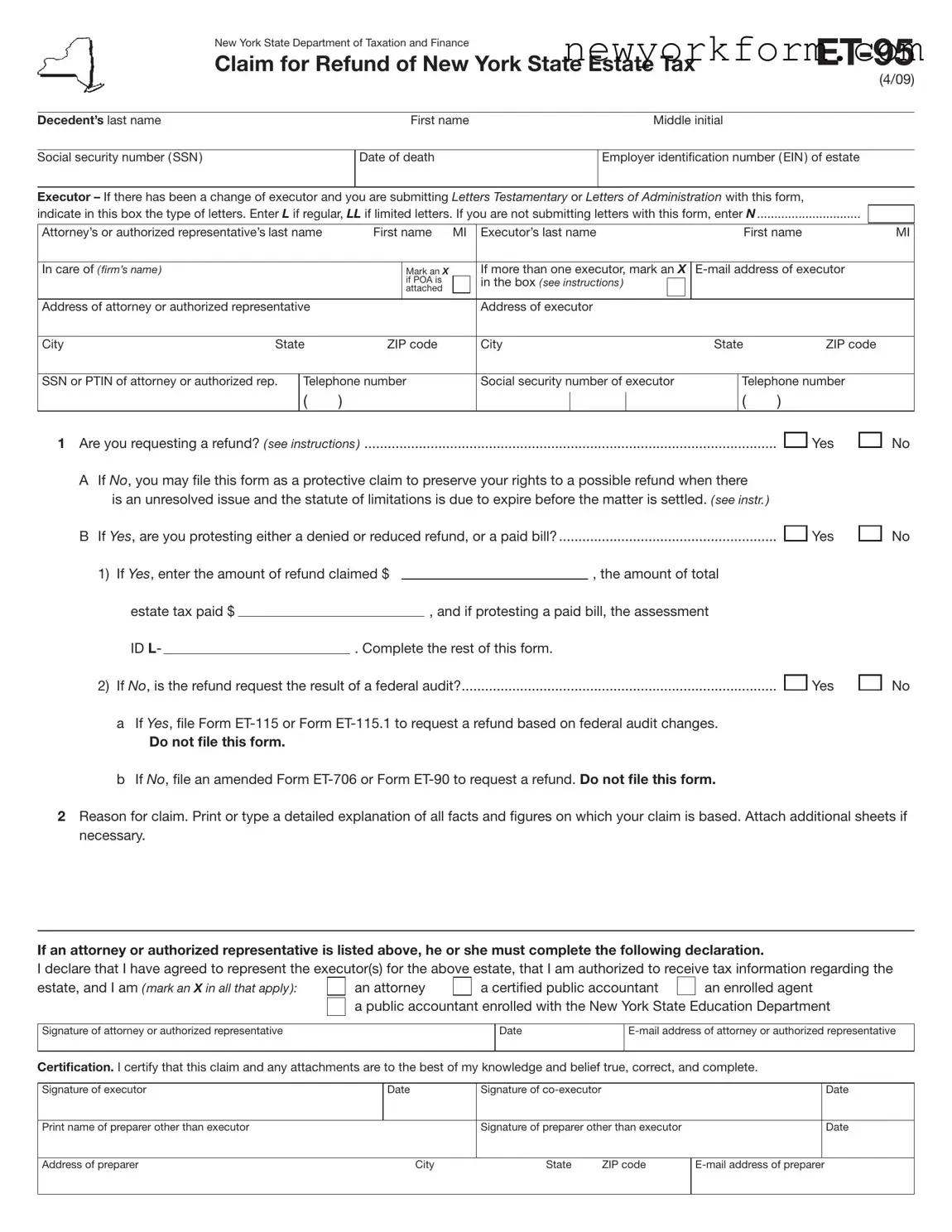

When navigating the complexities of estate management and taxation in the Empire State, one critical document that often comes into play is the ET-95 form officially titled "Claim for Refund of New York State Estate Tax." This form, issued by the New York State Department of Taxation and Finance, serves as a crucial tool for executors or authorized representatives handling the affairs of a deceased's estate. It's designed to facilitate refunds of overpaid estate taxes, yet it can be employed under various circumstances beyond simple overpayment. Whether it's challenging a denied refund, filing a protective claim to safeguard the right to a future refund amidst unresolved tax matters, or contesting a tax bill already paid, the ET-95 form stands as a pivotal recourse. Detailed information required includes the decedent's personal details, such as their name and social security number, the executor's information, and, if applicable, details of any attorney or authorized representative. Moreover, the form demands a nuanced explanation of the refund claim's reasoning, underscoring the importance of thoroughness and accuracy in its completion. With stringent deadlines governing the submission window based on the date of the original tax filing or payment, understanding the nuances and provisions of the ET-95 cannot be overstated for those seeking justice or correction in estate tax assessments.

New York Et 95 Sample

|

New York State Department of Taxation and Finance |

|

||

|

Claim for Refund of New York State Estate Tax |

|||

|

|

|

|

(4/09) |

|

|

|

|

|

Decedent’s last name |

|

First name |

Middle initial |

|

|

|

|

|

|

Social security number ( SSN ) |

|

Date of death |

Employer identiication number ( EIN ) of estate |

|

|

|

|

|

|

Executor – If there has been a change of executor and you are submitting Letters Testamentary or Letters of Administration with this form,

indicate in this box the type of letters. Enter L if regular, LL if limited letters. If you are not submitting letters with this form, enter N..............................

Attorney’s or authorized representative’s last name |

First name |

MI |

Executor’s last name |

|

First name |

MI |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

In care of ( firm’s name ) |

|

|

|

Mark an X |

|

|

If more than one executor, mark an X |

||||||||

|

|

|

|

if POA is |

|

|

in the box ( see instructions ) |

|

|

|

|

|

|

||

|

|

|

|

attached |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of attorney or authorized representative |

|

|

|

|

Address of executor |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

ZIP code |

|

|

City |

State |

|

ZIP code |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

SSN or PTIN of attorney or authorized rep. |

Telephone number |

|

|

Social security number of executor |

|

Telephone number |

|||||||||

|

|

( |

) |

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 Are you requesting a refund? ( see instructions ) |

|

Yes |

A If No, you may ile this form as a protective claim to preserve your rights to a possible refund when there |

|

|

is an unresolved issue and the statute of limitations is due to expire before the matter is settled. ( see instr. ) |

|

|

B If Yes, are you protesting either a denied or reduced refund, or a paid bill? |

|

Yes |

|

No

No

1) If Yes, enter the amount of refund claimed $ |

|

, the amount of total |

estate tax paid $ |

|

|

, and if protesting a paid bill, the assessment |

|

|

|

ID L- |

|

|

. Complete the rest of this form. |

|

|

|

2) If No, is the refund request the result of a federal audit? |

|

Yes |

||||

|

||||||

aIf Yes, ile Form

Do not file this form.

b If No, ile an amended Form

No

2Reason for claim. Print or type a detailed explanation of all facts and igures on which your claim is based. Attach additional sheets if necessary.

If an attorney or authorized representative is listed above, he or she must complete the following declaration.

I declare that I have agreed to represent the executor(s) for the above estate, that I am authorized to receive tax information regarding the

estate, and I am ( mark an X in all that apply ):

an attorney

an attorney

a certiied public accountant

a certiied public accountant

an enrolled agent a public accountant enrolled with the New York State Education Department

an enrolled agent a public accountant enrolled with the New York State Education Department

Signature of attorney or authorized representative |

Date |

|

|

|

|

Certification. I certify that this claim and any attachments are to the best of my knowledge and belief true, correct, and complete.

Signature of executor |

Date |

Signature of |

|

|

Date |

|

|

|

|

|

|

Print name of preparer other than executor |

|

Signature of preparer other than executor |

|

Date |

|

|

|

|

|

|

|

Address of preparer |

City |

State |

ZIP code |

||

|

|

|

|

|

|

Instructions

Use this form to claim a refund of New York State estate tax only for the following types of claims:

Protest of denied refund — If the Tax Department has denied or adjusted your refund for any reason other than offsets to amounts owed to other agencies or tax liabilities, you may immediately ile a formal claim for refund.

Protective claim * — A protective claim is a refund claim that is based on an unresolved issue(s) that involves the Tax Department or another taxing jurisdiction that may affect your New York State estate tax. The purpose of iling a protective claim is to protect any potential overpayment when the statute of limitations is due to expire.

Protest of paid bill * — If the bill was based on Form

*Note: Your protective claim or protest must be iled within three years from the time the return was iled or within two years from the time the tax was paid, whichever is later.

File all other claims, for dates of death after May 25, 1990, and before February 1, 2000, on Form

Executor information

Enter the name (last name irst) and other information for the executor of the estate. The term executor includes executrix, administrator, administratrix, or personal representative of the decedent’s estate; if no executor, executrix, administrator, administratrix, or personal representative is appointed, qualiied, and acting within the United States, executor means any person in actual or constructive possession of any property of the decedent.

If an executor has not been appointed, this form may be signed and iled by a person having knowledge of all the assets in the decedent’s estate. This person must also enter his or her name, address, and social security number in the area provided for the executor on the front of this form.

If the estate has more than one executor, mark an X in the box, enter the name and other information for the primary executor (preferably a person residing in New York State) in the area provided, and attach a list of each of the other executors with their mailing address and social security number if not previously submitted. Submit Letters Testamentary or Letters of Administration with this form if not previously submitted. It is suficient to have one of the coexecutors sign this form.

Attorney/representative information

If you, as the executor of the estate, have authorized a person to represent you regarding the estate, and you would like the department to contact him or her regarding the estate, enter the name (last name irst) of the attorney, accountant, or enrolled agent who is representing you. Also enter the irm’s name, address, and telephone number in the areas provided, and have the representative sign in the area provided on the front of this form.

Note: If you are giving a person power of attorney to represent you, attach a completed Form

Sign this claim and mail to:

NYS TAX DEPARTMENT

TDAB - ESTATE TAX AUDIT

W A HARRIMAN CAMPUS

ALBANY NY 12227

Privacy notification

The Commissioner of Taxation and Finance may collect and maintain personal information pursuant to the New York State Tax Law, including but not limited to, sections

This information will be used to determine and administer tax liabilities and, when authorized by law, for certain tax offset and exchange of tax information programs as well as for any other lawful purpose.

Information concerning quarterly wages paid to employees is provided to certain state agencies for purposes of fraud prevention, support enforcement, evaluation of the effectiveness of certain employment and training programs and other purposes authorized by law.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Manager of Document Management, NYS Tax Department, W A Harriman Campus, Albany NY 12227; telephone (518)

Need help?

Internet access: www.nystax.gov

(for information, forms, and publications)

|

|

available 24 hours a day, |

|

7 days a week. |

1 800 |

Telephone assistance is available from 8:00 A.M. to 5:00 P.M. (eastern time), Monday through Friday.

Estate Tax Information Center: |

(518) |

|

1 800 |

||

To order forms and publications: |

(518) |

|

1 800 |

Text Telephone (TTY) Hotline (for persons with hearing and speech disabilities using a TTY): If you have access to a TTY, contact us at 1 800

If you do not own a TTY, check with independent living centers or community action programs to ind out where machines are available for public use.

Persons with disabilities: In compliance with the Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and other facilities are accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.

File Overview

| Fact | Detail |

|---|---|

| Form Number | ET-95 |

| Issue Date | April 2009 (4/09) |

| Form Title | Claim for Refund of New York State Estate Tax |

| Issuing Agency | New York State Department of Taxation and Finance |

| Purpose | Used to claim a refund of New York State estate tax for denied refunds, protective claims, or protests of paid bills |

| Governing Law(s) | New York State Tax Law |

| Submission Destination | NYS TAX DEPARTMENT, TDAB - ESTATE TAX AUDIT, W A HARRIMAN CAMPUS, ALBANY NY 12227 |

| Who Can File | Executors of the decedent’s estate or their authorized representatives |

New York Et 95: Usage Guidelines

Filing a New York ET-95 form is a critical process for claiming a refund of New York State estate tax under specific circumstances such as a protest of a denied refund, a protective claim, or a protest of a paid bill. This paperwork plays a pivotal role in ensuring that any overpayment of estate taxes due to the estate can be rightfully returned. Accuracy and thoroughness in completing this form are paramount to facilitate the prompt processing of your claim. Below are step-by-step instructions designed to guide you through the process of accurately filling out the form.

- Start with the decedent’s information, including last name, first name, middle initial, and social security number (SSN). Then, input the date of death and the estate's employer identification number (EIN) if available.

- In the section labeled Executor, if there has been a change of executor since the initial filing, indicate the type of letters testamentary or letters of administration submitted by marking L for regular or LL for limited letters. If no letters are being submitted with this form, enter N.

- Fill in the attorney’s or authorized representative’s information including last name, first name, MI (middle initial), the name of the firm (in care of), and the address. If more than one executor exists, ensure to mark an X in the indicated box.

- Input the executor's contact information including the address, city, state, ZIP code, and telephone number. If an attorney or authorized representative is appointed, their contact information should be listed as well.

- For question 1 on the form, specify if you are requesting a refund by marking Yes or No. If “Yes,” include the amount of the refund claimed, the total estate tax paid, and the assessment ID if applicable.

- If the refund request results from a federal audit, indicate by marking Yes under question 1b and follow the provided instructions regarding the filing of Form ET-115 or Form ET-115.1 instead.

- In the section labeled Reason for claim, provide a detailed explanation for your refund claim. Include all necessary facts, figures, and attach additional sheets if necessary.

- If an attorney or authorized representative is completing the form, they must mark the appropriate box to indicate their relationship to the estate (attorney, certified public accountant, enrolled agent, or public accountant) and sign and date the form.

- Finally, the executor or co-executor must certify the claim by signing and dating the form. If another person prepared the form, their information should be included as well.

- Review all entered information for accuracy and completeness. Once satisfied, mail the signed form to the address provided on the form: NYS TAX DEPARTMENT TDAB - ESTATE TAX AUDIT, W A HARRIMAN CAMPUS, ALBANY NY 12227.

Completing the ET-95 form accurately is vital to ensuring the estate's financial affairs are settled properly. It helps to safeguard the estate against any potential loss due to overpaid taxes and ensures that any due refunds are efficiently processed and returned to the estate. Following these instructions will aid in a seamless process, contributing to a swift resolution of your estate tax matters.

FAQ

- What is the purpose of the New York ET-95 form?

- Who can file the ET-95 form?

- What documentation is required when submitting the ET-95 form?

- How is the ET-95 form submitted?

- What are the deadlines for filing the ET-95 form?

The New York ET-95 form, titled "Claim for Refund of New York State Estate Tax," is designed for individuals seeking a refund of estate tax paid to the New York State Department of Taxation and Finance. This form is specifically used under three circumstances: to protest a denied or reduced refund, to file a protective claim preserving rights to a possible refund while an issue is unresolved, and to protest a paid bill based on specific assessments or notices provided by the Tax Department. It ensures that claimants can articulate the basis for their refund request, whether stemming from a direct denial or adjustment by the state, or proactively in anticipation of potential disputes.

The ET-95 form can be filed by the executor of the decedent's estate or, if no executor has been appointed, any person in possession of the decedent's property who has knowledge of the estate's assets. This includes individuals holding titles such as executor, executrix, administrator, personal representative, or a similar role responsible for managing the deceased's estate. If the estate has multiple executors, a primary executor, preferably located in New York State, should be identified, and a list of all co-executors should be attached.

When filing the ET-95 form, claimants must attach all necessary documentation supporting their refund claim. This includes a detailed explanation of the facts and figures forming the basis of the claim, any related Letters Testamentary or Letters of Administration if there has been a change of executor, and additional sheets if the space provided is insufficient. For those represented by an attorney or authorized agent, a duly completed and signed declaration by the representative is required, alongside any previously unsubmitted Estate Tax Power of Attorney forms.

The completed ET-95 form, along with all accompanying documents and attachments, should be mailed to the NYS TAX DEPARTMENT at the TDAB - ESTATE TAX AUDIT, W A HARRIMAN CAMPUS, ALBANY NY 12227. Before mailing, ensure that the form and all supporting documentation are complete and accurate to avoid processing delays.

The ET-95 form must be filed within strict time frames based on either the date the original tax return was filed or the date the tax was paid, whichever is later. Specifically, a protective claim or protest must be filed within three years from the time the return was filed or within two years from the time the tax was paid. For claims relating to dates of death after May 25, 1990, and before February 1, 2000, the form ET-90 should be used instead, marked as AMENDED. For dates of death on or after February 1, 2000, Form ET-706 is appropriate, with an indication made on the top of the form.

Common mistakes

Filling out the New York ET-95 form, known as the Claim for Refund of New York State Estate Tax, can be complex. Individuals often make several common mistakes during this process that can lead to delays or the denial of their claim. Understanding these errors is crucial to ensure a smooth and successful refund claim.

One of the first mistakes involves incorrect or incomplete executor information. The form requires detailed information regarding the executor's name, contact details, and Social Security number. If more than one executor exists, marking the appropriate box and providing information for each is necessary. Failure to do so might result in processing delays.

Another error is not attaching the necessary documentation, such as Letters Testamentary or Letters of Administration, if there has been a change of executor. These documents are crucial for the Department of Taxation and Finance to verify the executor's authority.

Further, individuals often overlook the need to select the correct reason for the claim. The form provides options for claims related to protested denied refunds, protective claims, and protests of paid bills. Choosing the wrong category can lead to confusion and potential rejection of the claim.

- Incorrect or incomplete executor information, crucial for processing the claim.

- Failure to attach essential documents like Letters Testamentary or Letters of Administration.

- Not correctly identifying the reason for the claim can lead to confusion and potential rejection.

- Providing inaccurate tax amounts, either the refund claimed or the estate tax paid, can lead to discrepancies and audit issues.

- Omitting or incorrectly filling out the social security numbers of the executor or the decedent, a critical step for identification and processing.

- Not marking the appropriate boxes for changes in executor status or other relevant details, which can lead to misunderstanding and processing hurdles.

- Forgetting to sign and date the form, a fundamental requirement for the claim's validity.

- Misunderstanding the statute of limitations and filing the claim too late, thus forfeiting the right to a refund or the ability to protest.

These common pitfalls highlight the importance of carefully reviewing all sections of the ET-95 form and ensuring that all required information is complete and accurate. Remember, when in doubt, seeking the advice of a tax professional or attorney is advisable to avoid errors that could impact the outcome of your refund claim.

- Accuracy in filling out the form is paramount to avoid delays or denials.

- Attaching and correctly filling out all supplementary documents is a non-negotiable part of the process.

- Understanding the intricacies of estate tax laws in New York can aid in a smoother claim process.

Ultimately, the key to successfully navigating the Claim for Refund of New York State Estate Tax lies in attention to detail, thoroughness, and, when necessary, seeking experienced guidance. Avoiding these common errors can significantly increase the chances of a favorable resolution to your refund claim.

Documents used along the form

When dealing with the ET-95 form for claiming a refund of New York State estate tax, it's important to recognize that this form doesn't stand alone. Several other documents often accompany or support the ET-95 form, each serving its unique function in the process of handling an estate's financial and legal matters. Understanding these forms can provide clarity and ensure that the process is as smooth as possible.

- ET-706, New York State Estate Tax Return: This form is used for filing estate taxes with the state of New York. If changes at the federal level affect the state tax owed, an amended ET-706 may accompany the ET-95.

- ET-90, Amended Estate Tax Return: For dates of death before February 1, 2000, this form is used instead of the ET-706 to amend previously filed estate tax returns.

- ET-14, Estate Tax Power of Attorney: If an executor authorizes someone to represent them concerning the estate, this form grants that authority officially.

- ET-115 or ET-115.1, Request for Refund Based on Federal Audit Changes: These forms apply when federal audit adjustments necessitate a refund from the New York State estate tax.

- Letters Testamentary or Letters of Administration: These documents are issued by the court, authorizing an individual to act as the executor or administrator of the estate.

- DTF-960, Statement of Proposed Audit Changes: If the state proposes adjustments to the reported estate tax, this document outlines those changes.

- DTF-961, Notice of Additional Tax Due: This notice informs the estate of additional taxes owed following an audit or review.

- DTF-966.1, Notice and Demand for Payment of Tax Due: Should there be a discrepancy or outstanding tax due, this form is sent to demand payment.

- Death Certificate: While not a tax form, a certified copy of the death certificate is often required to accompany tax filings for the estate.

- Federal Estate Tax Return (Form 706): For estates that need to file federally, this return, and any amendments, may influence the state tax situation.

Navigating the intricacies of estate taxation can be daunting. Each document serves a role in ensuring the estate is handled correctly and in compliance with state and federal laws. It's essential to understand the purpose of these forms and how they interact with each other, bringing clarity and simplicity to what can otherwise be a complex process.