Free New York 8104 Form in PDF

The form 8104 is a significant document associated with the New York Life Insurance Company, including its Arizona branch and the New York Life and Annuity Corporation. This document, crucial for policyholders, outlines procedures for changing dividend options on insurance policies. It stipulates that such changes will be acknowledged on the current policy anniversary date provided the request is received at least 31 days prior to this date; otherwise, changes take effect on the subsequent anniversary. The form caters to diverse preferences by offering options like canceling the One Year Term Rider, electing for Paid-Up Additions, leaving dividends to accumulate at interest, applying dividends to pay premiums or loans, or even receiving them in cash. It also specifies that Whole Life Additions are limited to policies issued within a particular timeframe. Additionally, the form features a section for tax withholding choices in compliance with IRS requirements, making it evident that policyholders' Social Security or Tax ID numbers are mandatory to prevent automatic withholding. Completing this form correctly can affect policyholders' loan repayment methods and dividend benefits, emphasizing the need for careful review and consideration of the elections made pertaining to dividend options and tax withholding preferences.

New York 8104 Sample

Next >

Print...

New York Life Insurance Company |

NYLIFE Insurance Company of Arizona |

New York Life and Annuity Corporation |

(Not licensed in every state) |

(A Delaware Corporation) |

4343 North Scottsdale Rd, Suite 220 |

51 Madison Avenue, New York, NY 10010 |

Scottsdale, AZ 85251 |

www.newyorklife.com |

|

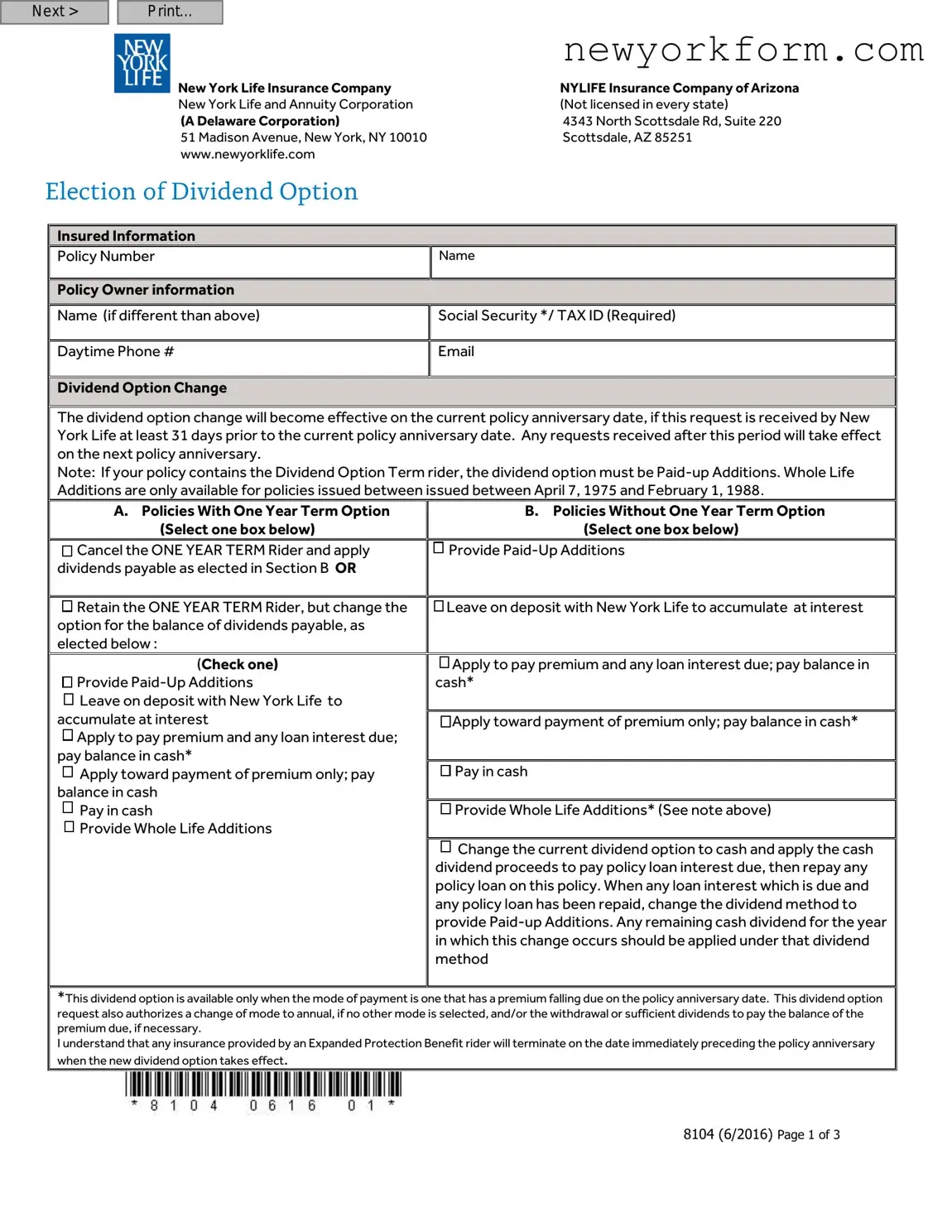

Insured Information

Insured Information

Policy Number |

Name |

|

|

Policy Owner information |

|

|

|

Name (if different than above) |

Social Security */ TAX ID (Required) |

|

|

Daytime Phone # |

|

|

|

Dividend Option Change

Dividend Option Change

The dividend option change will become effective on the current policy anniversary date, if this request is received by New York Life at least 31 days prior to the current policy anniversary date. Any requests received after this period will take effect on the next policy anniversary.

Note: If your policy contains the Dividend Option Term rider, the dividend option must be

A.Policies With One Year Term Option (Select one box below)

Cancel the ONE YEAR TERM Rider and apply dividends payable as elected in Section B OR

Cancel the ONE YEAR TERM Rider and apply dividends payable as elected in Section B OR

Retain the ONE YEAR TERM Rider, but change the option for the balance of dividends payable, as elected below :

Retain the ONE YEAR TERM Rider, but change the option for the balance of dividends payable, as elected below :

(Check one)

Provide

Provide

Leave on deposit with New York Life to accumulate at interest

Leave on deposit with New York Life to accumulate at interest

Apply to pay premium and any loan interest due; pay balance in cash*

Apply to pay premium and any loan interest due; pay balance in cash*

Apply toward payment of premium only; pay balance in cash

Apply toward payment of premium only; pay balance in cash

Pay in cash

Pay in cash

Provide Whole Life Additions

Provide Whole Life Additions

B.Policies Without One Year Term Option (Select one box below)

Provide

Provide

Leave on deposit with New York Life to accumulate at interest

Leave on deposit with New York Life to accumulate at interest

Apply to pay premium and any loan interest due; pay balance in cash*

Apply to pay premium and any loan interest due; pay balance in cash*

Apply toward payment of premium only; pay balance in cash*

Apply toward payment of premium only; pay balance in cash*

Pay in cash

Pay in cash

Provide Whole Life Additions* (See note above)

Provide Whole Life Additions* (See note above)

Change the current dividend option to cash and apply the cash dividend proceeds to pay policy loan interest due, then repay any policy loan on this policy. When any loan interest which is due and any policy loan has been repaid, change the dividend method to provide

Change the current dividend option to cash and apply the cash dividend proceeds to pay policy loan interest due, then repay any policy loan on this policy. When any loan interest which is due and any policy loan has been repaid, change the dividend method to provide

*This dividend option is available only when the mode of payment is one that has a premium falling due on the policy anniversary date. This dividend option request also authorizes a change of mode to annual, if no other mode is selected, and/or the withdrawal or sufficient dividends to pay the balance of the premium due, if necessary.

I understand that any insurance provided by an Expanded Protection Benefit rider will terminate on the date immediately preceding the policy anniversary when the new dividend option takes effect.

8104 (6/2016) Page 1 of 3

< Back

Next >

Print...

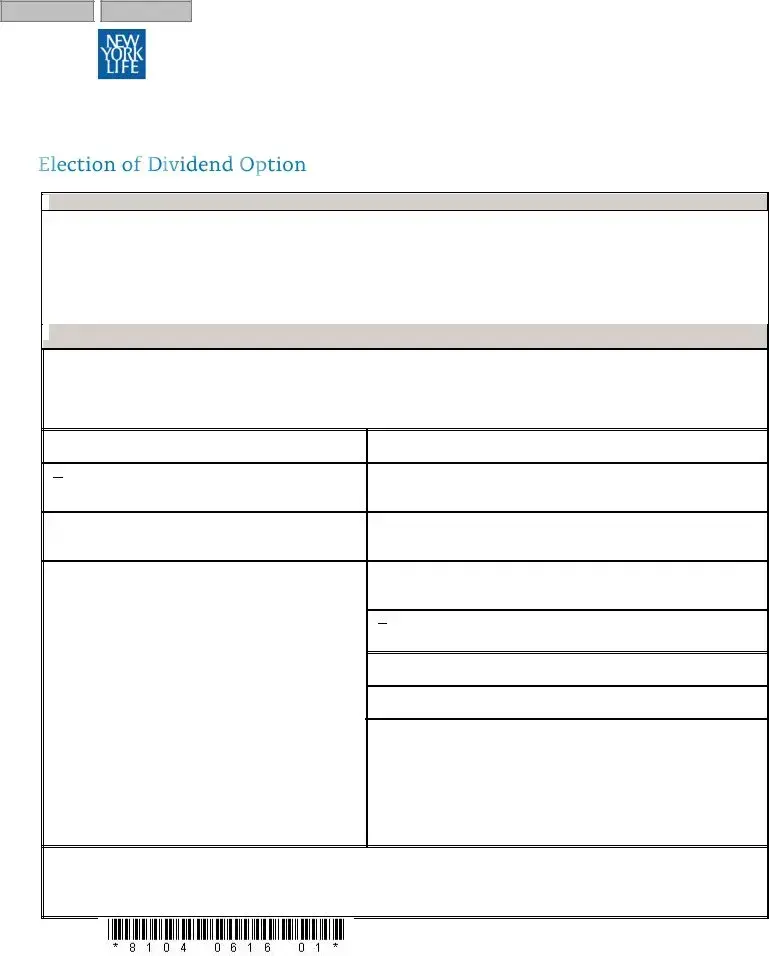

I wish to elect Added Value Advantage

Income Tax Withholding Section

Income Tax Withholding Section

IMPORTANT: The Internal Revenue Service (IRS) requires that you complete this section. See important tax information below before you make your withholding election. If your social security number (SSN) or taxpayer identification number (TIN) is not furnished, we are required by Federal law to withhold 10% of the taxable gain. Withholding election is not required for withdrawal from Dividend Deposits.

Are you a citizen of the United States (including a resident alien)? Yes |

No |

I elect to have the following withholding option applied to this payment and any future payment(s) under this policy (check only one box):

NO Federal or State Income taxes will be withheld |

ONLY Federal Income taxes withheld |

|

(This option may not be available for residents |

|

of certain states. See the State Income Tax |

|

Withholding section of this form) |

BOTH Federal and State Income taxes will be withheld

BOTH Federal and State Income taxes will be withheld

ONLY State income taxes withheld

If you elected any of the option above in which taxes will be withheld, you can specify the tax withholding percentage(%) of each withdrawal you would like to have applied to Federal and/or State income tax withholding. If a specific tax withholding amount is not indicated below, we will withhold 10% for federal tax purposes and the state’s minimum withholding (if applicable). Please fill in items (1) and (2) below.

(1)I would like to apply _____% of the taxable portion to Federal Withholding.

(2)I would like to apply _____% of the taxable portion to State Withholding.

If you elect to have Federal Income tax withheld, we are required to withhold at least 10% of the taxable portion of the distribution. If your state requires withholding, we will withhold the state’s minimum amount if you select an amount that is less than the minimum. Please see Important State Income Tax Withholding Information section.

Policyowner’s Signature (REQUIRED)

Policyowner’s Signature (REQUIRED)

Under penalties of perjury, I (as owner named) certify: (1) my social security number or Tax ID number shown on this form is my correct taxpayer identification number, (2) I am not subject to back withholding because (a) I am exempt from backup withholding; or (b) I have not been notified by the IRS that I am subject to backup withholding as a result of a failure to report all interest or dividend income; or (c) the IRS has notified me that I am no longer subject to backup withholding, (3) I am a U.S. person (includes a U.S. resident alien), and (4) I am exempt from Foreign Account Compliance Act (FATCA) reporting.

Check this box if the IRS has notified you that you are subject to backup withholding.

If I am not a U.S. citizen, U.S. resident alien or other U.S. person, I am submitting the applicable Form W8 with this form to certify my foreign status and if applicable, claim treaty benefits.

The Internal Revenue Service does not require your consent to any provision of this document other than the certifications required to avoid backup withholding.

X

|

Policy Owner Signature |

Name (Printed) |

Date |

|

|

X |

|

|

|

|

|

|

|

|

|

Policy Owner Signature |

Name (Printed) |

Date |

|

|

RETURN FORM TO: |

|

|

|

|

New York Life |

|

|

|

|

P.O. Box 130539 |

|

|

|

|

Dallas, TX |

|

|

|

8104 (6/2016) Page 2 of 3

< Back |

|

Print... |

|

|

|

Important Tax Information

Important Tax Information

You should consider very carefully which box you check above. You should consult with your personal tax advisor, plan administrator, State income tax authority, or your local IRS office if you have any questions about income tax withholding. IRS publication 505 (Tax Withholding and Estimated Tax) and IRS forms

Federal Income Tax Withholding

Federal Income Tax Withholding

A dividend withdrawal from your policy may result in a taxable gain reportable to the IRS on Form 1099. Federal income taxes must be withheld at a flat 10% rate from the taxable portion of your payment (as determined from our records), unless you elect not to have withholding apply by checking the appropriate box in the Income Tax Withholding Election section on this form.

Even if you elect not to have Federal income tax withheld, you are liable for payment of such tax on the taxable portion of your payment. There are penalties under the estimated tax payment rules if enough tax has not been paid through either estimated tax payments or withholding. If the taxable portion of a payment when added to the taxable portion of all other payments during the year is less than $200, Federal income tax is not required to be withheld.

State Income Tax Withholding

State Income Tax Withholding

In addition to the Federal income tax withholding requirements, some states require withholding on policy gains when federal income tax is withheld. As of January 1, 2012, the following states require state income tax withholding when federal income tax withholding is in effect: Iowa, Kansas, Maryland, Massachusetts, Nebraska, Oklahoma, and Virginia. If you live in Arkansas, California, Delaware, Georgia, Maine, North Carolina, Oregon, or Vermont we are required to withhold state income tax if federal income tax withholding is in effect, unless you elect not to have state income tax withheld. If you live in Michigan, we are required to withhold state income tax from the taxable portion of your payments, unless you provide us with a properly completed Form MI

If you reside in any of the following states and request state tax withholding, you must also specify the percentage of state tax withholding that you choose to apply to the taxable portion of the withdrawal: Alabama, Colorado, Connecticut, District of Columbia, Idaho, Illinois, Indiana, Kentucky, Louisiana, Minnesota, Missouri, Montana, New Jersey, New Mexico, New York, North Dakota, Ohio, South Carolina, Utah, West Virginia, and Wisconsin. In these states, if a percentage is not specified, state tax will not be

withheld.

8104 (6/2016) Page 3 of 3

File Overview

| Fact Number | Description |

|---|---|

| 1 | The New York Life 8104 form is used for dividend option changes, tax withholding elections, and providing insured information for policies under New York Life Insurance Company and its affiliates. |

| 2 | Dividend option changes on the form will become effective on the current policy anniversary date if received at least 31 days prior to the anniversary. |

| 3 | For policies with the Dividend Option Term rider, the dividend option must be Paid-up Additions, highlighting specific restrictions based on policy features. |

| 4 | Whole Life Additions are available only for policies issued between April 7, 1975, and February 1, 1988, indicating a limitation based on the issuance date of the policy. |

| 5 | The form includes a section requiring the policy owner’s social security number or Tax ID number to comply with IRS requirements, emphasizing the legal requirement for tax identification. |

| 6 | It's mandatory for the policy owner to make an income tax withholding election, underlining the adherence to Federal and potentially state tax laws. |

| 7 | Federal law mandates a 10% withholding of the taxable gain if the policy owner's social security or tax ID number is not provided, ensuring compliance with tax withholding regulations. |

| 8 | The form allows for the selection of NO Federal or State income taxes being withheld, with certain stipulations based on the state of residence, showcasing state-specific tax obligations. |

| 9 | Policy owners can elect to change their withholding election at any time, offering flexibility in managing tax liabilities. |

| 10 | Important tax information is provided to guide the policy owner on the impact of their elections, highlighting the need to consult with tax advisors or relevant authorities for personalized advice. |

New York 8104: Usage Guidelines

Filling out the New York 8104 form is a straightforward process that revolves around making dividend option changes to a life insurance policy. This form allows policyholders to adjust how they would like to manage the dividends earned from their insurance policies, affecting both current and future payments. It’s an important step for those looking to optimize their policy's financial potential or adjust their strategy based on changing needs or goals. Before proceeding, ensure you understand the options available and how they align with your financial planning. Here is a step-by-step guide to complete the form:

- Gather required information: Have the policy number, insured's name, policy owner's information (if different), Social Security or Tax ID, daytime phone number, and email address ready.

- Dividend Option Change: Decide on the change you want to make to the dividend option. This change will become effective on the policy’s anniversary date if the request is received at least 31 days prior.

- For policies with a One Year Term Option:

- Select whether to cancel the ONE YEAR TERM Rider and how to apply dividends in Section B.

- Or choose to retain the ONE YEAR TERM Rider and select a new option for the balance of dividends payable as detailed.

- For policies without a One Year Term Option, select one of the available options listed under section B.

- Added Value Advantage: If applicable, mark the relevant box.

- Income Tax Withholding Section: Complete this part to comply with IRS requirements. Indicate if you are a U.S. citizen and select your withholding preference. Specify the percentage of the taxable portion you wish to apply toward Federal and/or State withholding if applicable.

- Policy Owner’s Signature: Review the declarations under the penalties of perjury section, sign, print your name, and date the form. If there is a co-owner, they must also sign and date.

- Return the Form: Send the completed form to New York Life at the provided address.

It is crucial to carefully choose your dividend options and tax withholding preferences to align with your financial goals and tax obligations. Consulting with a financial advisor or tax professional is advisable to make informed decisions. Remember, changes to dividend options can have long-term effects on your policy's performance and your financial strategy.

FAQ

What is the New York 8104 form?

The New York 8104 form is a document used for policyholders of New York Life Insurance Company, NYLIFE Insurance Company of Arizona, and New York Life and Annuity Corporation to make changes to the dividend options on their life insurance policy. This form allows policy owners to select how dividends are paid or applied, update personal information, and make withholding elections for tax purposes.

How can a dividend option change be made effective?

For a dividend option change to be effective on the current policy anniversary date, the request must be received by New York Life at least 31 days prior to the current policy anniversary date. Requests received after this deadline will be processed and take effect on the next policy anniversary.

Which dividend options are available for policies with the One Year Term Rider?

- Cancel the ONE YEAR TERM Rider and apply dividends as elected in the subsequent section

- Retain the ONE YEAR TERM Rider and select a different option for the use of balance dividends

What are the dividend options for policies without the One Year Term Option?

- Provide Paid-Up Additions

- Leave on deposit with New York Life to accumulate at interest

- Apply to pay premium and any loan interest due, with the balance paid in cash

- Provide Whole Life Additions for policies issued within specific dates.

Who needs to complete the Added Value Advantage Income Tax Withholding Section?

This section must be completed by all policyholders wishing to make a withholding election regarding their dividend payments or policy withdrawals. The Internal Revenue Service requires this to determine the appropriate amount of federal and, if applicable, state income tax to withhold based on the policyholder’s citizenship status and elections.

What are the guidelines for tax withholding on dividend payments?

Federal income tax must be withheld at a flat 10% rate from any taxable portion of a policy's distribution unless the policyholder elects otherwise. States may also require withholding when federal tax is withheld. Policyholders have the option to specify the percentage for federal and/or state withholding. Failure to elect not to have taxes withheld or to withhold less than the state’s minimum (if lower than 10% is elected) can lead to automatic withholding at the standard rates. It's crucial for policyholders to check with their state to understand the requirements and potentially consult a tax advisor for personal guidance.

Common mistakes

Filling out New York's 8104 form can sometimes be complex, and individuals often make errors that could delay processing. Below are eight common mistakes to be aware of when completing the form.

- Not providing a Social Security or Tax ID number: This is a crucial requirement. Failure to include it can lead to automatic withholding of 10% of the taxable gain, as mandated by federal law.

- Inaccurate dividend option selection: Policyholders sometimes select dividend options that are not permitted under their policy's terms or fail to understand the options available, particularly between "Paid-Up Additions" and "Whole Life Additions."

- Misunderstanding the ONE YEAR TERM Rider options: Many individuals either skip over the choice between canceling the rider and reallocating dividends or do not fully comprehend the implications of their selection.

- Income Tax Withholding Section errors: Policy owners often overlook the importance of this section, neglecting to select their preferred withholding option or incorrectly calculating the withholding percentages for state and federal taxes.

- Omitting policy owner information: It's critical to ensure that all policy owner information, including contact details, is fully and accurately provided.

- Failure to sign the form: The policy owner's signature is required to process the form. Omitting the signature will result in the form being returned or processing delays.

- Incorrect policy number: Entering the wrong policy number can lead to significant processing delays or the form being mismatched with the wrong policy.

- Not consulting tax advice: The form clearly advises policyholders to consult with a tax advisor regarding income tax withholding. Failing to do so can result in unexpected tax implications.

Understanding and accurately completing each section of the form is essential to ensure the desired outcome for policy changes and tax handling. Policyholders are encouraged to take their time, double-check their entries, and seek professional advice if there's any uncertainty. This care can prevent unnecessary delays or financial implications.

Documents used along the form

When managing life insurance policies, like those offered by New York Life, policyholders often encounter a need to submit additional forms and documents alongside the primary form, such as the New York 8104 form. These supplementary documents are crucial for various reasons, including updating beneficiary information, addressing tax withholding preferences, or altering coverage details. Understanding these forms can streamline the process, making policy management smoother for policyholders.

- Change of Beneficiary Form: This form allows policyholders to update or change the beneficiary(ies) designated to receive the policy's benefits upon the insured's death. It is crucial for ensuring that benefits are distributed according to the policyholder's current wishes.

- Application for Policy Loan: Enables policyholders to borrow against the cash value of their life insurance policy, providing a source of funds while still keeping the policy in force. It is important for policyholders needing immediate financial assistance.

- Request for Policy Surrender: Used by policyholders who wish to terminate their policy before its maturity. Completing this form enables them to receive the policy's accrued cash value, minus any applicable surrender charges or loans.

- Automatic Premium Payment Authorization: Allows policy premiums to be automatically deducted from a checking or savings account, ensuring the policy remains active by avoiding missed payments due to oversight or mail delays.

- Statement of Health Form: Required when a policyholder wants to increase their coverage or apply for a new policy. This document assesses the individual's health and determines eligibility for insurance or additional coverage.

- IRS Form W-9: Requests a taxpayer identification number and certification. For policyowners, it's vital for ensuring that tax-related transactions, like distributions or interest payments from the policy, are reported accurately to the IRS.

Each of these documents plays a significant role in maintaining, updating, or leveraging a life insurance policy to meet the evolving needs of the policyholder. Whether it's adjusting who will benefit from the policy, accessing funds for immediate needs, ensuring timely premium payments, or complying with tax laws, these forms facilitate important actions that policyholders might need to take over the life of their policy. Understanding and utilizing these documents effectively can help policyholders make the most out of their life insurance policies.

Similar forms

The New York 8104 form shares many similarities with IRS Form W-9, primarily in how they both request taxpayer identification numbers and certification against backup withholding. Both forms serve as a means for individuals to provide their Social Security Number (SSN) or Tax Identification Number (TIN) to ensure accurate tax reporting and compliance, emphasizing the necessity of accurate personal identification in managing financial transactions and tax obligations.

Another document that echoes the utility of the New York 8104 form is Form W-4P, Withholding Certificate for Pension or Annuity Payments. Much like the 8104 form, which allows policyholders to elect their preferred method of income tax withholding on distributions, Form W-4P enables recipients of pensions, annuities, and other deferred compensation plans to determine the amount of federal income tax to be withheld from their payments, reflecting a shared goal of personalized tax management.

IRS Form 1099 mirrors the New York 8104 form in its role in reporting income to both payees and the IRS, specifically regarding the potential tax implications of dividend withdrawals. The 8104 form’s discussions around tax withholdings and dividend options allude to the necessity of issuing a Form 1099 to report any taxable gains, signifying both forms' integral roles in transparent financial reporting and tax compliance.

Form MI W-4P, specific to the state of Michigan, is similar to the New York 8104 form in its aim to manage state tax withholdings for pension or annuity payments. Like the 8104's detailed guidelines on voluntary state and federal tax withholding choices, the MI W-4P form grants individuals the ability to control their tax withholdings, showcasing both forms’ commitment to offering choices to taxpayers in their respective states.

Similar to the New York 8104 form, the Life Insurance Application Form is used in the insurance industry but for initial policy setup rather than managing dividends or tax withholdings. Both documents require detailed personal information, policy details, and illustrate the broader process of establishing and modifying life insurance coverage, highlighting procedural nuances in insurance administration.

IRS Publication 505 (Tax Withholding and Estimated Tax) can be closely associated with the information provided in the New York 8104 form concerning tax withholdings. The publication provides detailed guidance on how to adjust withholding and make estimated tax payments, paralleling the 8104 form’s instructions on choosing withholding options for insurance dividend payments, both aiming to help taxpayers meet their tax obligations efficiently.

The Policy Change Request Form, commonly used in the insurance sector, shares its purpose with the New York 8104 form in allowing policyholders to make alterations to their insurance contracts. While the 8104 form focuses on dividend options and tax withholding elections, policy change forms can encompass a broader range of modifications, demonstrating the dynamic nature of insurance policies and the need for periodic adjustments.

Form W-8, used by non-U.S. persons to certify their foreign status and claim benefits under the Foreign Account Tax Compliance Act (FATCA), parallels the New York 8104 form’s segment on tax compliance and certification. Both forms ensure adherence to U.S. tax laws, specifically in verifying the tax status of individuals and facilitating appropriate tax treatment, underscoring the importance of tax identity in financial dealings.

The Dividend Option Change Request Form, often utilized within insurance companies, is specifically designed to alter the way dividends are handled and can be directly compared to the segment of the New York 8104 form dealing with dividend options. Both documents empower policyholders by allowing them to recalibrate the financial approach to their dividends, either reinvesting them, applying them towards premiums, or receiving them in cash.

Finally, the State Income Tax Withholding Election Form, which can be considered akin to the New York 8104 form, enables individuals to make informed choices about their state tax withholdings on various distributions, including insurance payouts. Both documents provide important options for managing tax implications based on the policyholder's residence and personal tax circumstances, reflecting the intertwined nature of tax policy and personal finance.

Dos and Don'ts

When filling out the New York 8104 form, it's important to know what you should and shouldn't do to ensure that the information is accurate and compliant. Here are some guidelines to follow:

What You Should Do:- Review the form thoroughly before you start filling it out to ensure you understand each section.

- Check the policy number and ensure it matches the information on your policy documents.

- Provide accurate personal information, including your name, social security number, or tax ID, as these are required for identification and tax purposes.

- Make a clear choice regarding the dividend option change you desire, understanding the options available based on your policy details.

- Complete the Income Tax Withholding Section if applicable, especially if you wish to change your withholding preferences or update your tax information.

- Sign and date the form to certify that the information provided is correct and that you understand the implications of your selections.

- Return the completed form to the designated address provided by New York Life before the deadline to ensure your changes take effect on the desired date.

- Don’t leave the social security number or tax ID section blank, as failure to provide this information can lead to mandatory tax withholding.

- Don’t overlook the policy anniversary date requirement for dividend option changes to ensure your request is processed for the current year.

- Avoid selecting a dividend option that is not available for your policy type, particularly noting the restrictions on Whole Life Additions and similar specifics.

- Do not ignore the “Important Tax Information” section, as this contains vital information about your tax obligations and options.

- Don’t forget to specify the percentage of the taxable portion you wish tax withholding to apply to if you’re electing to withhold taxes, ensuring clarity and preventing default amounts.

- Avoid submitting the form without reviewing all your selections and verifying personal information to prevent errors or delays.

- Do not mail the form to the wrong address, as this could delay processing and affect the timing of your dividend option changes.

Misconceptions

When dealing with the complexities of insurance forms such as the New York 8104 form, it's easy to find oneself tangled in misconceptions. Understanding these forms properly is crucial to making informed decisions about your life insurance policy. Here are five common misunderstandings regarding the New York 8104 form and clear explanations to dispel them.

- Misconception 1: The 8104 form is only for changes to personal information.

This is not accurate. While the form does include sections for updating policy owner information, its primary purpose is to request changes to the dividend option on your life insurance policy. It allows policyholders to choose how dividends are used, such as applying them towards premium payments or adding them to the policy’s value.

- Misconception 2: Dividend options are limited regardless of the policy type.

Actually, the options available can vary depending on whether your policy includes specific riders or was issued in a certain timeframe. For instance, Whole Life Additions are only an option for policies issued between April 7, 1975, and February 1, 1988. Understanding the specifics of your policy is key to knowing which options you can select.

- Misconception 3: Changing dividend options can be done anytime before the policy anniversary date.

This statement is only partially true. While you can request a change at any time, for the new dividend option to take effect by the current anniversary date, New York Life must receive the form at least 31 days before that date. Requests submitted later will take effect the following year.

- Misconception 4: Withholding elections for dividends are optional.

In fact, the Internal Revenue Service (IRS) mandates that you complete the Income Tax Withholding Section if you are withdrawing dividends from your policy. Your social security or tax ID number is also required to prevent mandatory withholding of a portion of the taxable gain. This is a critical step to ensure compliance with federal tax laws.

- Misconception 5: The form is solely for New York residents.

Despite its name, the New York 8104 form is not exclusive to New York residents. It's applicable to policyholders across various states, subject to the specific rules and requirements of each state regarding dividend options and tax withholdings. It’s important to note the form even mentions states with specific withholding requirements, highlighting its wider relevance.

Clearing up these misconceptions ensures that policyholders are better equipped to make informed decisions about their insurance policies. Remember, when in doubt, seeking clarification from New York Life or a professional advisor is always a wise course of action.

Key takeaways

Here are key takeaways about filling out and using the New York 8104 form:

- The 8104 form is used for making changes to dividend options on a New York Life Insurance policy.

- Requests to change the dividend option must be received at least 31 days before the policy anniversary date to take effect on the current anniversary. Requests received after this period will take effect on the next anniversary.

- For policies with the Dividend Option Term Rider, dividends must be applied as Paid-up Additions, while Whole Life Additions are only available for policies issued between April 7, 1975, and February 1, 1988.

- Dividend options include providing Paid-Up Additions, leaving on deposit to accumulate interest, applying towards premium and loan interest, premium payment only, cash payment, and providing Whole Life Additions.

- Changing the dividend option to cash to pay policy loan interest and then repay any policy loan is possible. Once loans are repaid, dividends can then be used for Paid-up Additions.

- This form also includes an Income Tax Withholding Section, which is mandatory due to IRS requirements. If a Social Security Number (SSN) or Tax Identification Number (TIN) is not provided, a 10% withholding of the taxable gain is mandated by Federal law.

- Policy owners must select their preferred method for federal and, if applicable, state income tax withholdings. They have the option not to withhold taxes or choose different withholdings for federal and state taxes.

- Specifying the exact percentage for tax withholding is necessary if you want something other than the standard 10% federal withholding and the state’s minimum requirement.

- Policy owners must certify their SSN or TIN, confirm they are not subject to back withholding, and acknowledge their U.S. person status to avoid backup withholding penalties. If applicable, foreign persons must submit a Form W-8.

- For any changes in withholding preferences or dividend options, the policy owner's signature is required on the form, underscoring the importance of personal validation for any request.

Please note that consulting a tax advisor is recommended for making informed decisions about income tax withholding choices, which are also subject to changes in state laws.

Common PDF Documents

Cpap Application - Employers need to demonstrate experience rating for the policy period to qualify for any calculated credits.

Ny Dmv Forms - A direct approach is employed to prevent underage applicants from using or applying for multiple identities within the state's DMV system.

Shed Distance From Property Line - Zoning characteristics, including district and street width, are necessary to provide a complete picture of the proposed work’s location.