Free New York Dtf 84 Form in PDF

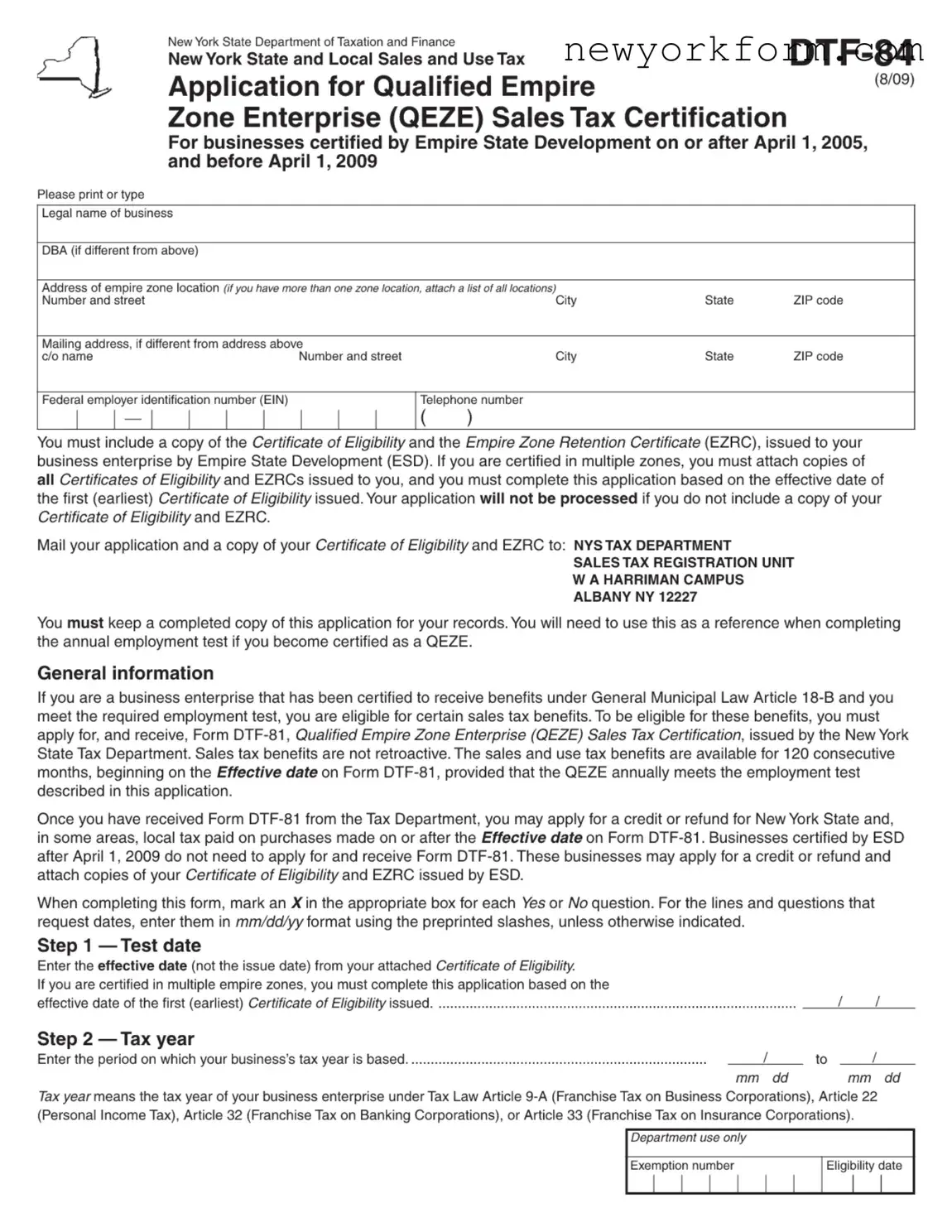

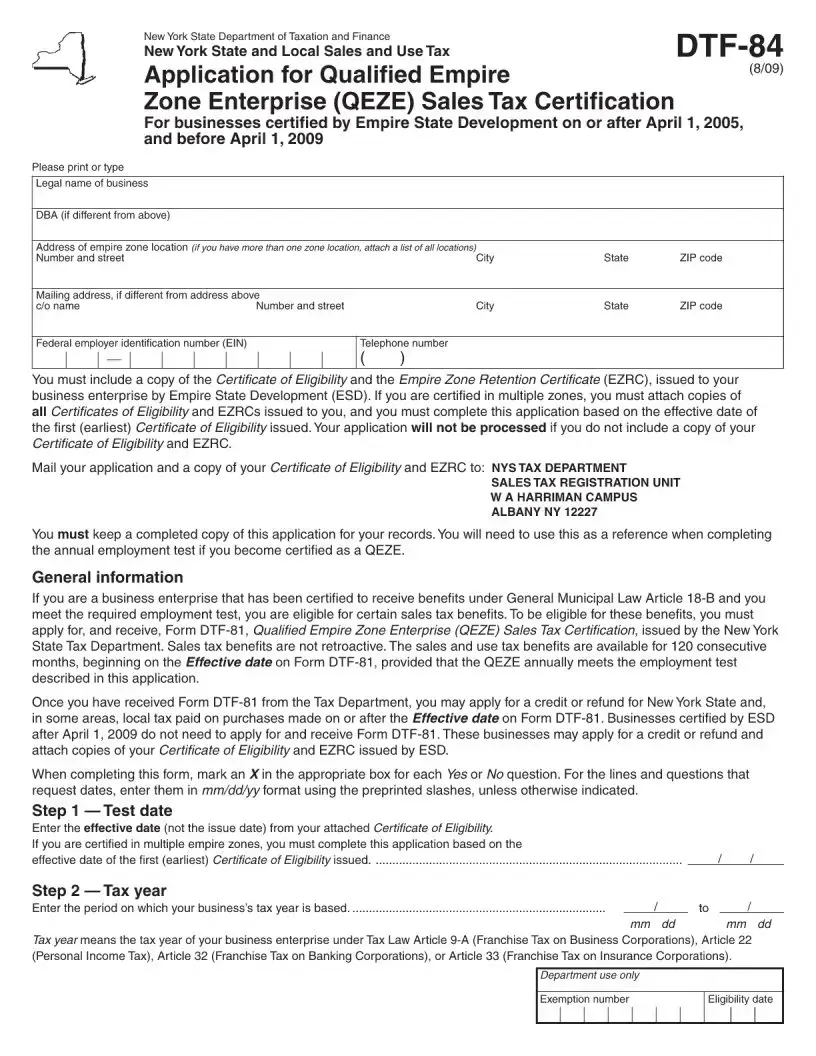

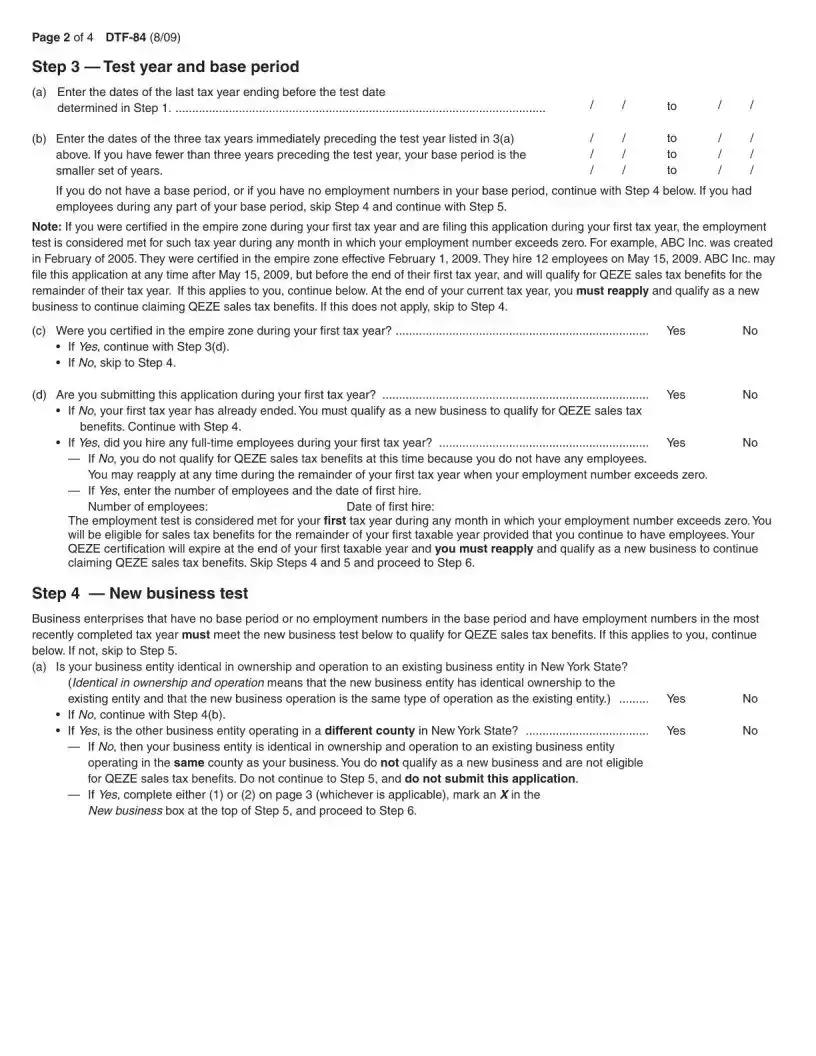

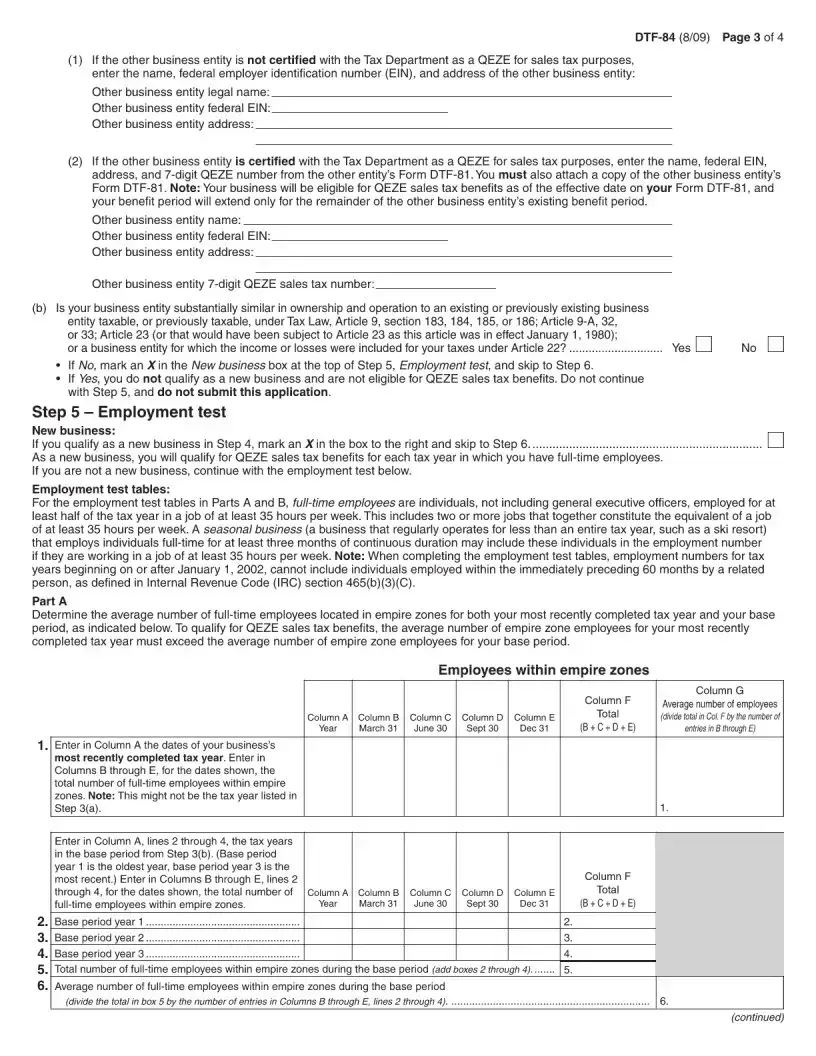

In the world of New York State taxes, the DTF-84 form plays a pivotal role for business entities. This form, which might seem daunting at first glance, is essential for businesses seeking to establish or confirm their sales tax status. It's particularly valuable for newly established companies, or those undergoing ownership or organizational changes, that need to apply for a Certificate of Authority to collect sales tax within the state. Through this form, businesses can detail their specific activities, ownership information, and operational locations, thus ensuring compliance with state tax laws. The state utilizes the information provided to assess tax responsibilities and to issue the appropriate tax documents. Understanding the DTF-84 form's requirements, how to accurately complete it, and the implications of the information provided can significantly ease the application process for a Certificate of Authority, smoothing the way for businesses to legally operate within New York's dynamic economy.

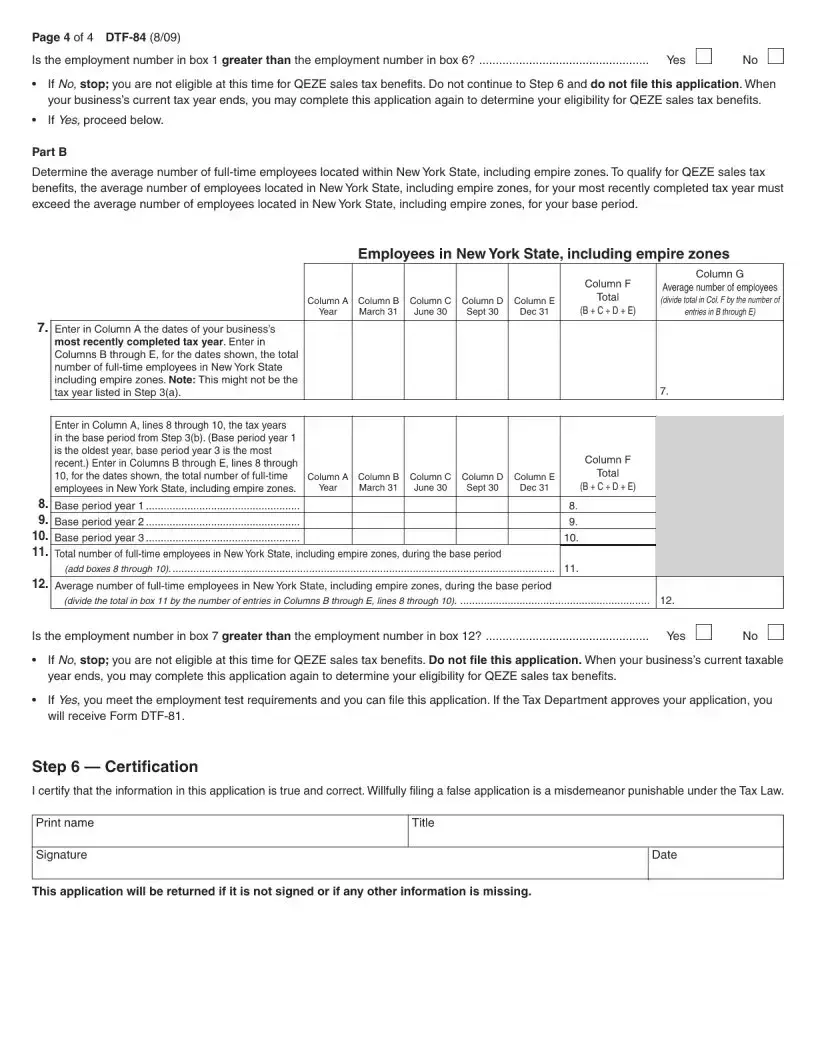

New York Dtf 84 Sample

File Overview

| Fact | Detail |

|---|---|

| Form Name | New York State Department of Taxation and Finance Employee's Withholding Allowance Certificate |

| Purpose | To determine the amount of New York State, New York City, and Yonkers tax to be withheld from an employee's paycheck |

| Who Must File | Employees working in New York State who want to adjust their withholding allowances or who need to have tax withheld at a higher rate |

| Where to File | Submitted to the employer, not directly to the New York State Department of Taxation and Finance |

| Form Number | DTF-84 |

| Governing Law | New York State Tax Law – Article 22, Sections 671-685 |

| Revisions | Subject to updates and revisions, which are typically announced by the Department of Taxation and Finance |

| Accessibility | Available online through the New York State Department of Taxation and Finance website |

| Additional Requirements | Employees claiming exemption from withholding must meet specific criteria and annually submit a new Form DTF-84 |

| Penalties | Incorrect or fraudulent withholding allowance claims may result in penalties |

New York Dtf 84: Usage Guidelines

Filling out the New York DTF-84 form is a straightforward process, yet it requires attention to detail to ensure accuracy and compliance. This form is essential for taxpayers who are involved with estate matters and need to address specific financial disclosures related to the estate's assets and liabilities. Once completed, the DTF-84 form becomes part of the official records and aids in the transparent and fair management of estate-related financial responsibilities. To fill out this form correctly, follow the steps below, ensuring all the information provided is accurate and up to date.

- Start by entering the full legal name of the estate in the designated space at the top of the form.

- Next, fill in the estate's identification number. This is a unique number assigned for tax purposes.

- Input the date when the form is being filled out in the specified field.

- Provide the name and title of the fiduciary responsible for the estate. This is usually the executor or administrator appointed by the court.

- List all assets and liabilities of the estate in the sections provided. Ensure each asset or liability is described clearly and valued accurately.

- If additional space is needed, attach separate sheets following the format outlined in the form’s instructions. Make sure to mark these sheets clearly as belonging to the DTF-84 form and number them consecutively.

- Review all the information provided on the form and the attached sheets, if any, to confirm its accuracy and completeness.

- Sign and date the form in the designated area. The signature must be that of the fiduciary responsible for the estate.

- Submit the completed DTF-84 form to the New York State Department of Taxation and Finance, following the submission guidelines provided in the form's instructions.

Accurately completing the DTF-84 form is crucial for meeting legal obligations and ensuring the financial aspects of the estate are handled properly. Take your time to gather all necessary information and review everything thoroughly before submission. Compliance with these steps will contribute to a smoother process in managing the estate's tax-related matters.

FAQ

-

What is the New York DTF-84 form?

The New York DTF-84 form, officially recognized as the Affidavit for Transfer of Motor Vehicle, is a legal document required by the New York State Department of Taxation and Finance. It is used when a vehicle is acquired through a means other than a traditional sale, such as a gift, inheritance, or as a part of settling an estate. This form is essential for the proper registration and transfer of ownership of the vehicle.

-

Who needs to file the New York DTF-84 form?

Any individual who acquires a motor vehicle in a manner that does not involve a standard purchase transaction within New York State is required to file the DTF-84 form. This applies to situations where a vehicle is received as a gift, through inheritance, or in settlement of an estate, among other circumstances.

-

When should the New York DTF-84 form be filed?

The DTF-84 form should be filed at the time of registration of the motor vehicle with the New York Department of Motor Vehicles (DMV). Timely filing is crucial to avoid any potential legal issues or delays in the registration process.

-

What information is required to complete the DTF-84 form?

To complete the DTF-84 form, you will need to provide detailed information about the transaction and the vehicle. This includes the vehicle's make, model, year, Vehicle Identification Number (VIN), the names and addresses of both the transferrer and the recipient, and the specific circumstances of the transfer. Additionally, attestation to the facts as they are presented and acknowledgment of understanding the tax implications are required.

-

Where can I find the New York DTF-84 form?

The New York DTF-84 form is available for download from the New York State Department of Taxation and Finance website. It can also be obtained in person from local DMV offices or by contacting the Department of Taxation and Finance directly to request a mailed copy.

-

Is there a fee to file the New York DTF-84 form?

There is no fee to submit the DTF-84 form itself. However, other fees related to the registration of the vehicle, including but not limited to sales tax or other applicable taxes, may apply depending on the specific circumstances of the vehicle transfer.

-

What are the consequences of not filing the DTF-84 form?

Failing to file the DTF-84 form can result in a variety of legal and financial complications. These may include delays in the registration process, penalties for non-compliance with state tax laws, and potential challenges in establishing legal ownership of the vehicle.

-

Can the DTF-84 form be filed electronically?

As of the last update, the New York DTF-84 form must be submitted in paper form. Electronic submission options are not currently available for this specific form. Interested parties are advised to check the latest guidelines from the New York State Department of Taxation and Finance for any updates on submission methods.

-

Who can I contact for assistance with the DTF-84 form?

For assistance with the DTF-84 form, individuals can contact the New York State Department of Taxation and Finance directly. Support is available through their helpline, via email, or in person at a local office. Expert advice and guidance can help ensure that the form is completed accurately and submitted properly.

Common mistakes

Filling out governmental forms can often be a daunting task due to their complexity and the fear of making a mistake. The New York DTF-84 form, used for registering a sales tax certificate of authority, is no exception. When this form is not filled out correctly, it can lead to delays or even the rejection of an application. Knowing the common mistakes to avoid is crucial in ensuring a smooth registration process.

- Not Checking the Box for the Correct Type of Business Entity: One of the first sections requires the applicant to identify the type of business entity. This is a common area where mistakes are made. Selecting the wrong entity type can create complications and confusion later on. Whether it's a sole proprietorship, partnership, corporation, or LLC, it's vital to ensure the correct box is checked.

- Leaving Required Fields Blank: Some fields on the DTF-84 form are mandatory. Failing to fill in all required areas is a significant error. This oversight can lead to the form being returned or the processing delayed. Double-checking that all necessary information has been provided before submitting can circumvent this issue.

- Inaccurate or Incomplete Description of Business Activities: The form asks for a detailed description of business activities. A mistake often made here is providing vague or incomplete information. Being as detailed and specific as possible helps New York's Department of Taxation and Finance understand the business, which is essential for the proper assessment of tax liabilities.

- Miscalculating the Estimated Monthly Sales Tax: Applicants are required to estimate their monthly sales tax. Incorrectly estimating this figure, either by overestimating or underestimating, can lead to unnecessary complications, including financial penalties. It's advisable to use historical sales data or industry averages as benchmarks for these estimates.

- Incorrect or Missing Signature: The form must be signed by the owner, officer, or authorized agent of the business. An oversight often seen is the submission of the form without the necessary signature or with a signature that does not match the records. This discrepancy can invalidate the entire application.

- Not Including the Appropriate Documentation: The DTF-84 form may require supporting documentation, depending on the business entity and its specific situation. A common mistake is neglecting to include these documents with the submission. This oversight can result in processing delays or a denial of the application.

- Incorrect Contact Information: Providing inaccurate or outdated contact information can significantly delay the process. Whether it's an email, phone number, or mailing address, ensuring that all contact information is current and correct is essential for any correspondence related to the application.

Avoiding these errors when completing the New York DTF-84 form is pivotal for businesses aiming for a hassle-free registration. Each mistake, while seemingly minor, can lead to delays, additional scrutiny, or outright rejection of the application. By approaching this task with attention to detail and ensuring all information is accurate and complete, businesses can facilitate a smoother registration process, allowing them to focus on their operations rather than bureaucratic hurdles.

Documents used along the form

In the realm of managing and organizing tax-related documents in New York, the New York DTF 84 form serves as a crucial piece of paperwork for those navigating their tax responsibilities. This form, however, often does not stand alone. Several other documents commonly accompany it, each playing a vital role in ensuring the completeness and accuracy of one's tax affairs. The synergy between these documents facilitates a smoother interaction with tax regulations, making it essential for individuals and businesses alike to be familiar with them.

- Form IT-201: This is the Individual Income Tax Return form. It serves as the primary form for New York State residents to file their annual income tax return. Accompanying the DTF 84, this form provides a comprehensive overview of an individual's income, deductions, and credits for the year.

- Form IT-2: Known as the Summary of W-2 Statements, this form consolidates information from all W-2 forms received by an individual. It's critical for accurately reporting wages and taxes withheld to the state, making it an essential accompaniment to the DTF 84 for those employed.

- Form IT-1099-R: This form is used to report distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, insurance contracts, etc. For individuals who need to report such income, this form works alongside the DTF 84 to provide a detailed account of such earnings.

- Form IT-214: Also known as Claim for Real Property Tax Credit, this form is used by New York residents to claim a credit for eligible real estate taxes paid. For homeowners or renters who qualify, this form complements the DTF 84 by potentially reducing the overall tax liability.

- Form W-4: The Employee's Withholding Certificate allows individuals to determine the amount of federal income tax to be withheld from their paychecks. While not a state form, this federal document supports the accuracy of both federal and state tax filings, including the submission of the DTF 84.

- Schedule A (Form IT-201): This schedule is an itemized deduction form that provides a detailed account of allowable deductions beyond the standard deduction. For those with significant deductible expenses, this schedule enhances the DTF 84 form by clearly itemizing these deductions.

- Form IT-203: For nonresidents or part-year residents of New York, this form serves as the Nonresident and Part-Year Resident Income Tax Return. It is essential for individuals in these categories to accurately report income earned in New York State, alongside the DTF 84, to ensure proper tax compliance.

Collectively, these forms and documents create a comprehensive framework for addressing a wide range of tax situations in New York. From detailing income sources to articulating deductions, credits, and withholdings, the purposeful compilation of these forms alongside the DTF 84 ensures that individuals and businesses can navigate their tax obligations with greater confidence and accuracy.

Similar forms

The New York DTF 84 form, pivotal for recording transactions and changes in certificate of authority for sales tax, shares similarities with various other documents, each serving specific yet akin regulatory or compliance functions. One such document is the IRS Form W-9, Request for Taxpayer Identification Number and Certification. Like the DTF 84, the W-9 is used to collect taxpayer information, ensuring that accurate financial reporting is maintained for tax purposes. Both forms play a crucial role in the administration of tax laws, albeit for different tax-related purposes.

Another document analogous to the New York DTF 84 form is the Form SS-4, Application for Employer Identification Number (EIN) issued by the Internal Revenue Service. This form is used by entities to apply for an EIN, a requirement for tax filing and reporting similar to the certificate of authority addressed by the DTF 84. Both forms are essential in the establishment and recognition of an entity’s tax responsibilities and identity in their respective domains.

The New York State ST-100, Quarterly Sales and Use Tax Return, also shares similarities with the DTF 84 form. The ST-100 is used by businesses to report and pay the sales and use tax they have collected, analogous to how the DTF 84 manages the issuance or changes in the certificate of authority needed to collect such taxes. Both documents are integral to New York State’s sales tax compliance and regulatory framework.

Similarly, the Certificate of Registration for Sales Tax (Form ST-1) found in other states is akin to the DTF 84 in that it serves as the document businesses use to register for sales tax collection. While the specifics can vary from state to state, the core purpose aligns with the DTF 84's role in New York, highlighting the universal need for such regulatory documentation across different jurisdictions.

The Uniform Commercial Code (UCC-1) Financing Statement is another document sharing a fundamental resemblance with the DTF 84. Though primarily used for a different purpose – securing interest in a borrower's personal property as collateral for a loan – it aligns with the DTF 84 in the aspect of registering and publicizing a legal or financial claim. Both forms ensure public notice of a registrant’s status or claim, serving critical roles in legal and financial transparency.

The Business Certificate for Partnerships operating in New York, often required at the county level, is similar to the DTF 84 form as both are necessary for the legal operation of businesses within the state. These forms help in establishing the business’s legal identity and authority to conduct business, which includes collecting sales taxes, in the case of the DTF 84 Form.

Lastly, the Application for Authority, often referenced by the form number NYS DOS 1336, is necessary for out-of-state entities wishing to do business in New York. This form bears resemblance to the DTF 84 in its purpose of enabling businesses to legally operate within a specific jurisdiction. However, while the DOS 1336 grants general operating authority, the DTF 84 is specific to the authority related to sales tax collection. Together, they underscore the layered requirements for businesses to comply with state regulatory frameworks.

Each of these documents, while serving distinct regulatory or compliance functions, intersect in their collective aim to organize and affirm the legal and fiscal responsibilities of entities. The New York DTF 84 form, by focusing on the sales tax certificate of authority, is a vital piece in the larger mosaic of business operation and tax regulation documentation, highlighting the interconnectivity of various administrative processes.

Dos and Don'ts

Filling out the New York DTF-84 form, which pertains to tax-related matters, requires attention to detail and an understanding of the form's requirements. To ensure that the process is completed correctly and efficiently, here are nine dos and don'ts to keep in mind:

- Do thoroughly read the instructions before you start filling out the form to ensure that you understand all the requirements.

- Do use black ink or type when filling out the form, as this ensures legibility and prevents any processing delays.

- Do double-check your figures and calculations to prevent any errors. Mistakes can lead to delays or incorrect tax assessments.

- Do include your social security number or employer identification number, as failing to do so may result in processing delays or penalties.

- Do contact a tax professional if you have questions or uncertainties. Tax laws can be complex, and professional guidance can help avoid errors.

- Don't leave any required fields blank. If a section does not apply to you, it's better to write "N/A" instead of leaving it empty.

- Don't use correction fluid or tape. If you make a mistake, it's advisable to start with a fresh form to maintain the document's clarity and legibility.

- Don't estimate figures. Use exact amounts whenever possible to ensure the accuracy of your tax reporting.

- Don't forget to sign and date the form. An unsigned form is considered incomplete and will not be processed.

By following these guidelines, individuals can fill out the New York DTF-84 form accurately and efficiently, helping to ensure a smooth process in their tax-related endeavors.

Misconceptions

When it comes to understanding the New York DTF-84 form, commonly referred to as the "Affidavit of Loss" form issued by the New York State Department of Taxation and Finance, several misconceptions often cloud its true purpose and function. Let's clear the air and debunk some of these myths.

It's only for businesses: A common misconception is that the DTF-84 form is solely for businesses to use. In reality, this form can be utilized by both individuals and businesses alike. It's designed to report the loss or destruction of important tax documents, not limited to any one group.

It's a form to file for tax returns: Some people mistakenly believe that the DTF-84 is a form to file their tax returns. However, its actual purpose is to serve as an affidavit for declaring the loss, destruction, or theft of New York State tax records and documents, not for filing tax returns.

It can replace lost documents: Another myth is the assumption that completing the DTF-84 form will automatically replace the lost tax documents. While filling out the form is an essential step, it primarily serves as a formal declaration of loss. The replacement of documents involves additional steps with the relevant tax authorities.

There's a fee to submit it: The process of submitting a DTF-84 form is free. Some may be under the impression that there's a processing fee, but the New York State Department of Taxation and Finance does not charge for the submission of this affidavit of loss.

Online submission is available: As much as digital advancements have streamlined many processes, the DTF-84 form does not have an online submission option. It must be mailed or faxed to the Department of Taxation and Finance, which can surprise those accustomed to online services.

Filling it out guarantees a tax audit exemption: A misunderstanding exists that once the DTF-84 is filed, it grants the filer immunity from tax audits on the lost documents. Filing this affidavit does not exempt individuals or businesses from audits, but rather informs the department of the situation should discrepancies arise.

Any lost document requires a DTF-84: While important, the DTF-84 form is specifically for declaring the loss of New York State tax documents. Not all lost documents related to tax affairs require the submission of this form. It's crucial to understand the specific circumstances under which it's necessary.

Immediate action is not necessary: Procrastination is a common trait, but delaying the filing of a DTF-84 after noticing the loss of tax documents can lead to complications. Immediate action is advised to prevent potential misuse or other issues arising from the loss of important tax-related documents.

In conclusion, the New York DTF-84 form is a critical tool for declaring lost, destroyed, or stolen tax documents to the New York State Department of Taxation and Finance. By understanding its actual purpose and debunking these common misconceptions, individuals and businesses can navigate their tax responsibilities more effectively and avoid potential pitfalls.

Key takeaways

The New York DTF 84 form, associated with tax registration for certain businesses, is an important document requiring careful attention to detail when filling out and using it. Here are nine key takeaways to consider:

- Understand Its Purpose: The form is designed to register businesses for various tax responsibilities in New York State. Knowing which taxes apply to your business is crucial before you start completing the form.

- Complete All Required Sections: Leaving sections incomplete can lead to processing delays or rejections. Make sure every applicable part of the form is filled out accurately.

- Provide Accurate Information: Any incorrect details can not only delay the processing but also potentially lead to penalties. Double-check all entries for accuracy.

- Know Your Tax Obligations: Different businesses have different tax responsibilities. Research or consult a professional to understand which taxes your business needs to register for.

- Sign and Date the Form: An unsigned form is considered invalid. Ensure that the authorized person signs and dates the form before submission.

- Keep a Copy for Your Records: After submitting the form, it's wise to retain a copy for your business records. This copy will be useful for future reference or in case of any disputes.

- Submit Before Deadlines: Adhering to submission deadlines is important to avoid penalties. Check the due dates applicable to your tax registrations.

- Update Information as Necessary: If your business information changes, such as the address or ownership, you need to update the state by submitting a new form. Keeping your information current is vital.

- Seek Professional Advice if Needed: If you are unsure about any aspects of your tax registration, consulting with a professional can provide clarity and ensure you are in compliance with state laws.

By keeping these key points in mind, businesses can navigate the process of filling out and using the New York DTF 84 form more confidently and efficiently, ensuring compliance with state tax laws.

Common PDF Documents

What Is It 201 Tax Form - The NYS IT-201-D form is a detailed document for New York State residents to itemize deductions, enhancing tax return accuracy.

Ny Sales Tax Rate 2023 - Filing the 810 form helps in preventing other businesses from registering the same or a similar name in New York.

Nyc Pw5 - Demands accurate completion of all fields to facilitate a comprehensive review of the after-hours work request.